Alphabet Inc (Google): Is It a Buy Right Now?

Alphabet Inc, otherwise known as Google (ticker symbol: GOOGL), is currently trading at $160.7 per share. Over the past year, it's down about 6%, following a 22% decline from its all-time highs. However, over the past five years, the stock has surged by 134%, outperforming the S&P 500. Despite recent headwinds, Google is trading at a P/E ratio of 18, which is relatively low for a high-growth tech stock.

In this analysis, we’ll examine Google’s latest Q1 2025 earnings and determine if it's a buy or sell, using a discounted free cash flow model and comparable company analysis.

Google’s Financial Overview

Alphabet is valued at just under $2 trillion, with an earnings per share (EPS) of $8.83 and a beta of 1, making it slightly more volatile than the market. Analysts have a buy rating, with a price target just shy of $200 per share.

Google also pays a 0.54% dividend, amounting to $0.87 per share. They distribute $4.7 billion in dividends annually, accounting for 4% of net income and 6% of free cash flow. Investors interested in capturing the dividend should buy shares before June 9 to receive their quarterly payout.

Revenue Growth and Earnings Analysis

Google’s trailing twelve-month revenue is at an all-time high of $360 billion. Comparing Q1 2024 vs. Q1 2025, total revenue increased by $10 billion, with its largest segment, Google Search, contributing $50.7 billion. Advertising revenue rose from $8 billion to $8.9 billion, while Google Network saw a slight decline.

Breaking revenue down further:

- Google Services grew by $7 billion.

- Google Cloud increased by $3 billion.

- Other revenue declined slightly.

- Hedging gains added to overall growth.

Net income also reached $111 billion, making Google one of the most profitable companies globally. Free cash flow hit an all-time high of $75 billion, with operating cash flow growth outpacing capital expenditures.

Alphabet continues share buybacks, with the board approving a $70 billion repurchase of Class A and C shares—a sign of shareholder-friendly practices.

Dividend and Buyback Strategy

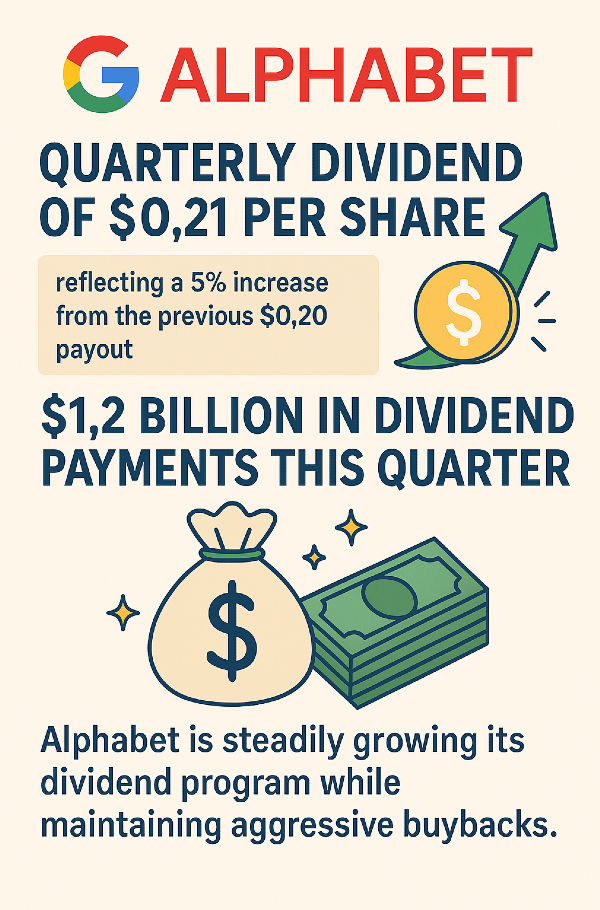

Alphabet declared a quarterly dividend of $0.21 per share, reflecting a 5% increase from the previous $0.20 payout. With $1.2 billion in dividend payments this quarter, Alphabet is steadily growing its dividend program while maintaining aggressive buybacks.

Valuation Models

Discounted Free Cash Flow (DCF) Model

Google's fair value estimate based on DCF analysis is $165 per share, suggesting a buy. Adjusting projections slightly:

- Expected revenue: $382 billion to $406 billion.

- Net income margin: 27.5% (up from prior estimates).

- Free cash flow conversion rate: 80%.

These adjustments push the valuation to $180 per share, further reinforcing Google as an undervalued buy.

Comparable Company Analysis

We compared Google to Apple (AAPL), Microsoft (MSFT), and Meta (META) to evaluate its competitive standing. Google ranks 8th largest by market cap, trailing Microsoft, Apple, Nvidia, Amazon, Meta, Broadcom, and Berkshire Hathaway.

Key metrics comparison:

- Revenue Growth (5-year): Google ranks among the top.

- Net Income: Google is the most profitable, at $111 billion.

- Profit Margins: 30%, higher than Apple but lower than Microsoft.

- Price-to-Sales & Price-to-Book: Google trades lower than competitors, indicating relative undervaluation.

