Disclaimer

Thanks for joining me today for this analysis. Before we dive in, I need to address the recent news that broke on May 15th regarding a Department of Justice investigation into United Health Group’s Medicaid practices.

While the market has reacted strongly—dropping the stock 10% today alone—it’s important to step back and assess whether this news warrants a shift in our investment approach.

Let’s keep this in perspective: United Health’s stock was already down 48% since April, and now, with this DOJ probe speculation, it’s sitting at its lowest point in five years.

Here’s why I’m not changing my analysis: The Wall Street Journal has reported this as a possible probe, citing unnamed sources. Meanwhile, United Health Group itself has denied receiving any official notice of a new investigation.

We also need to recall that back in March, the DOJ failed to prove fraud against United Health Group, resulting in the case being dismissed due to lack of evidence. That history suggests this might just be another round of speculation rather than definitive wrongdoing.

Given these uncertainties, overreacting to the news—as the market appears to be doing—could open up a potential buying opportunity for investors. Until we have actual facts, I’m keeping my analysis unchanged.

Introduction

Welcome back! Today, we’re looking at another high-profile stock: United Health Group.

I’m Carlos McCord, CPA, and on this channel, I break down stocks to determine whether they are quality investments or ones to avoid.

United Health Group presents an interesting case right now. Over the past year, scrutiny on the healthcare industry has intensified, driven by frustration over high costs and corporate profits.

One of United Health’s subsidiaries, United Health Incorporated, made headlines when its CEO was murdered, an event that shocked many but also reflected underlying public dissatisfaction.

More recently, the CEO stepped down, causing further instability. With leadership changes, delayed guidance, and a 48% stock decline, investors are wondering—is this an opportunity or a warning sign?

Let’s dive into the numbers and see what’s happening.

Financial Overview

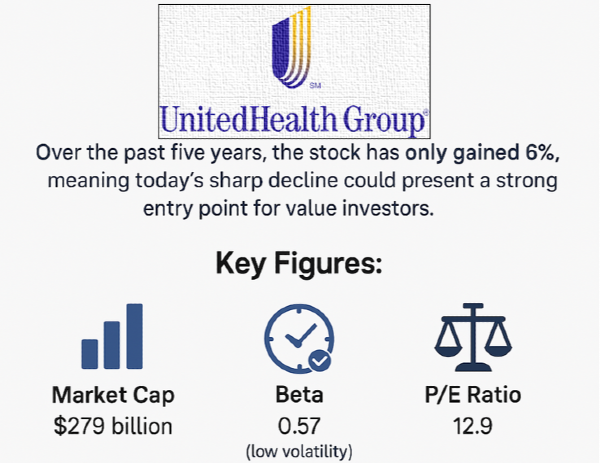

United Health Group is currently trading at $381 (as of May 14th). Over the past five years, the stock has only gained 6%, meaning today’s sharp decline could present a strong entry point for value investors.

Key Figures:

- Market Cap: $279 billion

- Beta: 0.57 (low volatility)

- P/E Ratio: 12.9

- Dividend Yield: 2.7%

This is a major industry leader with historically strong financials, so let’s break down the numbers further.

Revenue Growth

United Health Group has shown consistent double-digit growth, averaging 10-11% over the past decade.

| Year |

Revenue (Billion) |

Growth Rate (%) |

| 2015 |

$157 |

- |

| 2024 |

$407 |

10.5% avg |

In recent years, we’ve seen some single-digit growth—for example, 8.9% in 2020—but this hasn’t been concerning given the company’s overall trajectory.

Margins & Profitability

Margins have hovered around 23%, declining slightly to 21% over the past 12 months.

While this isn’t a major red flag, it could indicate cost pressures affecting profitability.

Net income tells a similar story. The company posted a 35% decline last year, but the trailing 12 months show a rebound to $22.1 billion, suggesting momentum is returning.

Profitability Over Time:

- 5-year net income growth: 3%

- 10-year net income growth: 11.3%

- Net profit margin: 3.6% (down from 6%, but trending back up)

It’s important to remember that healthcare isn’t a high-growth sector—this isn’t a new disruptor but rather an industry leader maintaining its position.

Free Cash Flow Stability

United Health Group’s free cash flow growth has remained modest in recent years, showing a 2.7% growth rate over the past three years and 5.9% over five years.

While there have been three down years, the latest data suggests a recovery back to its trend, aligning with the company’s net profit trajectory.

Debt & Leverage

Debt has increased from $25.4 billion in 2015 to $72.3 billion, but the company maintains strong leverage.

Key metric:

- Debt-to-free cash flow ratio: 3.5 (Ideally, this should be under 3, but under 5 is acceptable.)

- Average time to repay debt: 2.5 years—a solid position reflecting financial strength.

