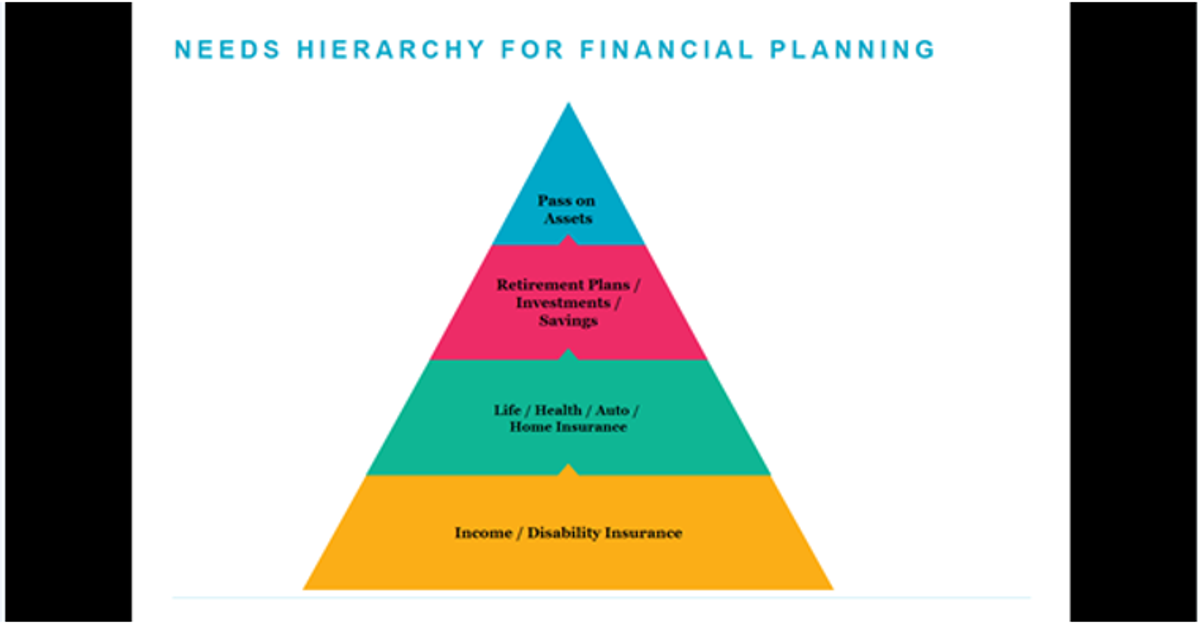

What is Insurance?

Actionable Items for You:

- Insurance is a big part of financial planning - you should have enough to secure your family financially in the event of an accident.

- Get at us if you want some help seeing if you have enough coverage to reduce risk.

Insurance coverage is a funny thing. Everyone seems to have some sort of idea what it is, most think they need it but not urgently, everyone has it for their car, and some have way too much. But what is insurance coverage, really?

It’s kinda right there in the name. Insurance can cover things like health, property & casualty insurance, life insurance, and insurance against disability. It all boils down to one thing - risk. When you have a family or loved ones that depend on your income, you need to make sure there’s a plan in place if you were to have an accident or no longer be able to work.

That’s the main point here - there is a high priority for you to get some basic coverage to secure you and your family from financial hardship if and when something terrible happens. It might not seem like an urgent need, but everyone thinks the same until an accident happens. It’s a big part of financial planning - emphasis on planning.

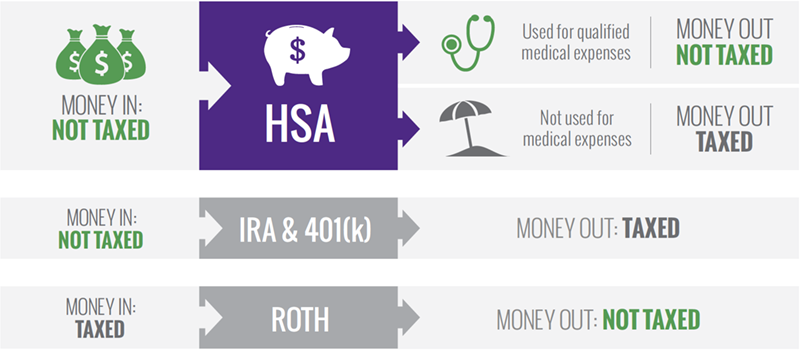

HSA Benefits

The top benefits of a Health Savings Account (HSA) and why you need to know.

Actionable Items for You:

- A Health Savings Account (HSA) is a really powerful way to build wealth. It has triple tax benefits that you should be aware of.

- The catch is that you have to use the account to spend on qualified medical expenses - but it’s not that big of a catch for the benefits.

Do you want not single, not double, but TRIPLE tax advantages in your savings account? If you said yes, keep reading. If no… maybe we weren’t clear enough.

Today we’re talking about Health Savings Accounts or HSAs. They're one of the most tax-advantaged accounts that the IRS will allow you to save in, as they have massive benefits, provided the account holder follows all the rules properly. While some accounts tax you when you put funds into an account, after you pay income tax or withdraw funds, HSAs are just built differently. Here are the top 3 benefits.

1. Contributions are Tax-Free.

Some accounts (like a Roth 401k or Roth IRA) are taxed before you put funds in, but then the money is not taxed when spent from the account. With an HSA, though, funds are not taxed before saving - kind of like a traditional 401k or IRA.

2. Growth is Tax-Free.

When the funds are inside an HSA, growth is tax-free - this has massive compounding effects long-term. You can also invest in growth assets like stocks or ETFs, and they can compound your future without paying Uncle Sam.

3. Distributions are Tax-Free.

So the catch with the traditional 401k or the IRA is that, while contributions are tax-free, withdrawals are taxable. The third tax advantage of HSAs is huge, in that funds spent from an HSA are not taxed - as long as they are spent on qualified medical expenses. You can still use the funds for other things if you need to, but hold off using an HSA for a new car. Use this account for those doctor visits or prescription eyeglasses instead.

That there is the holy trifecta of investment savings, and if you’re not taking advantage of it, you’re missing out. You have to know the game to play it, and that’s where we can help you.

Want some help finding the right HSA for you? Schedule an Intro Call (https://calendly.com/freeman-intro-call/30min?month=2021-05), a no-obligation consultation with one of our team members.

Shopping for Insurance

Source: Hawley & Associates

Actionable Items for You:

It’s probably been a while since you shopped for your home or auto insurance. You might want to get some quotes to lower your spend.

There are a few ways to make this ‘shopping’ experience go quite smoothly and efficiently - we talk about them below.

When was the last time you shopped for your auto or homeowners insurance? We recommend shopping for new property & casualty insurance about every year or two, which many will put off or simply keep using the same insurer. Not doing so can lose you big bucks, as you may be able to snag some discounts without much work. When looking around:

Get quotes from at least three insurers.

Ask about discounts and savings, but pay attention to the overall price. A company that offers few discounts still may have lower premiums.

Choose a company with a good service rating. You want to rely on them when you need them.

Ask your friends and family about their carriers and service experiences.

Drive safely.

In most circumstances, your driving record (violations, accidents, claims) causes your auto insurance premiums to increase. However, you may not have had any incidents and find that when you get a notice from your insurance company about the renewal, your policy’s premium has increased. Yes, there’s inflation on insurance, and there may be even more impact this year versus years past.

Save on Premium Costs

Here are few possible ways to reduce your premium costs:

- Make sure that your driving habits (how much you drive) are reported correctly. If you no longer commute to the office and work from home, you would want to make sure your auto insurance carrier is made aware. The amount of miles you put on the vehicle is one calculation they use to determine your rate.

- Maintain a good credit rating. Over 90% of insurance carriers use your credit rating as a factor in the premium you pay.

- Increase your deductible. An increase of your deductible (the amount you pay out of pocket for an at-fault incident) from $500 to $1000 could save you 8%-10% on your premium. If you are a low-risk driver, these savings could add up over time.

In less than 30 minutes, you can get multiple quotes either online or by picking up the phone. Being prepared with the following will help make this task even easier:

- Information for each driver in your household, including birthdays and occupations

- Information about your car, including its make, model, mileage, and vehicle

- identification number (VIN)

- Average miles driven per year

- Driving history

- Current coverage information

Life Insurance vs Life Assurance

Do you know the difference between Life Insurance and Life Assurance coverage?

Source: Free Price Compare

Actionable Items for You

- Life insurance = small payments to cover you for a certain amount of years, like when your kids finally flee the house (you might wanna add a few extra years to your expectations).

- Life assurance = higher payments, but coverage is permanent - your loved ones will get a payout at the end of your life regardless.

Life insurance.

