Key Notes

- Littelfuse is a circuit component manufacturer

- The company is a potential buy, with strong sales growth projections

- Sales growth is being buoyed by foreign sales growth and the eMobility sector

What is Littelfuse Inc (LFUS)?

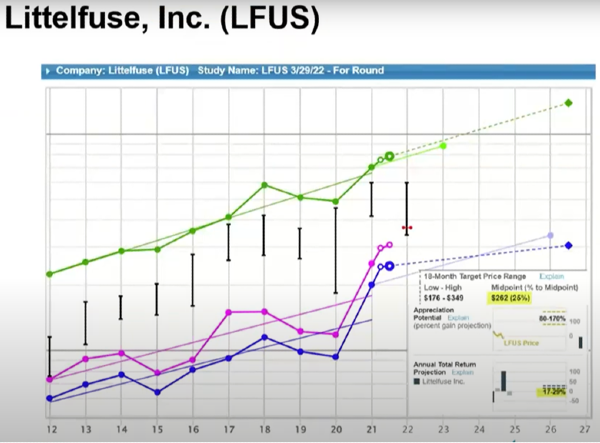

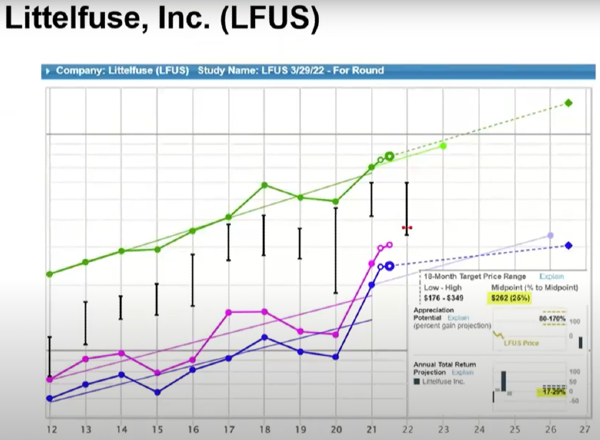

Littelfuse has a strong consistency in sales with just a little bit of volatility as you can see in 2019 and 2020. Littelfuse is an industrial company although they're now rated as a technology company because, of course, more things get technological in our world. Littelfuse sells circuit breakers, hence the name. Their roots are in electric fuses and over the years since being founded in 1927 that's the business that they have stuck with. circuit breakers have gotten more and more complex and installed into more and more complex devices. As we'll see as we review the company, notice that value line, at October 2022’s price, had a pretty optimistic potential return of 17% to 29% over the next three to five years and a 25% return in the shorter term.

Read More: The Top Stocks Analyzed with a Stock Selection Guide

How to Screen for It

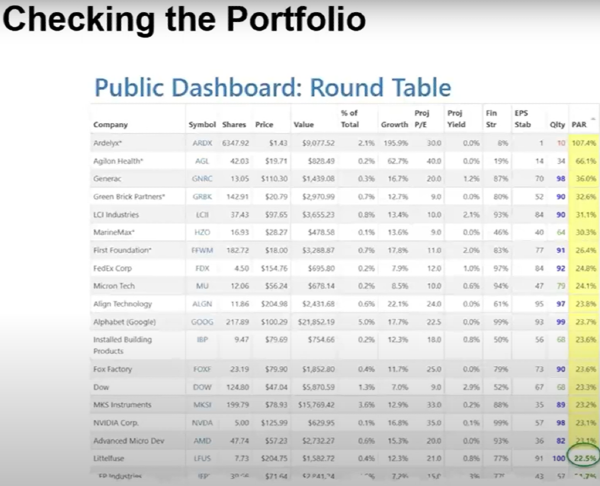

I found Littelfuse Inc. by taking a look at the round table portfolio and seeing what is attractive there. I ranked by par and behold! The highest, sweet spot company is LFUS, although some of those yellow companies that are just above the sweet spot are high quality and certainly deserves some attention. I jumped in with Littelfuse Inc. even with other great picks like MKS instruments on the list.

Little Fuse Industry Comparison

Above is a quick industry study and comparison ranked by par. You see it's the

second highest ranked company in the industry and has excellent quality and financial strength compared to the first ranked LSI Industries.