Using industry-standard EV-to-EBITDA and PE ratios, Google's fair value estimate based on peer comparison is $230 per share, reinforcing strong upside potential.

Final Verdict: Is Google a Buy?

- DCF Model: Suggests Google is undervalued at $180 per share.

- Comparable Company Analysis: Estimates fair value around $230 per share.

- Ben Graham Valuation: Dislikes most tech stocks right now due to high bond yields, valuing Google at just $100 per share—but Graham's methodology tends to undervalue growth stocks.

- Dividend Growth: Still in early stages but showing consistent increases.

Comparing Google's 5-year performance against competitors:

- Alphabet up 134%, trailing Apple (144%), Microsoft (175%), and Meta (211%).

- Over the past year, Alphabet is the only stock down, while Meta is up 40%, Microsoft 8%, and Apple 13%.

Conclusion

Google appears undervalued relative to competitors, making it an attractive buying opportunity. If the stock rebounds toward its fair value estimates ($180–$230 per share), it could offer strong returns for long-term investors.

| Company |

Symbol |

Better Than GOOGL? |

| Amazon |

AMZN |

Amazon dominates e-commerce and cloud computing, with AWS driving high-margin growth. Its diversified revenue streams make it less reliant on advertising. |

| Microsoft |

MSFT |

Microsoft has a strong enterprise software business, recurring revenue from Office 365, and a leading position in AI and cloud computing with Azure. |

| Meta |

META |

Meta has a higher growth trajectory in social media and AI-driven advertising, with strong engagement across Facebook, Instagram, and WhatsApp. |

| Nvidia |

NVDA |

Nvidia leads in AI and GPU technology, benefiting from explosive demand in AI computing, gaming, and data centers. |

| Apple |

AAPL |

Apple has a loyal customer base, strong brand power, and high-margin hardware sales, complemented by growing services revenue. |

https://youtu.be/PlLTtpOX6Wg?si=xcrHkpwvVWxl4NnN

Alphabet Inc (Google): Is It a Buy Right Now?

Alphabet Inc, otherwise known as Google (ticker symbol: GOOGL), is currently trading at $160.7 per share. Over the past year, it's down about 6%, following a 22% decline from its all-time highs. However, over the past five years, the stock has surged by 134%, outperforming the S&P 500. Despite recent headwinds, Google is trading at a P/E ratio of 18, which is relatively low for a high-growth tech stock.

In this analysis, we’ll examine Google’s latest Q1 2025 earnings and determine if it's a buy or sell, using a discounted free cash flow model and comparable company analysis.

Google’s Financial Overview

Alphabet is valued at just under $2 trillion, with an earnings per share (EPS) of $8.83 and a beta of 1, making it slightly more volatile than the market. Analysts have a buy rating, with a price target just shy of $200 per share.

Google also pays a 0.54% dividend, amounting to $0.87 per share. They distribute $4.7 billion in dividends annually, accounting for 4% of net income and 6% of free cash flow. Investors interested in capturing the dividend should buy shares before June 9 to receive their quarterly payout.

Revenue Growth and Earnings Analysis

Google’s trailing twelve-month revenue is at an all-time high of $360 billion. Comparing Q1 2024 vs. Q1 2025, total revenue increased by $10 billion, with its largest segment, Google Search, contributing $50.7 billion. Advertising revenue rose from $8 billion to $8.9 billion, while Google Network saw a slight decline.

Breaking revenue down further:

Net income also reached $111 billion, making Google one of the most profitable companies globally. Free cash flow hit an all-time high of $75 billion, with operating cash flow growth outpacing capital expenditures.

Alphabet continues share buybacks, with the board approving a $70 billion repurchase of Class A and C shares—a sign of shareholder-friendly practices.

Dividend and Buyback Strategy

Alphabet declared a quarterly dividend of $0.21 per share, reflecting a 5% increase from the previous $0.20 payout. With $1.2 billion in dividend payments this quarter, Alphabet is steadily growing its dividend program while maintaining aggressive buybacks.

Valuation Models

Discounted Free Cash Flow (DCF) Model

Google's fair value estimate based on DCF analysis is $165 per share, suggesting a buy. Adjusting projections slightly:

These adjustments push the valuation to $180 per share, further reinforcing Google as an undervalued buy.

Comparable Company Analysis

We compared Google to Apple (AAPL), Microsoft (MSFT), and Meta (META) to evaluate its competitive standing. Google ranks 8th largest by market cap, trailing Microsoft, Apple, Nvidia, Amazon, Meta, Broadcom, and Berkshire Hathaway.

Key metrics comparison:

Using industry-standard EV-to-EBITDA and PE ratios, Google's fair value estimate based on peer comparison is $230 per share, reinforcing strong upside potential.

Final Verdict: Is Google a Buy?

Comparing Google's 5-year performance against competitors:

Conclusion

Google appears undervalued relative to competitors, making it an attractive buying opportunity. If the stock rebounds toward its fair value estimates ($180–$230 per share), it could offer strong returns for long-term investors.

https://youtu.be/PlLTtpOX6Wg?si=xcrHkpwvVWxl4NnN