United Health Group demonstrates healthy debt management, ensuring its balance sheet remains strong while maintaining free cash flow.

Dividend Growth: A Powerhouse for Investors

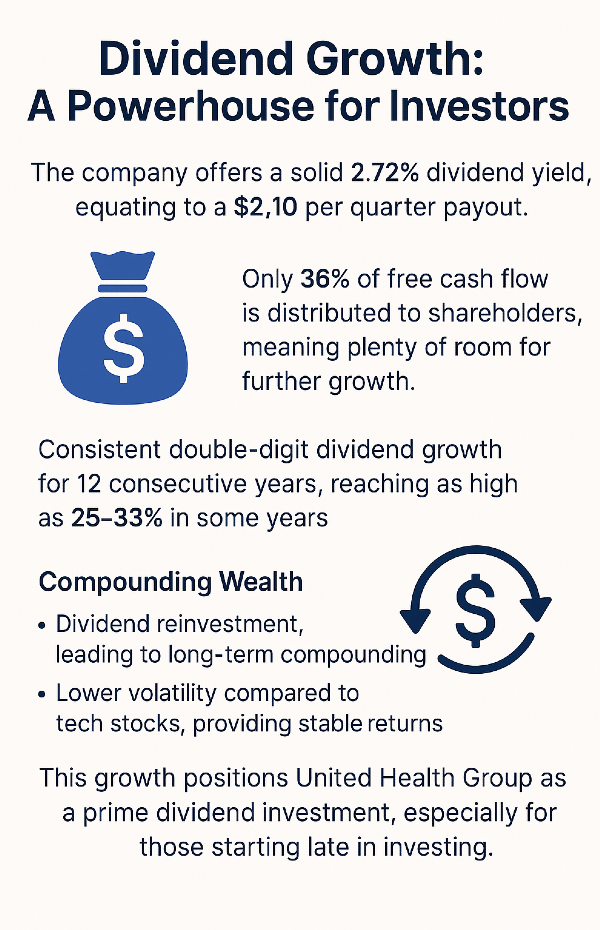

The company offers a solid 2.72% dividend yield, equating to a $2.10 per quarter payout.

What makes this dividend stand out?

- Only 36% of free cash flow is distributed to shareholders, meaning plenty of room for further growth.

- Consistent double-digit dividend growth for 12 consecutive years, reaching as high as 25-33% in some years.

This growth positions United Health Group as a prime dividend investment, especially for those starting late in investing.

Compounding Wealth

Investors benefit from:

- Dividend reinvestment, leading to long-term compounding.

- Lower volatility compared to tech stocks, providing stable returns.

If a company consistently raises dividends, investors essentially get a yearly “pay raise”—something most jobs don’t offer.

Share Buybacks & Value Creation

United Health Group has aggressively repurchased shares, reducing shares outstanding consistently over the years.

Despite a slight increase in the last year, the overall trend remains strongly downward, meaning existing shares become more valuable.

For a mature company, this share reduction strategy enhances investor value, complementing dividend payouts.

Return on Capital & Cost Efficiency

The company excels in capital efficiency, creating value at a strong spread:

- Return on Capital: 17.7%

- Weighted Average Cost of Capital (WACC): 4.53%

- Value creation spread: ~13% annually

This indicates smart management decisions, ensuring capital is used effectively.

Valuation: A Major Upside Potential

Based on its historical averages, United Health Group’s valuation suggests significant upside:

- Expected growth rate: 11% over the next five years

- Discount rate applied: 10% (adjusted with a risk premium)

- Historical price-to-free cash flow: 15x

Currently trading at $381, the intrinsic value estimate falls around $516, translating to an upside of 67%.

A fair range would be $490-$542, reinforcing the view that this stock remains undervalued.

Directional Investing vs. Exact Targets

While exact valuation figures are never guaranteed, directionally assessing whether a stock is overvalued, fairly valued, or undervalued is key to smart investing.

United Health Group, based on its financial health, dividend strength, and share buybacks, presents a compelling case for investment.

Conclusion: United Health Group’s Resilience Amid Market Uncertainty

United Health Group has faced significant volatility in recent months, with its stock plunging 48% due to external concerns. However, this decline does not necessarily indicate a deterioration in business fundamentals.

One of the key reassurances for investors is the leadership transition. While CEO changes often spark uncertainty, the incoming executive was previously the CEO and has remained closely connected to the business as board chairman. This level of familiarity reduces risk and suggests the company is not entering uncharted territory.

Market Overreaction vs. Reality

The scale of the stock’s decline raises an important question: Has United Health Group actually become 48% worse in a matter of months? The answer, backed by financial metrics and historical trends, is likely no. Investors often overreact to negative headlines, creating deep buying opportunities for those who assess long-term fundamentals rather than short-term price swings.

