Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU

Is Western Alliance Bank Stock a Buy?

Western Alliance Bank (WAL) is projected to be a strong buy with a projected annual return (PAR) value of 19.3%. The bank has a terrific return on average assets (ROAA) of 1.86% - an industry high. Sales, assets, and profit have all grown the last 10 years, and it is expected that this trend will continue for the next 5 years.

The Stock Selection Guide for Western Alliance Bank

I've had a lot of respect for this bank for a long time. This is Western Alliance Bank (WAL).

A stock selection guide for Western Alliance Bank

I'll start with the visual analysis. It's just about as pretty as you can make it. Our tools from BetterInvesting™ allow you to put assets right onto the graph. Assets are the

Lifeblood of any asset-based company and that would include all banks, insurance companies, and brokerage firms. The aqua colored line is the asset growth which you like to see roughly parallel with sales growth.

Read More: Why Book Value per Share is Important

The traditional sales growth line is the green line. You like to see both the assets line and sales line to be roughly parallel with the blue line which is the earnings per share line.

if you look down at the numbers at the bottom, I've included the growth rates. You get sales growth at 21%, you get asset growth at 22.7%, and you get earnings growth at 25.7%. That's pretty close in my book for me to say that these trends are all up straight and parallel.

Why should sales and profit lines be up, straight, and parallel? Read How to Use a Stock Selection Guide to learn more.

The bank's been doing pretty well. Those future dots, which are projections thru 2022 to 2024, are coming from The Morning Star data that is provided by BetterInvesting™ and you'll notice that my projections are leaning on those dots quite a bit to help me set forecast numbers. I'm very comfortable with that 20% sales growth; especially since the 10-year growth rate has been 21%. I probably could raise that historical EPS number to 20% growth but for this exercise I'm going to keep it to what I view as conservative at 15% even though the ten-year average has been at about 25%. Note that the most recent earnings growth was 5% so we'll see what happens as the years progress.

Western Alliance Bank Rankings

This looks to be a very strong visual analysis. When I see a strong visual analysis like this, I like to go to the company's website to take a detailed look at the company’s profile and leadership.

I've chosen just a couple of representative slides from the company website and investor presentation. They rank very high on Forbes “America's best banks”. In fact, for two of the last three years they've ranked as the number one bank by a number of different agencies that rank regional banks. You'll find Western Alliance Bank near the top of almost any one of the different rankings you might pull off the internet.

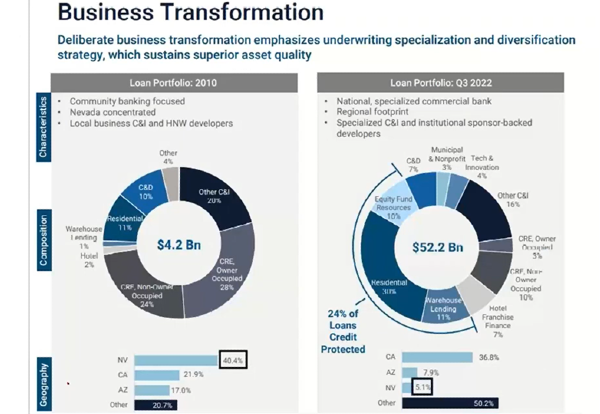

Western Alliance is in fact a family of banks. You won't find any banks actually tagged as Western Alliance, but you will find a large number of banks with the brands that have regional brand recognition like Alliance Bank of Arizona, Bank of Nevada, and Torrey Pines Bank.