Ranking by quality again, LFUS is right among the top three stocks. I like looking for the best among the best in quality and again you could see among these excellent Quality Companies, Littelfuse Inc. is the best buying opportunity at the time based on par.

About the Company Littelfuse Inc.

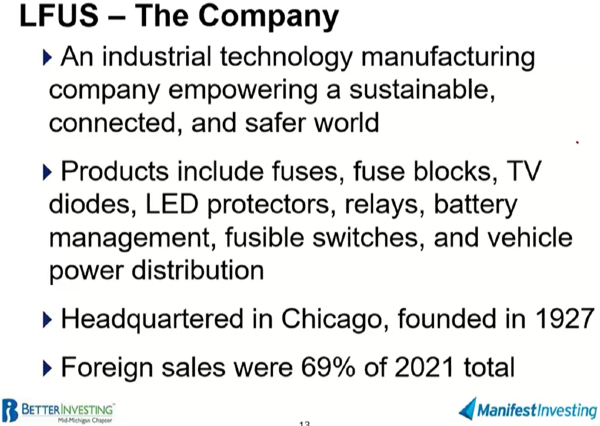

LFUS sells fuses, fuse blocks, diodes, LED protectors, and various relays which again is power management, battery management, and switches. What they're really starting to get more into and looking at for a potential high growth area for the company going forward is vehicle power distribution. Littelfuse Inc. is looking to have their components in Individual EVS electric vehicles, battery infrastructure, and batteries in the vehicles as well as the infrastructure to support recharging. Notice that foreign sales

are a significant share of their sales. In fact, well over 50% of Littelfuse’s sales in 2021 were outside the United States.

Littelfuse’s Environmental, Sustainability, and Governance Policies

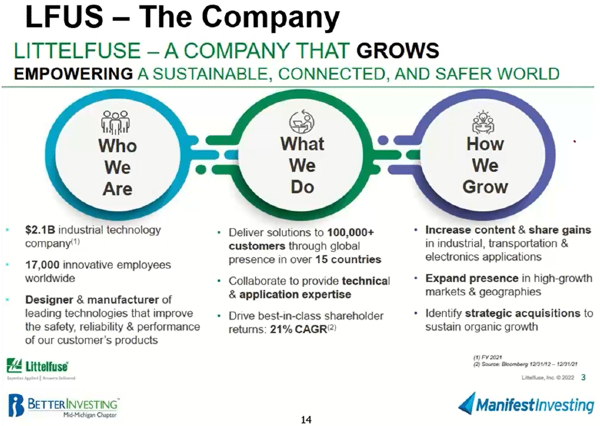

This slide from the company's investor presentation gives you a little

bit of who they are, what they do, and how they plan to grow the company even

though it has been around since 1927. The company does grow through Acquisitions as well as seeking to cross-sell and grow internally. If you do the math on what the company's projecting its future growth is in the mid-double digit or low to mid-double digits. The company is predicting about half of that to be organic growth which is internal and about half through acquisitions.

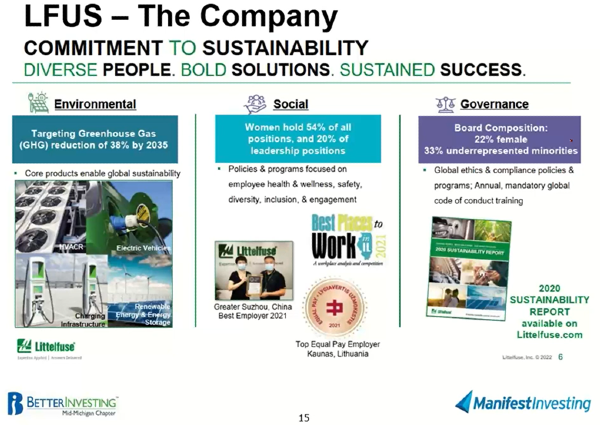

Littelfuse likes to focus on their sustainability initiatives and they mention it on the slide above. I’ve noticed it is getting to be a bit trendy in some respects for companies to talk about ESG (the environmental, social and governance issues) but here is their ESG outlook for the company which I think is something that merits taking a look at.

