Alexandria Real Estate (ARE): Undervalued REIT. The overall Real Estate Investment Trust (REIT) sector has been down a lot year to date. For example, the office REIT category has been down 21.9% since the start of 2022. In addition, the REIT Industrial category is down 18% year to date. This decline provides long-term investors with some opportunities in the Real Estate sector.

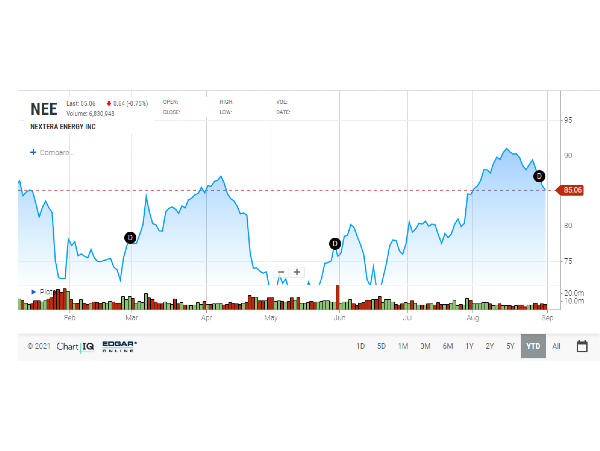

For example, Alexandria Real Estate Equities, Inc. (ARE) is one company I have had my eye on, and it looks like an excellent area to pick up some shares as it is near a support level at around $140 per share. The chart below shows that the $130 – $140 level was once a support level at four different times. In addition, the stock is trading at $145 per share. Thus, the REIT looks like it is in an excellent range to pick up shares. Next, we will determine if Alexandria Real Estate is an undervalued REIT and deserving of our hard earned money.

Source: TradingView

Alexandria Real Estate (ARE): Undervalued REIT

Affiliate

If you are interested in investing in stocks that pay dividends I recommend signing up for the Sure Dividend Newsletter* . It is a good value and one of the best dividend stock newsletters available. There is a 7-day free trial and grace period so it is risk free. The service provides top 10 stock picks each month with discussion of advantages, valuation, and risks. I highly recommend them and use their insights for my own stock research.

Overview of Alexandria Real Estate Equities

Alexandria Real Estate Equities (ARE) is an S&P 500 Index urban office REIT. The company is the first, longest-tenured, and pioneering owner, operator, and developer uniquely focused on collaborative life science, agricultural tech, and technology campuses in innovation cluster locations. The REIT has a total market capitalization of about $24.3 billion and an asset base in North America of 74.1 million square feet as of June 30, 2022.

Alexandria Real Estate was founded in 1994. The REIT pioneered this niche and has since established a significant market presence in major clusters, including Boston, the San Francisco Bay Area, New York City, San Diego, Seattle, Maryland Life Science Corridor, and the Research Triangle. Alexandria Real Estate has a longstanding and proven track record of developing Class A properties clustered in urban life science, agricultural tech, and technology campuses that provide its tenants with highly dynamic and collaborative environments that enhances their ability to successfully recruit and retain world-class talent and inspire productivity, efficiency, creativity, and success.

Alexandria Real Estate is down ~36% since its all-time high in January 2022. The primary driver of the stock price decrease has nothing to do with the company itself, as earnings are expected to grow about 12% in 2022 and are expected to grow roughly 8% in 2023. Instead, it has to do with the increase in interest rates, as this affected all REIT stocks in the markets.

The current stock price of $145 (as of this writing) is right at the lower end of the 52-week range, between $130 and $224.95 per share. Thus, Alexandria Real Estate looks like a stock that seems to be in the right place to buy up shares where both the 52-week range and support line meet.

ARE Dividend History, Growth, and Yield

We will look at Alexandria Real Estate’s dividend history, growth, and yield. We will then determine if it’s still a good buy at current prices.

Alexandria Real Estate is considered a Dividend Contender, a company that has increased its dividend for more than ten years. In this case, Alexandria Real Estate has increased its dividend for 12 consecutive years and the most recent dividend increase was 3%, announced in May 2022.

Dividend Growth

Additionally, according to Portfolio Insight* , ARE has a five-year dividend growth rate of about 6.76%, which is excellent considering how fast inflation increased last year and this year. The 10-year dividend growth rate is higher at ~9.19%. The dividend growth rate has been slowing down in recent years.

Something essential to note is that Alexandria Real Estate continued to pay its dividend during the most challenging period in the last 100 years. Many businesses and industries cut or suspended their dividend payments during the COVID-19 pandemic. However, Alexandria Real Estate continued to pay out its dividend and increased them. That is very noteworthy. This fact alone leads me to believe in the strength of the company and the fact that management is focused and committed to the dividend policy.

Dividend Yield

The company has an excellent dividend yield of approximately 3.34%, which is more than double the average dividend yield of the S&P 500 Index. This dividend yield is a respectable initial yield for dividend growth-driven investors. Although, it may not be an excellent stock for income-driven investors who may want a 4.5% yield or higher. However, with the company’s increasing dividend rate, I can see over a 5% yield on cost (YOC) in the next 5 to 7 years.

Alexandria Real Estate’s current dividend yield is higher than its own 5-year average dividend yield of 2.68%. I like to look at this metric because it gives me a good idea if a company I am researching is undervalued or overvalued based on the current and 5-year average yield. Stock price and dividend yield are inversely related. If the stock price increases, the dividend yield decreases, and vice versa.

Dividend Safety

Let’s determine if the current dividend is safe. This metric is critical to look at as a dividend growth investor. Undervalued dividend stocks sometimes present a “value trap,” and the stock price can continue to decline.

We must look at two critical metrics to determine if the dividend payments are safe yearly. The first one is Funds From Operation per share (FFO), and then we must look into Free Cash Flow (FCF) per share or Operating Cash Flow (OCF).

Analysts predict that Alexandria Real Estate will earn an FFO of about $8.41 per share for the fiscal year (FY) 2022. Analysts are 85% accurate when forecasting Alexandria Real Estate’s future FFO. Also, the company beats these estimates 15% of the time. In addition, the company is expected to pay out $4.72 per share in dividends for the entire year. These numbers give a payout ratio of approximately 56% based on FFO, a conservative value, leaving the company with much room to continue to grow its dividend. Most REITs tend to have a payout ratio of over 80%.

I am excited by having an 80% or lower dividend coverage with a dividend yield of 3.34% for future growth. At this point, it will allow the company to continue to grow its dividend at a mid-single-digit rate without sacrificing dividend safety. In addition, Alexandria Real Estate has a dividend payout ratio of 69% on an FCF basis. Thus, the dividend is well covered in both FFO and FCF.

Revenue and Earnings Growth / Balance Sheet Strength

We will now look at how well the REIT performed and grew its FFO and revenue throughout the years. When valuing a company, these two metrics are at the top of my list to study. Without revenue growth, a company can’t have sustainable FFO growth and continue paying a growing dividend.

Alexandria Real Estate revenues have been growing modestly at a compound annual growth rate (CAGR) of about 15.2% for the past ten years. Net income, however, did much better with a CAGR of ~21.1% over the same ten-year period. However, FFO has grown 4.5% annually over the past ten years and has a CAGR of 8.1% over the past five years.

Source: Portfolio Insight*

Since revenue, net income, and FFO did have good growth over the years, we will determine if this stock is attractive based on its valuation and dividend yield. We will talk about the company’s valuation later in this article. In the meantime, analysts predict that the company will grow FFO at a 5% rate over the next five years.

Last year’s FFO increased from $7.53 per share in FY2020 to $7.50 per share for FY2021, a decrease of 0.4% considering the challenging two years because of the COVID-19 pandemic. Additionally, analysts expect Alexandria Real Estate to make an FFO of $8.41 per share for the fiscal year 2022, which would be a ~12% increase compared to FY2021. This growth is something I like to see that future earnings continue to grow.

The company has a solid balance sheet. Alexandria Real Estate has an S&P Global credit rating of BBB+ and a Moody’s rating of Baa1, lower medium-grade investment rating. Also, the company has a debt-to-equity ratio of 0.6, which is a good ratio. Thus, the company has a stable balance sheet to overcome significant economic downturns like the COVID-19 pandemic last two years, adding to the dividend safety.

Risks

However, there are still risks with an investment in Alexandria Real Estate. For example, if there is a recession, this can continue to bring the stock price lower as it did in the Great Recession and during the COVID-19 pandemic, which saw prices decrease 76.9% and 97.4%, respectively. Also, since this is an office-type REIT, the company is at risk of more tenants having its employees work from home.

Competitive Advantage

Management execution of new properties in the portfolio, either through acquisition or construction of new properties, is its most significant competitive advantage in the future. Thus, the efficiency to scale is its most crucial growth driver.

Alexandria Real Estate an Undervalued REIT

One of the valuation metrics that I like to look for is the dividend yield compared to the past few years histories. I also want to look for a lower price-to-FFO (P/FFO) ratio based on the past 5-year or 10-year average. Lastly, I like to use the Dividend Discount Model (DDM). I use a DDM analysis because a business ultimately equals the sum of the future cash flow that that business can provide.

Let’s first look at the P/FFO ratio. Alexandria Real Estate has a P/FFO ratio of ~17.8X based on FY 2022 FFO of $8.41 per share. The P/FFO multiple is excellent compared to the past 5-year P/FFO average of 23.0X. If the REIT were to vert back to a P/FFO of 23.0X, we would obtain a price of $193.43 per share.

Now let’s look at the dividend yield. As I mentioned, the dividend yield currently is ~3.34%. There is good upside potential as Alexandria Real Estate’s own 5-year dividend yield average is ~2.68%. For example, if the REIT were to return to its dividend yield 5-year average, the price target would be $181.53.

The last item I like to look at to determine a fair price is the DDM analysis. I factored in a 9% discount rate and a long-term dividend growth rate of 6%. I use a 9% discount rate because of the higher-than-normal current dividend yield. In addition, the projected dividend growth rate is conservative and lower than its past 5-year average. These assumptions give a fair price target of approximately $166.77 per share.

If we average the three fair price targets of $193.43, $181.53, and $166.77, we obtain a reasonable, fair price of $180.58 per share, giving the firm a possible upside of 24.5% from the current price of $145 share price. Clearly, Alexandria Real Estate is an undervalued REIT.

Conclusion on Alexandria Real Estate (ARE): Undervalued REIT

Alexandria Real Estate is a high-quality company that should meet most investors’ requirements. The company has a market-beating 3.34% yield and a long-term dividend growth history. Past earnings growth has been excellent. However, past performance does not mean it will be the same in the future. However, I think at the current price the stock looks to be attractive.

Disclosure: I do not own shares of ARE

Thanks for reading Alexandria Real Estate (ARE): Undervalued REIT.

You can also read Kilroy Realty (KRC): Undervalued REIT and 4.2% Yield by the same author.

Author Bio: My name is Felix Martinez, and I am a Dividend Growth Investor who has invested in dividend growth stocks for the past seven years. I also run a YouTube channel called FiscalVoyage. I have written for SeekingAlpha.com as well as SureDividend.com. I focus on undervalued dividend growth stocks with capital return and dividend income potential. Make sure to follow me on my YouTube Channel. See you there.

Alexandria Real Estate (ARE): Undervalued REIT. The overall Real Estate Investment Trust (REIT) sector has been down a lot year to date. For example, the office REIT category has been down 21.9% since the start of 2022. In addition, the REIT Industrial category is down 18% year to date. This decline provides long-term investors with some opportunities in the Real Estate sector.

For example, Alexandria Real Estate Equities, Inc. (ARE) is one company I have had my eye on, and it looks like an excellent area to pick up some shares as it is near a support level at around $140 per share. The chart below shows that the $130 – $140 level was once a support level at four different times. In addition, the stock is trading at $145 per share. Thus, the REIT looks like it is in an excellent range to pick up shares. Next, we will determine if Alexandria Real Estate is an undervalued REIT and deserving of our hard earned money.

Source: TradingView

Alexandria Real Estate (ARE): Undervalued REIT

Affiliate

If you are interested in investing in stocks that pay dividends I recommend signing up for the Sure Dividend Newsletter* . It is a good value and one of the best dividend stock newsletters available. There is a 7-day free trial and grace period so it is risk free. The service provides top 10 stock picks each month with discussion of advantages, valuation, and risks. I highly recommend them and use their insights for my own stock research.

Overview of Alexandria Real Estate Equities

Alexandria Real Estate Equities (ARE) is an S&P 500 Index urban office REIT. The company is the first, longest-tenured, and pioneering owner, operator, and developer uniquely focused on collaborative life science, agricultural tech, and technology campuses in innovation cluster locations. The REIT has a total market capitalization of about $24.3 billion and an asset base in North America of 74.1 million square feet as of June 30, 2022.

Alexandria Real Estate was founded in 1994. The REIT pioneered this niche and has since established a significant market presence in major clusters, including Boston, the San Francisco Bay Area, New York City, San Diego, Seattle, Maryland Life Science Corridor, and the Research Triangle. Alexandria Real Estate has a longstanding and proven track record of developing Class A properties clustered in urban life science, agricultural tech, and technology campuses that provide its tenants with highly dynamic and collaborative environments that enhances their ability to successfully recruit and retain world-class talent and inspire productivity, efficiency, creativity, and success.

Alexandria Real Estate is down ~36% since its all-time high in January 2022. The primary driver of the stock price decrease has nothing to do with the company itself, as earnings are expected to grow about 12% in 2022 and are expected to grow roughly 8% in 2023. Instead, it has to do with the increase in interest rates, as this affected all REIT stocks in the markets.

The current stock price of $145 (as of this writing) is right at the lower end of the 52-week range, between $130 and $224.95 per share. Thus, Alexandria Real Estate looks like a stock that seems to be in the right place to buy up shares where both the 52-week range and support line meet.

ARE Dividend History, Growth, and Yield

We will look at Alexandria Real Estate’s dividend history, growth, and yield. We will then determine if it’s still a good buy at current prices.

Alexandria Real Estate is considered a Dividend Contender, a company that has increased its dividend for more than ten years. In this case, Alexandria Real Estate has increased its dividend for 12 consecutive years and the most recent dividend increase was 3%, announced in May 2022.

Dividend Growth

Additionally, according to Portfolio Insight* , ARE has a five-year dividend growth rate of about 6.76%, which is excellent considering how fast inflation increased last year and this year. The 10-year dividend growth rate is higher at ~9.19%. The dividend growth rate has been slowing down in recent years.

Source: Portfolio Insight*

Something essential to note is that Alexandria Real Estate continued to pay its dividend during the most challenging period in the last 100 years. Many businesses and industries cut or suspended their dividend payments during the COVID-19 pandemic. However, Alexandria Real Estate continued to pay out its dividend and increased them. That is very noteworthy. This fact alone leads me to believe in the strength of the company and the fact that management is focused and committed to the dividend policy.

Dividend Yield

The company has an excellent dividend yield of approximately 3.34%, which is more than double the average dividend yield of the S&P 500 Index. This dividend yield is a respectable initial yield for dividend growth-driven investors. Although, it may not be an excellent stock for income-driven investors who may want a 4.5% yield or higher. However, with the company’s increasing dividend rate, I can see over a 5% yield on cost (YOC) in the next 5 to 7 years.

Source: Portfolio Insight*

Alexandria Real Estate’s current dividend yield is higher than its own 5-year average dividend yield of 2.68%. I like to look at this metric because it gives me a good idea if a company I am researching is undervalued or overvalued based on the current and 5-year average yield. Stock price and dividend yield are inversely related. If the stock price increases, the dividend yield decreases, and vice versa.

Dividend Safety

Let’s determine if the current dividend is safe. This metric is critical to look at as a dividend growth investor. Undervalued dividend stocks sometimes present a “value trap,” and the stock price can continue to decline.

We must look at two critical metrics to determine if the dividend payments are safe yearly. The first one is Funds From Operation per share (FFO), and then we must look into Free Cash Flow (FCF) per share or Operating Cash Flow (OCF).

Analysts predict that Alexandria Real Estate will earn an FFO of about $8.41 per share for the fiscal year (FY) 2022. Analysts are 85% accurate when forecasting Alexandria Real Estate’s future FFO. Also, the company beats these estimates 15% of the time. In addition, the company is expected to pay out $4.72 per share in dividends for the entire year. These numbers give a payout ratio of approximately 56% based on FFO, a conservative value, leaving the company with much room to continue to grow its dividend. Most REITs tend to have a payout ratio of over 80%.

I am excited by having an 80% or lower dividend coverage with a dividend yield of 3.34% for future growth. At this point, it will allow the company to continue to grow its dividend at a mid-single-digit rate without sacrificing dividend safety. In addition, Alexandria Real Estate has a dividend payout ratio of 69% on an FCF basis. Thus, the dividend is well covered in both FFO and FCF.

Revenue and Earnings Growth / Balance Sheet Strength

We will now look at how well the REIT performed and grew its FFO and revenue throughout the years. When valuing a company, these two metrics are at the top of my list to study. Without revenue growth, a company can’t have sustainable FFO growth and continue paying a growing dividend.

Alexandria Real Estate revenues have been growing modestly at a compound annual growth rate (CAGR) of about 15.2% for the past ten years. Net income, however, did much better with a CAGR of ~21.1% over the same ten-year period. However, FFO has grown 4.5% annually over the past ten years and has a CAGR of 8.1% over the past five years.

Source: Portfolio Insight*

Since revenue, net income, and FFO did have good growth over the years, we will determine if this stock is attractive based on its valuation and dividend yield. We will talk about the company’s valuation later in this article. In the meantime, analysts predict that the company will grow FFO at a 5% rate over the next five years.

Last year’s FFO increased from $7.53 per share in FY2020 to $7.50 per share for FY2021, a decrease of 0.4% considering the challenging two years because of the COVID-19 pandemic. Additionally, analysts expect Alexandria Real Estate to make an FFO of $8.41 per share for the fiscal year 2022, which would be a ~12% increase compared to FY2021. This growth is something I like to see that future earnings continue to grow.

The company has a solid balance sheet. Alexandria Real Estate has an S&P Global credit rating of BBB+ and a Moody’s rating of Baa1, lower medium-grade investment rating. Also, the company has a debt-to-equity ratio of 0.6, which is a good ratio. Thus, the company has a stable balance sheet to overcome significant economic downturns like the COVID-19 pandemic last two years, adding to the dividend safety.

Risks

However, there are still risks with an investment in Alexandria Real Estate. For example, if there is a recession, this can continue to bring the stock price lower as it did in the Great Recession and during the COVID-19 pandemic, which saw prices decrease 76.9% and 97.4%, respectively. Also, since this is an office-type REIT, the company is at risk of more tenants having its employees work from home.

Competitive Advantage

Management execution of new properties in the portfolio, either through acquisition or construction of new properties, is its most significant competitive advantage in the future. Thus, the efficiency to scale is its most crucial growth driver.

Alexandria Real Estate an Undervalued REIT

One of the valuation metrics that I like to look for is the dividend yield compared to the past few years histories. I also want to look for a lower price-to-FFO (P/FFO) ratio based on the past 5-year or 10-year average. Lastly, I like to use the Dividend Discount Model (DDM). I use a DDM analysis because a business ultimately equals the sum of the future cash flow that that business can provide.

Let’s first look at the P/FFO ratio. Alexandria Real Estate has a P/FFO ratio of ~17.8X based on FY 2022 FFO of $8.41 per share. The P/FFO multiple is excellent compared to the past 5-year P/FFO average of 23.0X. If the REIT were to vert back to a P/FFO of 23.0X, we would obtain a price of $193.43 per share.

Now let’s look at the dividend yield. As I mentioned, the dividend yield currently is ~3.34%. There is good upside potential as Alexandria Real Estate’s own 5-year dividend yield average is ~2.68%. For example, if the REIT were to return to its dividend yield 5-year average, the price target would be $181.53.

The last item I like to look at to determine a fair price is the DDM analysis. I factored in a 9% discount rate and a long-term dividend growth rate of 6%. I use a 9% discount rate because of the higher-than-normal current dividend yield. In addition, the projected dividend growth rate is conservative and lower than its past 5-year average. These assumptions give a fair price target of approximately $166.77 per share.

If we average the three fair price targets of $193.43, $181.53, and $166.77, we obtain a reasonable, fair price of $180.58 per share, giving the firm a possible upside of 24.5% from the current price of $145 share price. Clearly, Alexandria Real Estate is an undervalued REIT.

Conclusion on Alexandria Real Estate (ARE): Undervalued REIT

Alexandria Real Estate is a high-quality company that should meet most investors’ requirements. The company has a market-beating 3.34% yield and a long-term dividend growth history. Past earnings growth has been excellent. However, past performance does not mean it will be the same in the future. However, I think at the current price the stock looks to be attractive.

Disclosure: I do not own shares of ARE

Thanks for reading Alexandria Real Estate (ARE): Undervalued REIT.

You can also read Kilroy Realty (KRC): Undervalued REIT and 4.2% Yield by the same author.

Author Bio: My name is Felix Martinez, and I am a Dividend Growth Investor who has invested in dividend growth stocks for the past seven years. I also run a YouTube channel called FiscalVoyage. I have written for SeekingAlpha.com as well as SureDividend.com. I focus on undervalued dividend growth stocks with capital return and dividend income potential. Make sure to follow me on my YouTube Channel. See you there.

Originally Posted on dividendpower.org