United Health Group remains a dominant force in healthcare, with a strong financial foundation, a consistent dividend payout, and a historically stable business model.

A Dow 30 Stock with Staying Power

This isn’t a speculative high-growth company—it’s an industry leader with established market dominance. Its membership in the Dow 30 and S&P 500 signals strong institutional backing, meaning most shareholders are unlikely to sell off completely despite short-term news cycles.

Why This Could Be a Buying Opportunity

For those seeking healthcare industry exposure, this moment presents one of the most attractive entry points in years. The stock’s price is now only 6% above where it was five years ago, reinforcing the long-term value proposition.

The company’s double-digit revenue growth—uncommon among mature businesses—further solidifies its investment appeal. Many large companies settle into mid-single-digit growth at this stage, yet United Health Group continues to grow at over 10% per year, proving its ability to expand efficiently even in a highly regulated industry.

Final Takeaway

Investors should approach this situation with pragmatic patience. The stock may continue experiencing short-term fluctuations, but United Health Group’s fundamentals remain intact. With its dividend growth, share repurchases, financial stability, and market leadership, the company is well-positioned to rebound over time.

This isn’t just about reacting to headlines—it’s about understanding the broader picture. Giants do fall, but they rarely stay down.

For those focused on long-term investing, United Health Group is a stock worth watching closely, if not outright considering as a potential addition to a portfolio.

Stocks Similar to UNH

| Company Name |

Symbol |

Why It May Be a Better Investment Than UNH |

| Elevance Health |

ELV |

Faster revenue growth and diversified services. Unlike UNH, Elevance Health has expanded aggressively into Medicaid and value-based care, offering potential upside in a rapidly changing healthcare landscape. |

| Cigna Group |

CI |

Stronger cost management and potential for higher margins. Cigna maintains a leaner operating structure, which has allowed it to generate better profit margins relative to UNH’s heavily diversified model. |

| Centene Corporation |

CNC |

Higher exposure to government healthcare programs. Centene focuses heavily on Medicaid, making it less susceptible to private insurance regulatory risks that UNH faces. |

| Humana Inc. |

HUM |

Dominance in Medicare Advantage. Humana specializes in serving the aging population, which has long-term stability and growth prospects that are more predictable than UNH’s broader model. |

| Molina Healthcare |

MOH |

More focused strategy and lower volatility. Molina avoids sprawling diversification, focusing instead on efficiency in government-funded health programs, resulting in less exposure to external risks affecting UNH. |

https://youtu.be/IPISO_RzfLY?si=a-XrAzTEmSJKyDy6

Disclaimer

Thanks for joining me today for this analysis. Before we dive in, I need to address the recent news that broke on May 15th regarding a Department of Justice investigation into United Health Group’s Medicaid practices.

While the market has reacted strongly—dropping the stock 10% today alone—it’s important to step back and assess whether this news warrants a shift in our investment approach.

Let’s keep this in perspective: United Health’s stock was already down 48% since April, and now, with this DOJ probe speculation, it’s sitting at its lowest point in five years.

Here’s why I’m not changing my analysis: The Wall Street Journal has reported this as a possible probe, citing unnamed sources. Meanwhile, United Health Group itself has denied receiving any official notice of a new investigation.

We also need to recall that back in March, the DOJ failed to prove fraud against United Health Group, resulting in the case being dismissed due to lack of evidence. That history suggests this might just be another round of speculation rather than definitive wrongdoing.

Given these uncertainties, overreacting to the news—as the market appears to be doing—could open up a potential buying opportunity for investors. Until we have actual facts, I’m keeping my analysis unchanged.

Introduction

Welcome back! Today, we’re looking at another high-profile stock: United Health Group.

I’m Carlos McCord, CPA, and on this channel, I break down stocks to determine whether they are quality investments or ones to avoid.

United Health Group presents an interesting case right now. Over the past year, scrutiny on the healthcare industry has intensified, driven by frustration over high costs and corporate profits.

One of United Health’s subsidiaries, United Health Incorporated, made headlines when its CEO was murdered, an event that shocked many but also reflected underlying public dissatisfaction.

More recently, the CEO stepped down, causing further instability. With leadership changes, delayed guidance, and a 48% stock decline, investors are wondering—is this an opportunity or a warning sign?

Let’s dive into the numbers and see what’s happening.

Financial Overview

United Health Group is currently trading at $381 (as of May 14th). Over the past five years, the stock has only gained 6%, meaning today’s sharp decline could present a strong entry point for value investors.

Key Figures:

This is a major industry leader with historically strong financials, so let’s break down the numbers further.

Revenue Growth

United Health Group has shown consistent double-digit growth, averaging 10-11% over the past decade.