Read More: The Top ESG Stocks to Buy Now

Littelfuse’s Market Segments

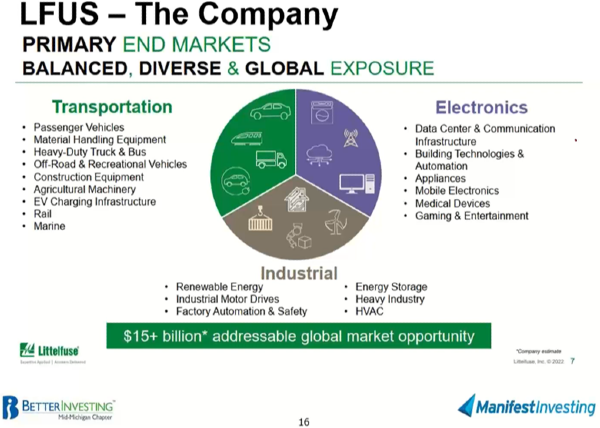

as I mentioned, here are Littelfuse’s end markets. You can see about a third is in the transportation area which is getting into the EV charging infrastructure as well as more traditional longer-term markets in transportation such as rail and marine vehicles. But Littelfuse is just about in all types of transportation that you can think of. They also are in multiple industrial arenas including HVAC, factory automation, motor drives and even renewables. The piece that gets more into the technology side is the electronics segment which includes data centers and communication infrastructure that touch just about all aspects of our lives. In electronics, they are providing circuit breakers and switches, so it’s likely a littelfuse product touches all of our lives.

LFUS in the Car Market

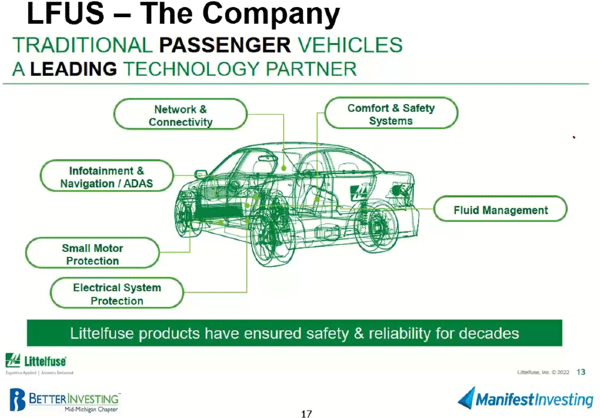

Here some details on where Littelfuse fits into traditional passenger vehicles that again has then grown into the electronic vehicle and the battery charging infrastructure. There strategic acquisitions have adopted to grow in these new markets while building upon their existing markets

One disclaimer is I don't own a full EV, but I do own a plug-in hybrid EV so maybe I'm biased a little bit in that area.

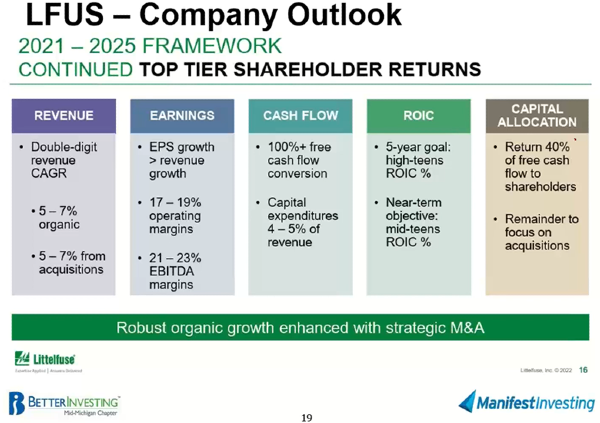

As I had mentioned earlier you can see they're projecting between 10% and 14% growth in revenue over the next five years. This outlook goes back to 2021 thru 2025. Littelfuse boils it down nicely at the very bottom of their slide. Their robust

organic growth enhanced with strategic mergers and acquisitions is focused on a high return on invested capital. The company has a strong cash flow and is returning a good chunk of the cash flow to its shareholders through dividends and buy backs.