You’ve probably heard of it. You pay a premium for a set period, and if you pass away during that period, there’s a significant payout for your loved ones. It’s pretty simple overall and akin to things like your car insurance or your home insurance - it is to ensure financial commitments you have, like providing for family or paying off mortgages or other debts, will be covered.

Most families have this type of coverage when they have young children or dependents. You can set a date in the future (like when your youngest turns 18 or another predetermined age) for when you can stop paying for the insurance. If you live past that date, you will not get a pay-out at the end of the term or refund your premiums. But that’s the point - it’s insurance against an adverse event.

None of us plan on dying before our children, but we have to be prepared for it. Life insurance is a great way to achieve security for your family. Of course, if you want to take life insurance to the next financial planning step, you might want to consider Life Assurance.

Life Assurance

Life Assurance is similar but different. Some refer to this type of coverage as a ‘whole life’ policy because, as you can probably guess, it covers you for your whole… life. Essentially, it does the same as life insurance but you have a guaranteed payment at the end of the policy (i.e. when you die). It costs more to get that extension of coverage.

Sometimes, life insurance will make more sense for you. But in many cases, life assurance has plenty of benefits - like a big payment to cover your estate costs, taxes, or pesky mortgage debt you were never able to pay off. It can be an excellent way to build passive wealth for your heirs or maybe a large charitable contribution when you pass, among other reasons.

Insurance or assurance are essential factors in protecting wealth. Our financial planners are ready to explore whether you and your family have the proper coverage. Schedule an Intro Call (https://calendly.com/freeman-intro-call/30min?month=2021-05) to find out how we help our clients.

Why You Need Life Insurance

Why do you need some sort of life insurance? Life expectancy just fell the most since WWII, and was worse for minorities.

Source: npr.org

Actionable Items for You:

- Black Americans lost about three years on average to life expectancy last year - that’s why it’s so important to have a plan in place. It should motivate you to get the ball rolling and do it now.

The reason we wanted to talk about insurance this month is painfully clear. According to the Centers for Disease Control and Prevention, life expectancy in the US declined by 1.5 years in 2020, primarily attributed to the… you know.

But for Black Americans, it was worse. Almost three years was taken off our life expectancy, dropping from 74.7 years in 2019 to 71.8 years in 2020. Do the math - you probably have fewer years left than you think, statistically.

I don’t know about you, but when I see that number, it motivates me. It motivates me to keep ensuring my family is taken care of, ensuring I have the infrastructure in place for them in the event that I pass away before I am ready. And insurance coverage is just a part of the bigger plan, but it’s an excellent place to start.

What is Insurance?

Source: IEEE Spectrum

Actionable Items for You:

Insurance coverage is a funny thing. Everyone seems to have some sort of idea what it is, most think they need it but not urgently, everyone has it for their car, and some have way too much. But what is insurance coverage, really?

It’s kinda right there in the name. Insurance can cover things like health, property & casualty insurance, life insurance, and insurance against disability. It all boils down to one thing - risk. When you have a family or loved ones that depend on your income, you need to make sure there’s a plan in place if you were to have an accident or no longer be able to work.

That’s the main point here - there is a high priority for you to get some basic coverage to secure you and your family from financial hardship if and when something terrible happens. It might not seem like an urgent need, but everyone thinks the same until an accident happens. It’s a big part of financial planning - emphasis on planning.

HSA Benefits

The top benefits of a Health Savings Account (HSA) and why you need to know.

Source: Healthequity.com

Actionable Items for You:

Do you want not single, not double, but TRIPLE tax advantages in your savings account? If you said yes, keep reading. If no… maybe we weren’t clear enough. Today we’re talking about Health Savings Accounts or HSAs. They're one of the most tax-advantaged accounts that the IRS will allow you to save in, as they have massive benefits, provided the account holder follows all the rules properly. While some accounts tax you when you put funds into an account, after you pay income tax or withdraw funds, HSAs are just built differently. Here are the top 3 benefits.

1. Contributions are Tax-Free.

Some accounts (like a Roth 401k or Roth IRA) are taxed before you put funds in, but then the money is not taxed when spent from the account. With an HSA, though, funds are not taxed before saving - kind of like a traditional 401k or IRA.

2. Growth is Tax-Free.

When the funds are inside an HSA, growth is tax-free - this has massive compounding effects long-term. You can also invest in growth assets like stocks or ETFs, and they can compound your future without paying Uncle Sam.

3. Distributions are Tax-Free.

So the catch with the traditional 401k or the IRA is that, while contributions are tax-free, withdrawals are taxable. The third tax advantage of HSAs is huge, in that funds spent from an HSA are not taxed - as long as they are spent on qualified medical expenses. You can still use the funds for other things if you need to, but hold off using an HSA for a new car. Use this account for those doctor visits or prescription eyeglasses instead.

That there is the holy trifecta of investment savings, and if you’re not taking advantage of it, you’re missing out. You have to know the game to play it, and that’s where we can help you. Want some help finding the right HSA for you? Schedule an Intro Call (https://calendly.com/freeman-intro-call/30min?month=2021-05), a no-obligation consultation with one of our team members.

Shopping for Insurance

Source: Hawley & Associates

Actionable Items for You:

It’s probably been a while since you shopped for your home or auto insurance. You might want to get some quotes to lower your spend.

There are a few ways to make this ‘shopping’ experience go quite smoothly and efficiently - we talk about them below.

When was the last time you shopped for your auto or homeowners insurance? We recommend shopping for new property & casualty insurance about every year or two, which many will put off or simply keep using the same insurer. Not doing so can lose you big bucks, as you may be able to snag some discounts without much work. When looking around:

Get quotes from at least three insurers.

Ask about discounts and savings, but pay attention to the overall price. A company that offers few discounts still may have lower premiums.

Choose a company with a good service rating. You want to rely on them when you need them.

Ask your friends and family about their carriers and service experiences.

Drive safely.

In most circumstances, your driving record (violations, accidents, claims) causes your auto insurance premiums to increase. However, you may not have had any incidents and find that when you get a notice from your insurance company about the renewal, your policy’s premium has increased. Yes, there’s inflation on insurance, and there may be even more impact this year versus years past.

Save on Premium Costs

Here are few possible ways to reduce your premium costs:

In less than 30 minutes, you can get multiple quotes either online or by picking up the phone. Being prepared with the following will help make this task even easier:

Life Insurance vs Life Assurance

Do you know the difference between Life Insurance and Life Assurance coverage?

Source: Free Price Compare

Actionable Items for You

Life insurance.

You’ve probably heard of it. You pay a premium for a set period, and if you pass away during that period, there’s a significant payout for your loved ones. It’s pretty simple overall and akin to things like your car insurance or your home insurance - it is to ensure financial commitments you have, like providing for family or paying off mortgages or other debts, will be covered. Most families have this type of coverage when they have young children or dependents. You can set a date in the future (like when your youngest turns 18 or another predetermined age) for when you can stop paying for the insurance. If you live past that date, you will not get a pay-out at the end of the term or refund your premiums. But that’s the point - it’s insurance against an adverse event. None of us plan on dying before our children, but we have to be prepared for it. Life insurance is a great way to achieve security for your family. Of course, if you want to take life insurance to the next financial planning step, you might want to consider Life Assurance.

Life Assurance

Life Assurance is similar but different. Some refer to this type of coverage as a ‘whole life’ policy because, as you can probably guess, it covers you for your whole… life. Essentially, it does the same as life insurance but you have a guaranteed payment at the end of the policy (i.e. when you die). It costs more to get that extension of coverage. Sometimes, life insurance will make more sense for you. But in many cases, life assurance has plenty of benefits - like a big payment to cover your estate costs, taxes, or pesky mortgage debt you were never able to pay off. It can be an excellent way to build passive wealth for your heirs or maybe a large charitable contribution when you pass, among other reasons. Insurance or assurance are essential factors in protecting wealth. Our financial planners are ready to explore whether you and your family have the proper coverage. Schedule an Intro Call (https://calendly.com/freeman-intro-call/30min?month=2021-05) to find out how we help our clients.

Why You Need Life Insurance

Why do you need some sort of life insurance? Life expectancy just fell the most since WWII, and was worse for minorities.

Source: npr.org

Actionable Items for You:

The reason we wanted to talk about insurance this month is painfully clear. According to the Centers for Disease Control and Prevention, life expectancy in the US declined by 1.5 years in 2020, primarily attributed to the… you know.

But for Black Americans, it was worse. Almost three years was taken off our life expectancy, dropping from 74.7 years in 2019 to 71.8 years in 2020. Do the math - you probably have fewer years left than you think, statistically.

I don’t know about you, but when I see that number, it motivates me. It motivates me to keep ensuring my family is taken care of, ensuring I have the infrastructure in place for them in the event that I pass away before I am ready. And insurance coverage is just a part of the bigger plan, but it’s an excellent place to start.