In recent years, we’ve seen some single-digit growth—for example, 8.9% in 2020—but this hasn’t been concerning given the company’s overall trajectory.

Margins & Profitability

Margins have hovered around 23%, declining slightly to 21% over the past 12 months.

While this isn’t a major red flag, it could indicate cost pressures affecting profitability.

Net income tells a similar story. The company posted a 35% decline last year, but the trailing 12 months show a rebound to $22.1 billion, suggesting momentum is returning.

Profitability Over Time:

It’s important to remember that healthcare isn’t a high-growth sector—this isn’t a new disruptor but rather an industry leader maintaining its position.

Free Cash Flow Stability

United Health Group’s free cash flow growth has remained modest in recent years, showing a 2.7% growth rate over the past three years and 5.9% over five years.

While there have been three down years, the latest data suggests a recovery back to its trend, aligning with the company’s net profit trajectory.

Debt & Leverage

Debt has increased from $25.4 billion in 2015 to $72.3 billion, but the company maintains strong leverage.

Key metric:

United Health Group demonstrates healthy debt management, ensuring its balance sheet remains strong while maintaining free cash flow.

Dividend Growth: A Powerhouse for Investors

The company offers a solid 2.72% dividend yield, equating to a $2.10 per quarter payout.

What makes this dividend stand out?

This growth positions United Health Group as a prime dividend investment, especially for those starting late in investing.

Compounding Wealth

Investors benefit from:

If a company consistently raises dividends, investors essentially get a yearly “pay raise”—something most jobs don’t offer.

Share Buybacks & Value Creation

United Health Group has aggressively repurchased shares, reducing shares outstanding consistently over the years.

Despite a slight increase in the last year, the overall trend remains strongly downward, meaning existing shares become more valuable.

For a mature company, this share reduction strategy enhances investor value, complementing dividend payouts.

Return on Capital & Cost Efficiency

The company excels in capital efficiency, creating value at a strong spread:

This indicates smart management decisions, ensuring capital is used effectively.

Valuation: A Major Upside Potential

Based on its historical averages, United Health Group’s valuation suggests significant upside:

Currently trading at $381, the intrinsic value estimate falls around $516, translating to an upside of 67%.

A fair range would be $490-$542, reinforcing the view that this stock remains undervalued.

Directional Investing vs. Exact Targets

While exact valuation figures are never guaranteed, directionally assessing whether a stock is overvalued, fairly valued, or undervalued is key to smart investing.

United Health Group, based on its financial health, dividend strength, and share buybacks, presents a compelling case for investment.

Conclusion: United Health Group’s Resilience Amid Market Uncertainty

United Health Group has faced significant volatility in recent months, with its stock plunging 48% due to external concerns. However, this decline does not necessarily indicate a deterioration in business fundamentals.

One of the key reassurances for investors is the leadership transition. While CEO changes often spark uncertainty, the incoming executive was previously the CEO and has remained closely connected to the business as board chairman. This level of familiarity reduces risk and suggests the company is not entering uncharted territory.

Market Overreaction vs. Reality

The scale of the stock’s decline raises an important question: Has United Health Group actually become 48% worse in a matter of months? The answer, backed by financial metrics and historical trends, is likely no. Investors often overreact to negative headlines, creating deep buying opportunities for those who assess long-term fundamentals rather than short-term price swings.

United Health Group remains a dominant force in healthcare, with a strong financial foundation, a consistent dividend payout, and a historically stable business model.

A Dow 30 Stock with Staying Power

This isn’t a speculative high-growth company—it’s an industry leader with established market dominance. Its membership in the Dow 30 and S&P 500 signals strong institutional backing, meaning most shareholders are unlikely to sell off completely despite short-term news cycles.

Why This Could Be a Buying Opportunity

For those seeking healthcare industry exposure, this moment presents one of the most attractive entry points in years. The stock’s price is now only 6% above where it was five years ago, reinforcing the long-term value proposition.

The company’s double-digit revenue growth—uncommon among mature businesses—further solidifies its investment appeal. Many large companies settle into mid-single-digit growth at this stage, yet United Health Group continues to grow at over 10% per year, proving its ability to expand efficiently even in a highly regulated industry.

Final Takeaway

Investors should approach this situation with pragmatic patience. The stock may continue experiencing short-term fluctuations, but United Health Group’s fundamentals remain intact. With its dividend growth, share repurchases, financial stability, and market leadership, the company is well-positioned to rebound over time.

This isn’t just about reacting to headlines—it’s about understanding the broader picture. Giants do fall, but they rarely stay down.

For those focused on long-term investing, United Health Group is a stock worth watching closely, if not outright considering as a potential addition to a portfolio.

Stocks Similar to UNH

https://youtu.be/IPISO_RzfLY?si=a-XrAzTEmSJKyDy6