Western Alliance Business Growth

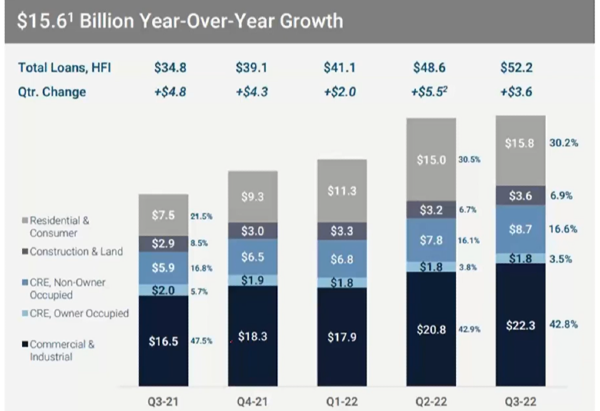

They began their history in Nevada and they had, and still have, a fairly simple business model. The bank makes money by loaning it to people and charging them various interest rates. You can see that a little bit more than 40% of their business comes from commercial and Industrial loans and about 30% of their business comes from residential and consumer mortgages. That leaves the rest in the middle there for construction loans.

Commercial real estate (CRE) owner occupied and non-owner occupied make up roughly 20% of the loans as of Q3, 2022. These loans are for commercial buildings like stores and restaurants for example. So Western Alliance Bank is a very traditional bank that loans out money to very traditional areas.

Back in 2010, over 40% of their business was coming from the state of Nevada. As of the third quarter of 2022, you see that the business is much more diversified and now about 37% of their business is coming from the state of California. The bank is still conducting a significant amount of business in Arizona and Nevada, but since 2010 they have expanded into real estate that is outside their traditional three-state area. In fact, about half of their business is now outside of their traditional California, Arizona, and Nevada region.

Western Alliance Bank Return on Average Assets

Western Alliance Bank Return on Average Assets

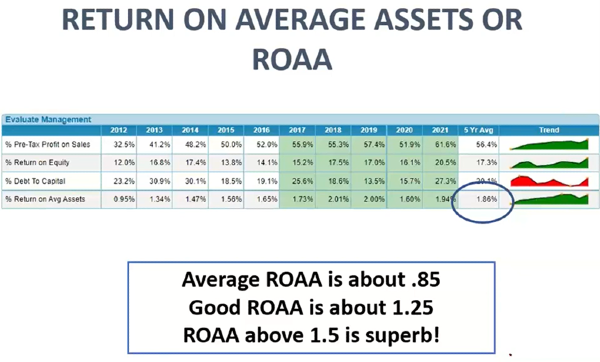

Percent return on average assets (ROAA) is an important value to research when analyzing a bank. I use a percent return on average assets number that comes in our data feed from Morningstar. I've been taught by folks that are in the know that this is a very sensitive number and it's a number that can tell you a lot of good information about a bank.

A solid ROAA for a bank is 0.85%. If ROAA can be pushed up to about 1.25%, you're looking at a good solid bank. And when you can push that number up to 1.5%, you're looking at an outstanding bank! Western Alliance bank has pushed its ROAA significantly past this threshold and has a five-year average ROAA of 1.86%!

This bank is one of a very few banks that manages to be ranked consistently in this superb category. This number has more meaning the longer a bank can hold itself at these very high levels. If you go back in time, you'll notice that ROAA for this bank is about 1.5% starting in 2014. The bank has been able to keep its ROAA above 1.5% through 2021. This is an impressive metric, and I would challenge you to find more than a handful of other banks that are able to maintain this kind of return on average assets over this length of time.

Western Alliance Bank Analysis Results

The stock market hates Banks right now. They're trading at 52-week lows. If you follow the financial sector you might know that recently most of the money center banks reported their earnings and finally we began to see some price increases and a little bit of optimism about the business models of these big money center banks.

Money center banks raise funds from domestic and international money markets and rely less on depositors for funds.

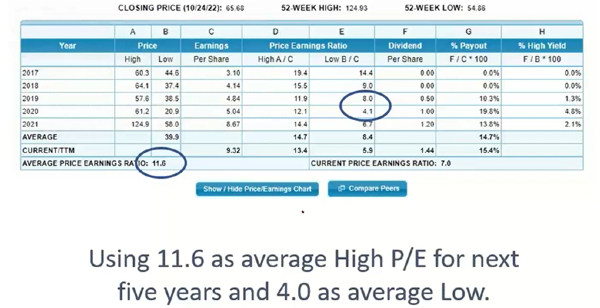

However, Wall Street still has very little optimism when it comes to simple, old-fashioned Banks. But think about it, Western Alliance Bank has been able to make good money with zero percent interest. What might they be able to do as interest rates move to 2.5% or 3.5%? That's where the banks are headed, and I'd like to get in near the bottom. I'm very comfortable buying a bank with a P/E ratio somewhere beneath 10. And I'm very comfortable at coming up with this stock’s potential return if I assume the P/E ratios are going to be a little bit challenged.