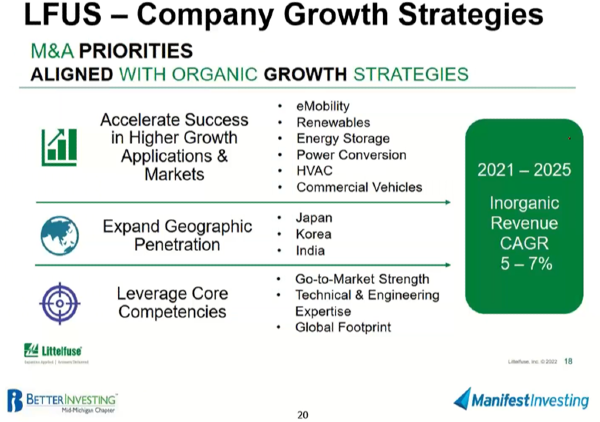

LFUS Growth Strategy

Littelfuse is expanding in eMobility and energy areas while seeking to expand geographically in east and central Asia as well as India. Again, they continue to implement the same strategy as they did when the company started: build on their current expertise and leveraging what they do well.

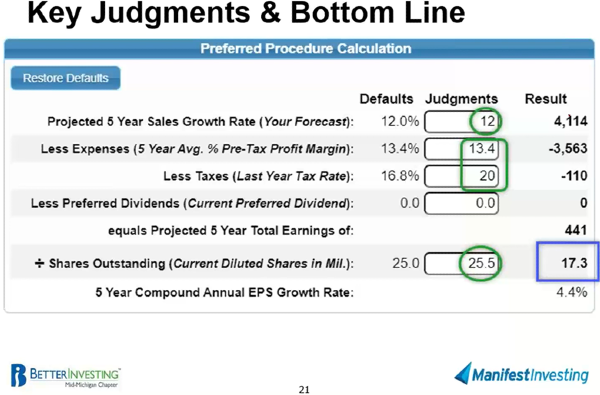

Key Judgements and Bottom Line

Here are my judgments. I chose a 12% projected growth rate which is right in the middle of the company's projected areas and right in line with the value Line and other analysts. Also, I've been relatively conservative on the margin. If you remember the first chart that showed consistent sales growth, a little bit of volatility in earnings, and pre-tax margins, I was conservative on the margin because the company, although it's a tech company, is serving industrial markets so it has a bit of industrial cyclicality to it. Hence, I've chosen to just stay with the average profit margin for the last five years being the same over the next five years. However, right now the current profit margin is more like 16% or 17% so I could be pleasantly surprised.

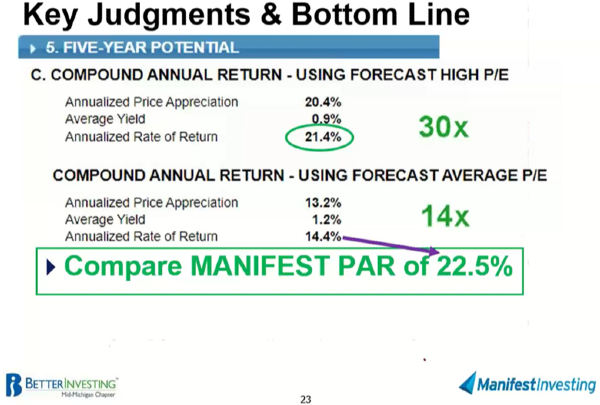

Using a high P/E ratio of 30x, it gives a potential return of 21.4%. With an average P/E ratio of 14x, my estimates suggest a potential return of 14.4%.

This article was written in partnership with Manifest Investing. Check out their monthly Round Table meeting to learn more about investing while having some fun.

Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU

Key Notes

What is Littelfuse Inc (LFUS)?

Littelfuse has a strong consistency in sales with just a little bit of volatility as you can see in 2019 and 2020. Littelfuse is an industrial company although they're now rated as a technology company because, of course, more things get technological in our world. Littelfuse sells circuit breakers, hence the name. Their roots are in electric fuses and over the years since being founded in 1927 that's the business that they have stuck with. circuit breakers have gotten more and more complex and installed into more and more complex devices. As we'll see as we review the company, notice that value line, at October 2022’s price, had a pretty optimistic potential return of 17% to 29% over the next three to five years and a 25% return in the shorter term.

How to Screen for It

I found Littelfuse Inc. by taking a look at the round table portfolio and seeing what is attractive there. I ranked by par and behold! The highest, sweet spot company is LFUS, although some of those yellow companies that are just above the sweet spot are high quality and certainly deserves some attention. I jumped in with Littelfuse Inc. even with other great picks like MKS instruments on the list.

Little Fuse Industry Comparison

Above is a quick industry study and comparison ranked by par. You see it's the second highest ranked company in the industry and has excellent quality and financial strength compared to the first ranked LSI Industries.

Ranking by quality again, LFUS is right among the top three stocks. I like looking for the best among the best in quality and again you could see among these excellent Quality Companies, Littelfuse Inc. is the best buying opportunity at the time based on par.

About the Company Littelfuse Inc.

LFUS sells fuses, fuse blocks, diodes, LED protectors, and various relays which again is power management, battery management, and switches. What they're really starting to get more into and looking at for a potential high growth area for the company going forward is vehicle power distribution. Littelfuse Inc. is looking to have their components in Individual EVS electric vehicles, battery infrastructure, and batteries in the vehicles as well as the infrastructure to support recharging. Notice that foreign sales are a significant share of their sales. In fact, well over 50% of Littelfuse’s sales in 2021 were outside the United States.

Littelfuse’s Environmental, Sustainability, and Governance Policies

LFUS Investor Presentation

This slide from the company's investor presentation gives you a little bit of who they are, what they do, and how they plan to grow the company even though it has been around since 1927. The company does grow through Acquisitions as well as seeking to cross-sell and grow internally. If you do the math on what the company's projecting its future growth is in the mid-double digit or low to mid-double digits. The company is predicting about half of that to be organic growth which is internal and about half through acquisitions.

LFUS Investor Presentation

Littelfuse likes to focus on their sustainability initiatives and they mention it on the slide above. I’ve noticed it is getting to be a bit trendy in some respects for companies to talk about ESG (the environmental, social and governance issues) but here is their ESG outlook for the company which I think is something that merits taking a look at.

Littelfuse’s Market Segments

LFUS Investor Presentation

as I mentioned, here are Littelfuse’s end markets. You can see about a third is in the transportation area which is getting into the EV charging infrastructure as well as more traditional longer-term markets in transportation such as rail and marine vehicles. But Littelfuse is just about in all types of transportation that you can think of. They also are in multiple industrial arenas including HVAC, factory automation, motor drives and even renewables. The piece that gets more into the technology side is the electronics segment which includes data centers and communication infrastructure that touch just about all aspects of our lives. In electronics, they are providing circuit breakers and switches, so it’s likely a littelfuse product touches all of our lives.

LFUS in the Car Market

LFUS Investor Presentation

Here some details on where Littelfuse fits into traditional passenger vehicles that again has then grown into the electronic vehicle and the battery charging infrastructure. There strategic acquisitions have adopted to grow in these new markets while building upon their existing markets

One disclaimer is I don't own a full EV, but I do own a plug-in hybrid EV so maybe I'm biased a little bit in that area.

LFUS Investor Presentation

As I had mentioned earlier you can see they're projecting between 10% and 14% growth in revenue over the next five years. This outlook goes back to 2021 thru 2025. Littelfuse boils it down nicely at the very bottom of their slide. Their robust organic growth enhanced with strategic mergers and acquisitions is focused on a high return on invested capital. The company has a strong cash flow and is returning a good chunk of the cash flow to its shareholders through dividends and buy backs.

LFUS Growth Strategy

LFUS Investor Presentation

Littelfuse is expanding in eMobility and energy areas while seeking to expand geographically in east and central Asia as well as India. Again, they continue to implement the same strategy as they did when the company started: build on their current expertise and leveraging what they do well.

Key Judgements and Bottom Line

Here are my judgments. I chose a 12% projected growth rate which is right in the middle of the company's projected areas and right in line with the value Line and other analysts. Also, I've been relatively conservative on the margin. If you remember the first chart that showed consistent sales growth, a little bit of volatility in earnings, and pre-tax margins, I was conservative on the margin because the company, although it's a tech company, is serving industrial markets so it has a bit of industrial cyclicality to it. Hence, I've chosen to just stay with the average profit margin for the last five years being the same over the next five years. However, right now the current profit margin is more like 16% or 17% so I could be pleasantly surprised.

Using a high P/E ratio of 30x, it gives a potential return of 21.4%. With an average P/E ratio of 14x, my estimates suggest a potential return of 14.4%.

This article was written in partnership with Manifest Investing. Check out their monthly Round Table meeting to learn more about investing while having some fun.

Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU