Uber Technologies Inc. (NYSE: UBER) is currently trading at $72.91 per share. Over the past year, the stock has experienced volatility, with highs reaching $87 and lows dropping to $54. However, in the last five years, Uber has surged 160%, significantly outperforming the S&P 500.

This analysis will evaluate Uber’s most recent earnings and use three valuation methods—Discounted Free Cash Flow (DCF), Comparable Company Model, and the Ben Graham Formula for Intrinsic Value—to determine if Uber is a buy or sell.

Financial Overview

Stock Metrics

- Current price: $73 per share

- Market cap: $153 billion

- P/E ratio: 15.9 (well below the market average of 26.9)

- Earnings per share (EPS): $4.58

- Beta: 1.37 (indicating above-average volatility)

Analysts currently rate Uber as a buy, with a price target of around $88 per share. However, Uber does not pay dividends, so that won’t factor into our analysis.

Revenue Growth & Profitability

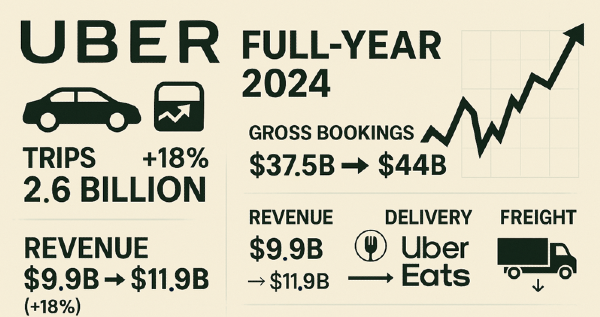

Uber reported full-year 2024 revenue of just under $44 billion, marking an all-time high. The company has seen exponential growth, aside from a temporary dip in 2020 due to the pandemic.

In its most recent earnings report:

- Trips increased 18%, reaching 2.6 billion

- Gross bookings grew from $37.5 billion to $44 billion

- Revenue climbed from $9.9 billion to $11.9 billion

Breaking it down further:

- Mobility (ride-sharing): $19.3 billion → $22.8 billion (+18%)

- Delivery (Uber Eats): $17 billion → $20.1 billion (flat growth)

- Freight: Slight decline

Uber also had its most profitable year ever, reporting $9.86 billion in net income and $6.9 billion in free cash flow.

Valuation Methods

Discounted Free Cash Flow (DCF) Model

DCF estimates Uber’s fair value based on projected free cash flow. Analysts expect revenue to hit $50-58 billion in the coming years, but assuming 15% growth, Uber’s valuation lands at $76 per share—fairly valued.

Ben Graham’s Intrinsic Value Formula

Ben Graham’s model suggests Uber has 31% expected growth, placing its fair value at $150 per share—indicating a strong buy.

Comparable Company Model

Comparing Uber to Lyft (LYFT), DoorDash (DASH), and Airbnb (ABNB):

- Uber has the highest revenue and second-highest growth rate (only beaten by DoorDash).

- Net income and margins show Uber leading its competitors.

- Price-to-sales and price-to-book ratios indicate relative undervaluation compared to Lyft and DoorDash.

Using this model, Uber appears significantly undervalued, with estimates ranging from $76 to $300 per share, depending on which competitor it’s benchmarked against.

Conclusion: Buy or Sell?

Given its strong fundamentals, growing profitability, and undervaluation across multiple models, Uber presents an attractive investment opportunity. The DCF model suggests fair valuation at $76, while the Ben Graham formula and comparable analysis indicate a much higher upside.

Investors should weigh Uber’s rapid growth against potential macroeconomic risks, but at $73 per share, the stock remains a compelling buy.

| Company |

Symbol |

Why It's Better Than Uber |

| Lyft |

LYFT |

Lyft focuses more on North American markets, potentially offering better regional stability and growth. |

| DoorDash |

DASH |

DoorDash dominates food delivery, a sector with strong consumer demand and less regulatory scrutiny than ridesharing. |

| Grab |

GRAB |

Grab has a diversified business model, including financial services and food delivery, making it less reliant on ride-hailing. |

| DiDi Global |

DIDIY |

DiDi has a strong presence in China, a massive market with high demand for ride-hailing services. |

| Avis Budget Group |

CAR |

Avis Budget benefits from the rental car industry, which has seen strong post-pandemic recovery and profitability. |

https://youtu.be/zCXwkgdXgD4?si=wGvfQGH1Af7EWbDw

Uber Technologies Inc. (NYSE: UBER) is currently trading at $72.91 per share. Over the past year, the stock has experienced volatility, with highs reaching $87 and lows dropping to $54. However, in the last five years, Uber has surged 160%, significantly outperforming the S&P 500.

This analysis will evaluate Uber’s most recent earnings and use three valuation methods—Discounted Free Cash Flow (DCF), Comparable Company Model, and the Ben Graham Formula for Intrinsic Value—to determine if Uber is a buy or sell.

Financial Overview

Stock Metrics

Analysts currently rate Uber as a buy, with a price target of around $88 per share. However, Uber does not pay dividends, so that won’t factor into our analysis.

Revenue Growth & Profitability

Uber reported full-year 2024 revenue of just under $44 billion, marking an all-time high. The company has seen exponential growth, aside from a temporary dip in 2020 due to the pandemic.

In its most recent earnings report:

Breaking it down further:

Uber also had its most profitable year ever, reporting $9.86 billion in net income and $6.9 billion in free cash flow.

Valuation Methods

Discounted Free Cash Flow (DCF) Model

DCF estimates Uber’s fair value based on projected free cash flow. Analysts expect revenue to hit $50-58 billion in the coming years, but assuming 15% growth, Uber’s valuation lands at $76 per share—fairly valued.

Ben Graham’s Intrinsic Value Formula

Ben Graham’s model suggests Uber has 31% expected growth, placing its fair value at $150 per share—indicating a strong buy.

Comparable Company Model

Comparing Uber to Lyft (LYFT), DoorDash (DASH), and Airbnb (ABNB):

Using this model, Uber appears significantly undervalued, with estimates ranging from $76 to $300 per share, depending on which competitor it’s benchmarked against.

Conclusion: Buy or Sell?

Given its strong fundamentals, growing profitability, and undervaluation across multiple models, Uber presents an attractive investment opportunity. The DCF model suggests fair valuation at $76, while the Ben Graham formula and comparable analysis indicate a much higher upside.

Investors should weigh Uber’s rapid growth against potential macroeconomic risks, but at $73 per share, the stock remains a compelling buy.

https://youtu.be/zCXwkgdXgD4?si=wGvfQGH1Af7EWbDw