If your debt is causing you a financial emergency, seek professional support immediately.

Savings

Actionable Items for You:

- Your Savings Rate (Savings per year / annual income) is more important than how your investments do initially. Make sure to pay yourself first, and you’re future retired self will thank you.

One of the best ways to invest in yourself is to "Pay Yourself First!” We have talked about this before and want to reemphasize it again - because it's that important.

The percentage of your total income that you pay yourself is also known as your “Savings Rate.” The higher your savings rate, the more money you are saving per month. The more money you are saving each month, the more you can accumulate towards retirement, a down payment, your emergency fund, or any other financial goals you might have.

Your Savings Rate is more important than the Rate of Return on your investments. This is especially true early on, when your investment balances are low and you are building your portfolio.

The following example will help understand why:

- Let's say someone is just starting out and has $5,000 saved in an investment account.

- They make $50,000/year and have a savings rate of 10% or the equivalent of $5000/year.

- At this stage, a 5-10% difference of return that the $5000 investment account is getting is minor ($250-$500) compared to the difference of increasing their savings rate, let's say by only 5%. That’s an additional $2500 to be tucked away every year.

As we discussed a few weeks ago the power of compound interest can have a profound impact on your investments - save early, save often, and save long-term. While you are in the beginning stages of accumulating savings and investments, we like to focus more on the savings rate than the rate of return, and allow time and compound interest to do their thing on the back end.

Debt Management - Debt as a tool to build wealth

Actionable Items for You:

- There’s such a thing as good debt, like a mortgage for buying your home. But should debt be used for investing too? The answer is… it depends.

- Margin investing is using your investments as collateral to buy more investments, and is akin to taking a loan out to buy securities. If it’s done right, it can be really powerful for your long-term retirement goals. If done wrong, it can lead to disaster.

What is Good Debt?

Everyone thinks debt is a bad word. But when debt is used to purchase an asset that has the potential for increased return, or that can generate income, this can be viewed as good debt. Good debt is one of the best ways to start leveraging the power of your money and to purchase assets that increase in value or create passive income streams that help you develop real wealth.

Ever heard of a mortgage? Your home is one example where we may first experience the power of leverage.

For most, it’s not possible to buy a house outright. Using debt as a tool allows you to get into your home with a reasonable monthly payment. From here you can build equity in the property, receive potential tax advantages, and if you know you’ll be able to make your monthly payment, there is the additional benefit of improving your credit score.

Depending on your circumstances and risk tolerance, using leverage to build your investment portfolio, or using leverage to build a portfolio of income-producing real estate, can be another good debt strategy.

What is Margin?

From Investopedia:

Margin refers to the amount of equity an investor has in their brokerage account. "To margin" or "buying on margin" means to use money borrowed from a broker to purchase securities. You must have a margin account to do so, which is a brokerage account where the broker lends the investor money to buy more securities.

Using margin to purchase securities is effectively like using the current cash or securities already in your account as collateral for a loan. The collateralized loan comes with a periodic interest rate that must be paid. The investor is using borrowed money, or leverage, and therefore both the losses and gains will be magnified as a result. Here’s a great breakdown of how it works.

In a bull market, we can see how an investment account that uses margin can add significantly to a portfolio’s return. However, we know that markets go up and down and it’s always possible for your borrowed securities to decrease, and when that happens, you may receive a margin call. This is when the broker will request additional cash to be deposited to make up for the decreased collateral, or they will be forced to sell your investments for you.

In the past couple of weeks, we have seen how a decrease in an asset (Bitcoin) and the use or overuse of leverage can quickly propel the price down further.

The comfort level with a given amount of debt depends on your tolerance for risk.

If you borrow to diversify your portfolio, are you willing to ride out a volatile stretch in the market? Also, consider your time horizon - are you determined to pay off an investment-related debt in two years, or would you be okay if it took longer in the event of a market pullback?

Questions like these can help you assess whether you feel comfortable taking on debt as a part of your investment strategy.

Debt Management - Strategies to eliminate your debt

Source: Forbes

Actionable Items for You:

- Paying down debt can be overwhelming, especially if you feel it’s not under control.