Read More: How to Interpret the Price to Earnings Ratio

I believe the five-year average P/E ratio of 11.6 was a challenged high P/E ratio. So, I took this average and set it as the high P/E ratio for the next five years. I then took the lowest of the low P/E ratios of 4.1 and set it as the average low for the next five years. That is giving me an average P/E ratio of just a little bit over 7. So being conservative on my estimates, I'm saying that the estimated future P/E ratio is just fairly average for the next five years to conduct my analysis.

But I would fully anticipate P/E ratio expansion to happen quite quickly as this bank became extremely more profitable as it had been in the past.

And even with these very low P/E ratio projections and very conservative projected earnings

per share (EPS) growth at 15%, I'm expecting the projected annual return (PAR) value for Western Alliance to be up around 19.3%. I get great validation from Manifest Investing that's calling for the par value to be at 18.9%.

Buying really great quality companies with a 95 quality rating and prices that I consider are low enough to give me high par values is what makes me money in my portfolio so I’m adding to my position.

Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU

I/we have a position in an asset mentioned

Check out the companion video to this article: https://www.youtube.com/watch?v=cBwigNigYtU

Is Western Alliance Bank Stock a Buy?

Western Alliance Bank (WAL) is projected to be a strong buy with a projected annual return (PAR) value of 19.3%. The bank has a terrific return on average assets (ROAA) of 1.86% - an industry high. Sales, assets, and profit have all grown the last 10 years, and it is expected that this trend will continue for the next 5 years.

The Stock Selection Guide for Western Alliance Bank

I've had a lot of respect for this bank for a long time. This is Western Alliance Bank (WAL).

A stock selection guide for Western Alliance Bank

I'll start with the visual analysis. It's just about as pretty as you can make it. Our tools from BetterInvesting™ allow you to put assets right onto the graph. Assets are the Lifeblood of any asset-based company and that would include all banks, insurance companies, and brokerage firms. The aqua colored line is the asset growth which you like to see roughly parallel with sales growth.

The traditional sales growth line is the green line. You like to see both the assets line and sales line to be roughly parallel with the blue line which is the earnings per share line.

if you look down at the numbers at the bottom, I've included the growth rates. You get sales growth at 21%, you get asset growth at 22.7%, and you get earnings growth at 25.7%. That's pretty close in my book for me to say that these trends are all up straight and parallel.

The bank's been doing pretty well. Those future dots, which are projections thru 2022 to 2024, are coming from The Morning Star data that is provided by BetterInvesting™ and you'll notice that my projections are leaning on those dots quite a bit to help me set forecast numbers. I'm very comfortable with that 20% sales growth; especially since the 10-year growth rate has been 21%. I probably could raise that historical EPS number to 20% growth but for this exercise I'm going to keep it to what I view as conservative at 15% even though the ten-year average has been at about 25%. Note that the most recent earnings growth was 5% so we'll see what happens as the years progress.

Western Alliance Bank Rankings

This looks to be a very strong visual analysis. When I see a strong visual analysis like this, I like to go to the company's website to take a detailed look at the company’s profile and leadership.

Source: Western Alliance Bank Investor Relations

I've chosen just a couple of representative slides from the company website and investor presentation. They rank very high on Forbes “America's best banks”. In fact, for two of the last three years they've ranked as the number one bank by a number of different agencies that rank regional banks. You'll find Western Alliance Bank near the top of almost any one of the different rankings you might pull off the internet.

Western Alliance is in fact a family of banks. You won't find any banks actually tagged as Western Alliance, but you will find a large number of banks with the brands that have regional brand recognition like Alliance Bank of Arizona, Bank of Nevada, and Torrey Pines Bank.

Western Alliance Business Growth

Source: Western Alliance Bank Investor Relations

They began their history in Nevada and they had, and still have, a fairly simple business model. The bank makes money by loaning it to people and charging them various interest rates. You can see that a little bit more than 40% of their business comes from commercial and Industrial loans and about 30% of their business comes from residential and consumer mortgages. That leaves the rest in the middle there for construction loans.

Commercial real estate (CRE) owner occupied and non-owner occupied make up roughly 20% of the loans as of Q3, 2022. These loans are for commercial buildings like stores and restaurants for example. So Western Alliance Bank is a very traditional bank that loans out money to very traditional areas.

Source: Western Alliance Bank Investor Relations

Back in 2010, over 40% of their business was coming from the state of Nevada. As of the third quarter of 2022, you see that the business is much more diversified and now about 37% of their business is coming from the state of California. The bank is still conducting a significant amount of business in Arizona and Nevada, but since 2010 they have expanded into real estate that is outside their traditional three-state area. In fact, about half of their business is now outside of their traditional California, Arizona, and Nevada region.

Western Alliance Bank Return on Average Assets

Western Alliance Bank Return on Average Assets

Percent return on average assets (ROAA) is an important value to research when analyzing a bank. I use a percent return on average assets number that comes in our data feed from Morningstar. I've been taught by folks that are in the know that this is a very sensitive number and it's a number that can tell you a lot of good information about a bank.

A solid ROAA for a bank is 0.85%. If ROAA can be pushed up to about 1.25%, you're looking at a good solid bank. And when you can push that number up to 1.5%, you're looking at an outstanding bank! Western Alliance bank has pushed its ROAA significantly past this threshold and has a five-year average ROAA of 1.86%! This bank is one of a very few banks that manages to be ranked consistently in this superb category. This number has more meaning the longer a bank can hold itself at these very high levels. If you go back in time, you'll notice that ROAA for this bank is about 1.5% starting in 2014. The bank has been able to keep its ROAA above 1.5% through 2021. This is an impressive metric, and I would challenge you to find more than a handful of other banks that are able to maintain this kind of return on average assets over this length of time.

Western Alliance Bank Analysis Results

The stock market hates Banks right now. They're trading at 52-week lows. If you follow the financial sector you might know that recently most of the money center banks reported their earnings and finally we began to see some price increases and a little bit of optimism about the business models of these big money center banks.

However, Wall Street still has very little optimism when it comes to simple, old-fashioned Banks. But think about it, Western Alliance Bank has been able to make good money with zero percent interest. What might they be able to do as interest rates move to 2.5% or 3.5%? That's where the banks are headed, and I'd like to get in near the bottom. I'm very comfortable buying a bank with a P/E ratio somewhere beneath 10. And I'm very comfortable at coming up with this stock’s potential return if I assume the P/E ratios are going to be a little bit challenged.

I believe the five-year average P/E ratio of 11.6 was a challenged high P/E ratio. So, I took this average and set it as the high P/E ratio for the next five years. I then took the lowest of the low P/E ratios of 4.1 and set it as the average low for the next five years. That is giving me an average P/E ratio of just a little bit over 7. So being conservative on my estimates, I'm saying that the estimated future P/E ratio is just fairly average for the next five years to conduct my analysis.

But I would fully anticipate P/E ratio expansion to happen quite quickly as this bank became extremely more profitable as it had been in the past.

And even with these very low P/E ratio projections and very conservative projected earnings per share (EPS) growth at 15%, I'm expecting the projected annual return (PAR) value for Western Alliance to be up around 19.3%. I get great validation from Manifest Investing that's calling for the par value to be at 18.9%. Buying really great quality companies with a 95 quality rating and prices that I consider are low enough to give me high par values is what makes me money in my portfolio so I’m adding to my position.

Check out the companion video to this article: https://www.youtube.com/watch?v=cBwigNigYtU

I/we have a position in an asset mentioned