- One of our three methods for payments below may help: The Debt Snowball method, the Debt Avalanche method, or the Debt Consolidation method.

“I want to pay down my debt, or I want to be debt-free.” Ever said that before?

As they say, the first step is admitting you have a problem, and we chat with our clients about this often. The recognition that eliminating personal debt will help one relieve stress, start a business, or be able to invest more to build wealth is an excellent starting point.

Actions to move forward from recognition to reduction take some work.

The next steps taken in this process are what we talked about over the past few weeks. Building awareness around cash flow can determine how much extra income should be put towards a debt elimination plan, and taking inventory of the debt that you have will help you plan on how to get there.

Understanding how much is coming in and going out every month is essential. Want to know how much discretionary income can be put towards your debt elimination goal?

Let’s say we have done our cash flow analysis and have determined that you have an extra $1000/month to put towards your goals. This could be split among several goals, like saving for retirement or a vacation, or you could decide that the goal of paying off debt is priority #1.

If we have taken inventory of our debts, as discussed in last week’s report, then we’ll know how much we owe on each account and the interest that is being charged on the debt. This will help us determine the right debt payment strategy for you.

Some strategies below will help you take an approach that focuses on putting your extra discretionary income towards one debt at a time and paying the minimum on the rest.

The Debt Snowball method:

This method focuses on the smallest debt balance first. So, you would put that extra $1000/month towards the smallest balance while only paying the minimum on your other debts. Once the smallest balance is paid off you move on to the next smallest balance. While this method may not be the most cost-effective, as you may pay more in interest, the psychology of getting smaller wins by paying off debt at a faster rate may produce more momentum and good feelings around the accomplishments you are making.

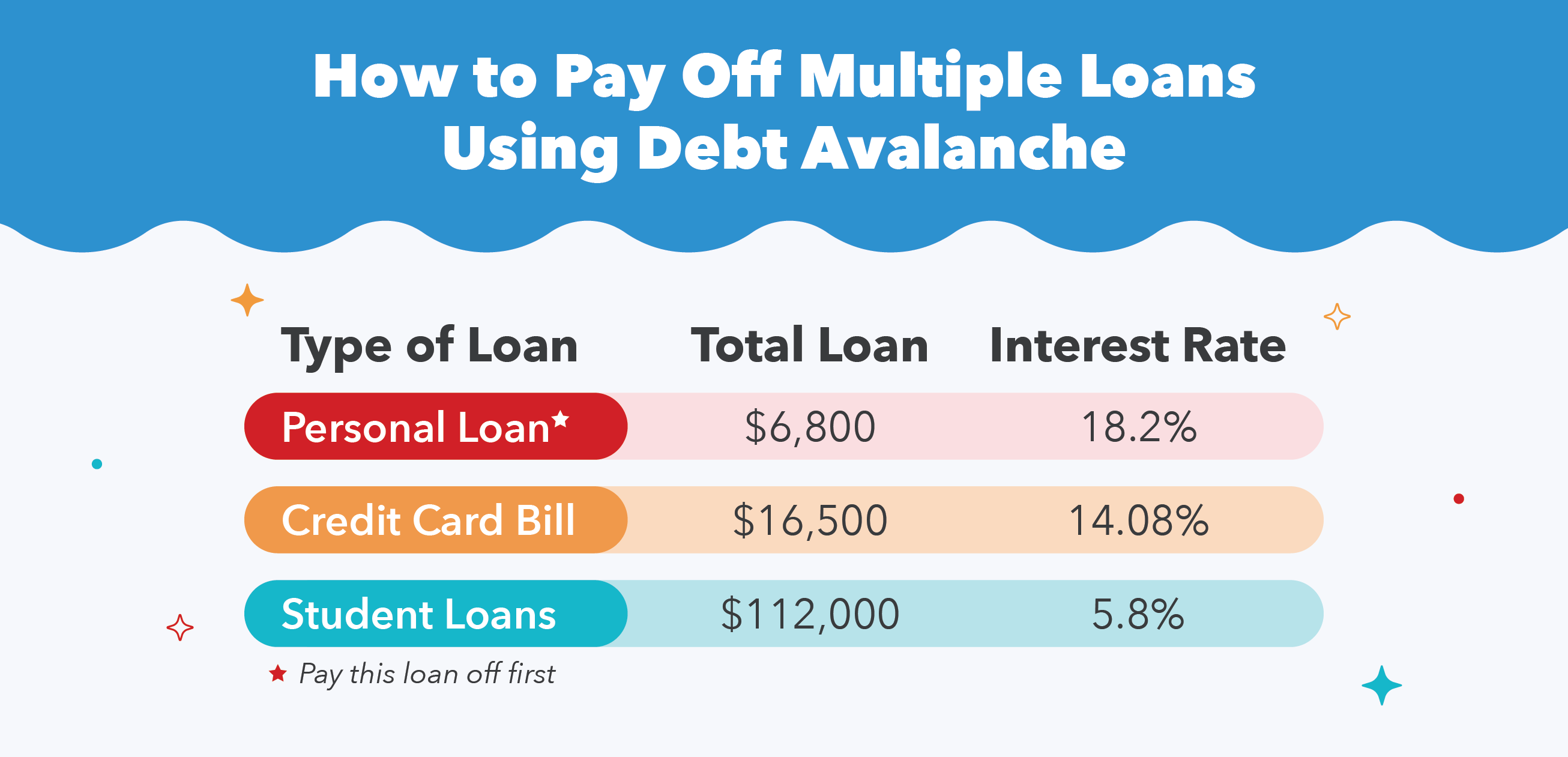

The Debt Avalanche method:

This method focuses on the debt with the highest interest rate first. Simply, putting the extra $1000/month towards the balance with the highest interest rate while only paying the minimum on other debts until it’s paid off is the most cost-effective way to do this. Once the first debt obligation is paid off you would then focus on the debt with the next debt with the highest interest rate, and so on.

Debt Consolidation method:

Another strategy that could be used is Debt Consolidation. The idea here is to bring multiple debt payments into one lump sum. The goal is to make it easier on you by only having one payment to remember and plan as well as having a lower interest rate and finding some savings by a reduced interest rate across the loans. This can be done via home re-finance, balance transfer cards, or a personal loan.

There isn’t a one solution fits all strategy. Schedule an Intro Call with one of our planners and we can explore what will work best for you.

Debt Management – Taking Inventory

Debt. It comes in all different shapes and sizes.

As an individual or family, we mostly deal with consumer debt. This is when we borrow money for a purchase, as a consumer, and are offered a loan or line of credit from a bank, credit union, a credit card company, or an institution (Dept. of Education). This debt comes with an agreement (terms) to pay back the borrowed money over time.

These consumer purchases we make could be for a car, a house, education, a shopping spree, or groceries.

Consumer debt can be put into two basic categories - secured debt and unsecured debt. Secured debt involves a loan that has collateral, for example, a car loan or a mortgage. Unsecured debt are things like credit cards, personal loans, and medical debt that is not backed by collateral or any other guarantor - just a promise to pay from the consumer.

It can seem overwhelming at times and many put planning off. However, if you have debt (like most of us do), are struggling with debt, or have the goal to reduce your debt, the starting point is to take inventory of everything that is owed.

You'll want to know the following information for every piece of debt you have:

- Company Name: Chase Credit Card

- Type: Revolving

- Interest rate: 16.74%

- Balance due: $1950

- Minimum payment: $50

- The payment amount you are making: $250

- Date due: 2nd of every month

This can seem dull, but you gotta do it to get a handle on debt before it spins out of control and snowballs. Debt accrues interest, which just means more debt if you don't start paying it off.

Inventory can be done by reviewing all of your account statements to capture all of the points above, and we would also recommend reviewing the information that can be found on your credit reports to make sure nothing has gone missing or been forgotten.

You can track down your credit reports and request them for free via this website. It only takes two minutes to answer some questions and get access:

https://www.annualcreditreport.com/

Federal law allows you to get Free Credit Reports every 12 months. Due to COVID-19, the three credit bureaus are allowing access to your free reports weekly.

In the coming weeks, we will discuss the next steps to come up with a plan to manage your debt. First, we want to build that awareness and take inventory of what we have.

Our planners are ready to continue this conversation and help you build a plan that suits your needs. Schedule an Intro Call to find out more about how we work with our clients to reduce their debt.

Actionable Items for You:

- Debt can be overwhelming, but taking the first step to get out of it starts with building an inventory of what you owe. Get the basic information and have it all in one place for easy access.

- It would be worth tracking down your credit reports at https://www.annualcreditreport.com/ to make sure you didn’t miss anything. Unchecked debt can be a major burden down the road.

If your debt is causing you a financial emergency, seek professional support immediately.

Savings

Source: Statista

Actionable Items for You:

One of the best ways to invest in yourself is to "Pay Yourself First!” We have talked about this before and want to reemphasize it again - because it's that important.

The percentage of your total income that you pay yourself is also known as your “Savings Rate.” The higher your savings rate, the more money you are saving per month. The more money you are saving each month, the more you can accumulate towards retirement, a down payment, your emergency fund, or any other financial goals you might have. Your Savings Rate is more important than the Rate of Return on your investments. This is especially true early on, when your investment balances are low and you are building your portfolio.

The following example will help understand why:

As we discussed a few weeks ago the power of compound interest can have a profound impact on your investments - save early, save often, and save long-term. While you are in the beginning stages of accumulating savings and investments, we like to focus more on the savings rate than the rate of return, and allow time and compound interest to do their thing on the back end.

Debt Management - Debt as a tool to build wealth

Source: Ramsey Solutions

Actionable Items for You:

What is Good Debt?

Everyone thinks debt is a bad word. But when debt is used to purchase an asset that has the potential for increased return, or that can generate income, this can be viewed as good debt. Good debt is one of the best ways to start leveraging the power of your money and to purchase assets that increase in value or create passive income streams that help you develop real wealth.

Ever heard of a mortgage? Your home is one example where we may first experience the power of leverage.

For most, it’s not possible to buy a house outright. Using debt as a tool allows you to get into your home with a reasonable monthly payment. From here you can build equity in the property, receive potential tax advantages, and if you know you’ll be able to make your monthly payment, there is the additional benefit of improving your credit score.

Depending on your circumstances and risk tolerance, using leverage to build your investment portfolio, or using leverage to build a portfolio of income-producing real estate, can be another good debt strategy.

What is Margin?

From Investopedia: Margin refers to the amount of equity an investor has in their brokerage account. "To margin" or "buying on margin" means to use money borrowed from a broker to purchase securities. You must have a margin account to do so, which is a brokerage account where the broker lends the investor money to buy more securities.

Using margin to purchase securities is effectively like using the current cash or securities already in your account as collateral for a loan. The collateralized loan comes with a periodic interest rate that must be paid. The investor is using borrowed money, or leverage, and therefore both the losses and gains will be magnified as a result. Here’s a great breakdown of how it works.

In a bull market, we can see how an investment account that uses margin can add significantly to a portfolio’s return. However, we know that markets go up and down and it’s always possible for your borrowed securities to decrease, and when that happens, you may receive a margin call. This is when the broker will request additional cash to be deposited to make up for the decreased collateral, or they will be forced to sell your investments for you.

In the past couple of weeks, we have seen how a decrease in an asset (Bitcoin) and the use or overuse of leverage can quickly propel the price down further.

The comfort level with a given amount of debt depends on your tolerance for risk. If you borrow to diversify your portfolio, are you willing to ride out a volatile stretch in the market? Also, consider your time horizon - are you determined to pay off an investment-related debt in two years, or would you be okay if it took longer in the event of a market pullback?

Questions like these can help you assess whether you feel comfortable taking on debt as a part of your investment strategy.

Debt Management - Strategies to eliminate your debt

Source: Forbes

Actionable Items for You:

“I want to pay down my debt, or I want to be debt-free.” Ever said that before? As they say, the first step is admitting you have a problem, and we chat with our clients about this often. The recognition that eliminating personal debt will help one relieve stress, start a business, or be able to invest more to build wealth is an excellent starting point.

Actions to move forward from recognition to reduction take some work. The next steps taken in this process are what we talked about over the past few weeks. Building awareness around cash flow can determine how much extra income should be put towards a debt elimination plan, and taking inventory of the debt that you have will help you plan on how to get there.

Understanding how much is coming in and going out every month is essential. Want to know how much discretionary income can be put towards your debt elimination goal? Let’s say we have done our cash flow analysis and have determined that you have an extra $1000/month to put towards your goals. This could be split among several goals, like saving for retirement or a vacation, or you could decide that the goal of paying off debt is priority #1. If we have taken inventory of our debts, as discussed in last week’s report, then we’ll know how much we owe on each account and the interest that is being charged on the debt. This will help us determine the right debt payment strategy for you.

Some strategies below will help you take an approach that focuses on putting your extra discretionary income towards one debt at a time and paying the minimum on the rest.

The Debt Snowball method:

Source: Ramsey Solutions

This method focuses on the smallest debt balance first. So, you would put that extra $1000/month towards the smallest balance while only paying the minimum on your other debts. Once the smallest balance is paid off you move on to the next smallest balance. While this method may not be the most cost-effective, as you may pay more in interest, the psychology of getting smaller wins by paying off debt at a faster rate may produce more momentum and good feelings around the accomplishments you are making.

The Debt Avalanche method:

Source: Mint

This method focuses on the debt with the highest interest rate first. Simply, putting the extra $1000/month towards the balance with the highest interest rate while only paying the minimum on other debts until it’s paid off is the most cost-effective way to do this. Once the first debt obligation is paid off you would then focus on the debt with the next debt with the highest interest rate, and so on.

Debt Consolidation method:

Source: Consolidatecreditcard.org

Another strategy that could be used is Debt Consolidation. The idea here is to bring multiple debt payments into one lump sum. The goal is to make it easier on you by only having one payment to remember and plan as well as having a lower interest rate and finding some savings by a reduced interest rate across the loans. This can be done via home re-finance, balance transfer cards, or a personal loan.

There isn’t a one solution fits all strategy. Schedule an Intro Call with one of our planners and we can explore what will work best for you.

Debt Management – Taking Inventory

Source: Time

Debt. It comes in all different shapes and sizes.

As an individual or family, we mostly deal with consumer debt. This is when we borrow money for a purchase, as a consumer, and are offered a loan or line of credit from a bank, credit union, a credit card company, or an institution (Dept. of Education). This debt comes with an agreement (terms) to pay back the borrowed money over time. These consumer purchases we make could be for a car, a house, education, a shopping spree, or groceries.

Consumer debt can be put into two basic categories - secured debt and unsecured debt. Secured debt involves a loan that has collateral, for example, a car loan or a mortgage. Unsecured debt are things like credit cards, personal loans, and medical debt that is not backed by collateral or any other guarantor - just a promise to pay from the consumer.

It can seem overwhelming at times and many put planning off. However, if you have debt (like most of us do), are struggling with debt, or have the goal to reduce your debt, the starting point is to take inventory of everything that is owed.

You'll want to know the following information for every piece of debt you have:

This can seem dull, but you gotta do it to get a handle on debt before it spins out of control and snowballs. Debt accrues interest, which just means more debt if you don't start paying it off. Inventory can be done by reviewing all of your account statements to capture all of the points above, and we would also recommend reviewing the information that can be found on your credit reports to make sure nothing has gone missing or been forgotten.

You can track down your credit reports and request them for free via this website. It only takes two minutes to answer some questions and get access: https://www.annualcreditreport.com/ Federal law allows you to get Free Credit Reports every 12 months. Due to COVID-19, the three credit bureaus are allowing access to your free reports weekly.

In the coming weeks, we will discuss the next steps to come up with a plan to manage your debt. First, we want to build that awareness and take inventory of what we have. Our planners are ready to continue this conversation and help you build a plan that suits your needs. Schedule an Intro Call to find out more about how we work with our clients to reduce their debt.

Actionable Items for You: