“If you want something you’ve never had, you must be willing to do something you’ve never done” -Thomas Jefferson

Remember the first time you rode that roller coaster? It looked like it would fling you off at any moment. You weren’t sure you had enough life insurance to provide for your family because you were definitely going to die that day – or so it seemed.

Take Control of Your Money with these Simple Steps!

Debt Free Living Is Possible

We all know how that day ended up. You were scared out of your mind before and during the ride, but after it was all over, you realized it wasn’t that bad. Some of you even wanted to go on it again! Such is life – finances are scary because most of us don’t know as much as we should about money. Putting our heads in the sand has cost us dearly in the past, and it’s clear the old way of doing things is not working.

The time to change your financial future is now. So get in, close the door, and put on your harness because it may get bumpy. If you stick with it, I promise you will make it out safe and sound in the end!

Hopefully, by now, you have taken the steps in the budget article and identified your income, monthly expenses, and debts. You should have a good idea of where you are financially – as grim as it may seem.

You may be in a place where it’s time to sell what you can to get out from under the crushing weight of your debt. Can you afford that car payment? How about the boat? Your level of financial insecurity will determine how drastic you need to get. Yard sales, Craigslist, Offer up, eBay, etc., are great ways to sell your stuff and bring in some much-needed income.

If you are struggling with how to get out of debt, follow these steps to get your life back on track. The way you currently live isn’t working, so let’s make some drastic changes to improve your life!

4 Steps To Make Your Own “Get Out Of Debt Plan”

When you break it down, the strategy to get out of debt is rather simple. The difficulty is creating the plan in the first place and actually sticking with it. To make it clear, I will break down the easiest and fastest way to create your own get out of debt plan.

1. Create A Budget

Before you do anything, you need to know how much money you have coming in each month and how much money you have going out. If you are unfamiliar with how to start a budget, check out my related article: How to create a budget – for beginners.

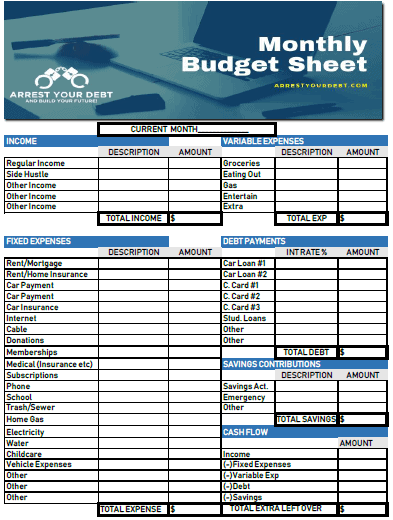

A budget will give you a clear picture of how bad your financial situation is or how quickly you can make it better. I created a free budget spreadsheet that you can download and use. Click the image below to download a free blank copy.

A budget is the foundation of any debt-free plan. Without a monthly budget, you have little to no chance of taking control of your money and eliminating your financial stress.

2. Be Honest About Your “Needs” And “Wants”

Take an honest look at your budget and see where there is wasteful spending. Waste can be described as “elective spending” such as entertainment. Look for things in your budget that you spend money on each month but don’t need these things to survive.

This includes nail or hair appointments, going to the movies, eating out at restaurants – you get the idea. Total up how much you generally spend on these things.

The first step is to identify how much money you could have if you didn’t spend anything on elective items. Now let me be clear, I understand that some wasteful spending is important to maintain your sanity. It just needs to be in moderation.

Ultimately wasteful spending and getting out of debt are linked together.

Less wasteful spending = more money to go towards debt = get out of debt faster

That is the simple formula to get out of debt. You are the one who gets to make the ultimate decision of how quickly you want to get out of debt. The more you cut, the faster it will happen.

Wasteful Spending Can Hide In Necessities

The problem with wasteful, discretionary, or elective spending is its ability to disguise itself as “necessary spending.” For instance, we all agree that to survive, we need clothing, food, shelter, and transportation. However, most of us – including myself – spend more on these necessities than we should.

As I get into this list, please understand I’m not telling you how to live your life. I am giving ideas for you to evaluate and decide if it is right for you. If you are sick and tired of being broke and stressing about money, you may decide to drastically change your life and spending to change your future drastically.

Save Money On Clothing

While we all need clothing, many of us wear clothes that would make kings of old envious. While a $200 pair of jeans may be more comfortable than a $30 pair, imagine how much extra money you could save if you buy generic. Or, heaving forbid, you bought slightly used clothing from a second-hand store!

Again, this depends on how quickly you want to get out of debt but double-check how much money you spend on clothing and see where you can make cuts if you wanted to.

Save Money On Groceries

I am the first to admit that spending money on food is where I struggle the most. When it comes to food, I usually spend more than I should because I am lazy. Rather than packing my lunch every day, I find myself going through a drive-through to grab a quick meal – at a much higher price.

In addition, when I get home from work and my wife and I are tired, it is so much easier to take the family to a restaurant than it is to make dinner at home.

However, when the end of the month comes, and I see how much money I spent on food, it has never been worth it. Whenever I overspend, I am always filled with regret.

I have found that to combat my midweek laziness, meal prepping is the best way to go. Check out my related article, How to meal prep for beginners, if you need some direction on how to meal prep each week to save you a TON of money each month.

Get in the habit of shopping for groceries. There are many ways you can save money on food each month through mobile apps and create a grocery list. I have another good article further detailing this: Save money on groceries with these simple tips.

Save Money On Your Mortgage Or Rent

Did you know that the average size of a new home build in the United States is now 2,600 square feet? That is more than double the size of the average home in 1960! In America, we definitely subscribe to the theory that bigger is better – but is it really? With increased home sizes comes increased spending on rent and mortgages.

Take a look at your current living situation and decide if downsizing is an option. We have much more space in our homes than we “need,” and most of us could cut way down on our square footage and our mortgage.

Relocating to a cheaper area may also be a good idea. In Arizona, you will pay more for a home simply because of the city you live in. The cheaper cities aren’t necessarily more dangerous, but some stigmas come with certain names.

This is only a viable tactic to reduce your debt load if you really are paying significantly more for where you are currently living than you need to be. If you are moving for purely financial reasons, you need to consider all of the different costs associated with your move.

Movers will likely be the largest expense, but even if you do this all on your own, it can still be a time-consuming and expensive process. Read up on moving checklists to make sure you fully understand what you are getting yourself into and what can go wrong.

How much are you paying for stigmas each month?

Save Money On Your Vehicle Expenses

You knew this section was coming. Everyone has a car payment, right? Wrong. I don’t, and I haven’t had a car payment in over 10 years. Now before you pat me on the back, let me tell you about my stupid vehicle decisions.

When my wife and I first married, we spent about $1,300 a month on vehicle payments. Looking back, I have no idea how we could afford those payments. However, 10 years ago, we decided to buy vehicles with cash and eliminate car payments. The amount of money we have saved over the past 10 years is astronomical.

My wife and I now drive vehicles that are over 10 years old and are closing in on 200,000 miles. And guess what, they still work! I had no idea vehicles could last so long if you maintained them and paid money once in a while to change the oil, rotate the tires, redo the brakes, etc.

Seriously, before we bought two cheap vehicles with cash, I thought that it was basically worthless after a vehicle hit 100,000 miles. I was convinced that after 100,000 miles, I would be stranded on the road over and over again. It turns out I was totally wrong. Our two vehicles are still running strong, and I’m super excited for the day my car crosses the 200,000-mile mark – just for bragging rights!

Reevaluate your vehicle situation. Could you save money with a cheaper insurance company or a cheaper vehicle? It’s worth looking into.

3. Decide How Much Should Be In Your Emergency Fund

The short answer is: $1,500 to $2,000. However, there is much more you need to know about emergency savings accounts.

Before you consider a “get out of debt loan” that many companies will try and sell you through consolidations or debt forgiveness programs, why don’t you be your own bank?

Before you yell at me because you are broke and that “free stuff” is even too expensive for you, hear me out. If you have done your job and created a budget, and decided to cut some unnecessary spending, extra money should be leftover. If there’s not, you either need to cut more out of your budget or pick up a side hustle.

Now that you have made enough cuts or increased your income let’s figure out what to do with that extra money.

Before you start paying any of your debt off, you need an emergency fund to protect yourself from life. For instance, if you have $300 extra each month and start putting it all towards debt, what do you do when your car breaks down? You’re going to put it on a credit card.

In other words, 1 step forward, two steps back.

To start taking 2 steps forward and only 1 step back, you need to protect yourself with an emergency fund. An emergency fund is a savings account with cash in it that you can quickly access when life throws expensive problems your way.

By dipping into this fund and replenishing it immediately, you will avoid all the interest charges that credit card companies tack on. An emergency savings is similar to your own insurance policy – for yourself.

To learn more about emergency funds and how to set one up, refer to my related article: Everything you need to know about emergency funds.

How To Identify An Emergency And When You Should Use Your Emergency Fund

Your emergency savings is only for that – emergencies. When you run out of fun money at the end of the month and want to go to a movie, that does not constitute an emergency.

An emergency savings should be your priority so you can deal with life when it happens because it will happen. Your washer and vehicle will both break simultaneously, and having these savings will keep you from going further into debt.

If you take money from it, your priority next month will be to replenish it. After your saving is adequate, between $1,500 and $2000, you can start attacking your debts.

Track Your Progress With An Emergency Fund Coloring Page And Other Debt Free Charts!

I am a very visual person, so I need physical things to keep me motivated. I created free coloring pages to keep me motivated when we first started our debt-free journey. If you are a visual person like me, click the image below to pick up your own emergency fund coloring page!

4. Choose The Best Way To Get Out Of Debt

After you have a fully-funded emergency savings, it’s now time to attack our debt! As discussed earlier, identify all of your debts individually.

We will now methodically destroy one debt at a time while paying the minimum amount on all of your other debts. Again, this is where personal finance becomes personal. Each of us is motivated by different strategies, so which debt you pay off first depends on your own personality.

There are two major methods to get out of debt. The first method is the debt snowball method originally credited to Dave Ramsey.

The other more mathematically sound method is the debt avalanche. The debt snowball pays off the lowest total debt first before you move on to the next.

The avalanche method pays off the debt with the highest interest rate first. For a more detailed comparison, refer to my related article: The debt snowball vs. the debt avalanche.

When it all comes down to it, it doesn’t really matter which method you choose as long as you pick a method and stick with it. In the end, if you quit halfway through, it didn’t matter which plan you chose. It’s more important to choose to stick with it than which plan you decide to follow.

Use Undebt.it To Help You Pick The Right Debt Payoff Plan

I recently came across the website Undebt.it and spoke with the owner and creator of the site, Jeff Donaldson. He has a great vision of helping people get out of debt and even designed a free website application to do just that. His get out of debt app is the perfect solution if you are unsure which debt plan you should follow.

I gave the Undebt.it app a test drive, and I was impressed with how much Jeff offered, for free! Full disclosure, he does have a paid version that costs $1 a month, but the free version does enough to get you on track. I wrote a full review of the Undebt.it app here.

That’s Great But How Do I Get Out Of Debt Fast?

In our current environment, everything is given to us immediately. Google is there for quick answers, and credit cards give us a way to buy things without waiting. Waiting has become a thing of the past – for those who are willing to spend money.

Unfortunately, many of us got into debt without even knowing it. One day we woke up and realized how big of a mess we were in. As much as I would like to give you a quick and simple way to get out of debt fast, I will not lie to you. There is no quick and painless way to get out of debt.

Those who promise you a quick and easy way are salesmen. They sell refinance and debt consolidation products as the “best ways to get out of debt.” In reality, these products make them rich and keep you broke.

If you’re considering debt consolidation, check out my article before you make your decision.

Getting out of debt once and for all will take longer than you will want. However, once you finally get out, you will feel a sense of accomplishment that is nothing short of awesome. Your look on money will have changed, and you will be able to finally start building wealth while watching your financial stress melt away.

But I’m Broke, How Can I Get Out Of Debt?

If you’re in debt, you’re right – you’re broke. However, just because you are broke, that doesn’t mean you’re broken.

You’re broke because of some financial mistakes that were either your fault or something that was thrust upon you. Either way, you’re in debt, and it’s time to get out.

Even if you’re broke and on a low income, it’s still possible to get out of debt. By following the 4 steps above, even broke people can start to make progress. You’re either broke because you spend too much money, don’t make enough money or both. Control your spending, or you will never make enough to get out of debt.

Once you control how much you spend by creating a budget, you can focus on making more money with a side hustle or increasing your income at work. The steps to get out of debt don’t change – regardless of how much you do or do not make. Control spending and increasing income will ultimately be the key.

I Have A Bunch Of Credit Card Debt, How Do I Get Out Of It?

I recently met with someone who had 10 different credit cards, and most of them were maxed out. They had a strategy of moving their balances around to 0% interest cards, but that strategy quickly caught up with them. After a certain amount of time, the 0% interest would skyrocket to over 20%, and they frantically would move money around to make their minimum payments.

Unfortunately, this strategy is quite common as people struggle to stay above water. The best way to get out of credit card debt is to stop using them. Once and for all.

You could also consider a credit repair company, like Credit Saint. They can help you fix your credit score and repair the damage of credit card debt.

Credit cards and payday loans are created to make the lenders money at the expense of the borrower. It’s a terrible downward spiral that people find themselves in with no clear way to get out.

To get out of credit card debt, refuse to put any more money on them. Pay the minimum balance on every card except for one. Pay off one card at a time as quickly as you can.

Follow the steps above to create a budget and figure out what plan you will use to get out of debt. Is it the debt avalanche or the debt snowball? There’s no wrong answer as long as you pick a plan and stick with it.

Debt Settlement May Be An Option

If you’re broke, debt settlement may not be an option for you. However, if you have any money in your savings account, some credit card companies or debt collectors are willing to settle the debts for pennies on the dollar. For more information on negotiating with debt collectors and debt settlements, check out my related article below.

How My Wife And I Will (hopefully) Stay Debt Free For Life

Below is a flow chart I created to show how your monthly debt attack should work in order from most important to least. This is how my wife and I overcame our debt and now live a debt-free life.

Obviously, yours may look different depending on how many debts you have, but you get the idea. As you start, attack one debt at a time. Make the minimum required payments on the others as you knock out the first debt. After the first is eliminated, it’s time to move on to the next.

So as you can see, we put our money into our checking account and take out our monthly anticipated bills. After that, we attack our emergency savings. If your emergency fund isn’t fully funded, make minimum payments on all your debts until it is funded. After it is funded, we start on the debt.

I am a visual person, and I need aids to stay motivated. Right now, my wife and I are paying off our house. To see the progress, I put a glass jar in our kitchen and filled it with marbles. Each marble represents $1,000 towards the total amount left on our house. Each month as we pay down the principle, I take out the corresponding amount of marbles to physically see the debt going down.

You can use similar visual aids for your debts to stay motivated.

Some people use thermometers that they color and put on their fridges. Either way, find what works for you. Ultimately, you want to get to a point where your flow chart is not focused on debts because you have paid them off! Below is a similar chart that my wife and I now use.

From the charts, you can see where I started to where I am now. Soon, I will delete the “pay off house fund” because that is where the majority of my extra money goes now. That will be a fantastic day! It will happen for me because of the safeguards I have put in place and the vision I have for my family. You can be here too, and it will not take as long as you think!

With a clear strategy in place, you will see how quickly you can accomplish your goals.

I’m Debt Free! Now What?

After you have paid off all your debts, you need to increase your emergency fund except for your home. I recommend you save up to 6 months of living expenses (in cash) if you lose your job or income.

Other experts range from 3-8 months of expenses, so I decided to fall on the 6th-month mark to feel comfortable. That means if your monthly necessary bills are $2,000 a month, you need to save up $12,000 in your emergency savings. This protects you from a job loss or other significant financial disaster for at least 6 months.

Again, if you have any questions or comments, please reach out to me. I am here for you, and I am living proof this can be accomplished. You can get to a point where an unexpected vehicle repair does not need to go on a credit card. You can do it, and I will be here for you!

“If you want something you’ve never had, you must be willing to do something you’ve never done” -Thomas Jefferson

Remember the first time you rode that roller coaster? It looked like it would fling you off at any moment. You weren’t sure you had enough life insurance to provide for your family because you were definitely going to die that day – or so it seemed.

Take Control of Your Money with these Simple Steps!

Debt Free Living Is Possible

We all know how that day ended up. You were scared out of your mind before and during the ride, but after it was all over, you realized it wasn’t that bad. Some of you even wanted to go on it again! Such is life – finances are scary because most of us don’t know as much as we should about money. Putting our heads in the sand has cost us dearly in the past, and it’s clear the old way of doing things is not working.

The time to change your financial future is now. So get in, close the door, and put on your harness because it may get bumpy. If you stick with it, I promise you will make it out safe and sound in the end!

Hopefully, by now, you have taken the steps in the budget article and identified your income, monthly expenses, and debts. You should have a good idea of where you are financially – as grim as it may seem.

You may be in a place where it’s time to sell what you can to get out from under the crushing weight of your debt. Can you afford that car payment? How about the boat? Your level of financial insecurity will determine how drastic you need to get. Yard sales, Craigslist, Offer up, eBay, etc., are great ways to sell your stuff and bring in some much-needed income.

If you are struggling with how to get out of debt, follow these steps to get your life back on track. The way you currently live isn’t working, so let’s make some drastic changes to improve your life!

4 Steps To Make Your Own “Get Out Of Debt Plan”

When you break it down, the strategy to get out of debt is rather simple. The difficulty is creating the plan in the first place and actually sticking with it. To make it clear, I will break down the easiest and fastest way to create your own get out of debt plan.

1. Create A Budget

Before you do anything, you need to know how much money you have coming in each month and how much money you have going out. If you are unfamiliar with how to start a budget, check out my related article: How to create a budget – for beginners.

A budget will give you a clear picture of how bad your financial situation is or how quickly you can make it better. I created a free budget spreadsheet that you can download and use. Click the image below to download a free blank copy.

A budget is the foundation of any debt-free plan. Without a monthly budget, you have little to no chance of taking control of your money and eliminating your financial stress.

2. Be Honest About Your “Needs” And “Wants”

Take an honest look at your budget and see where there is wasteful spending. Waste can be described as “elective spending” such as entertainment. Look for things in your budget that you spend money on each month but don’t need these things to survive.

This includes nail or hair appointments, going to the movies, eating out at restaurants – you get the idea. Total up how much you generally spend on these things.

The first step is to identify how much money you could have if you didn’t spend anything on elective items. Now let me be clear, I understand that some wasteful spending is important to maintain your sanity. It just needs to be in moderation.

Ultimately wasteful spending and getting out of debt are linked together.

Less wasteful spending = more money to go towards debt = get out of debt faster

That is the simple formula to get out of debt. You are the one who gets to make the ultimate decision of how quickly you want to get out of debt. The more you cut, the faster it will happen.

Wasteful Spending Can Hide In Necessities

The problem with wasteful, discretionary, or elective spending is its ability to disguise itself as “necessary spending.” For instance, we all agree that to survive, we need clothing, food, shelter, and transportation. However, most of us – including myself – spend more on these necessities than we should.

As I get into this list, please understand I’m not telling you how to live your life. I am giving ideas for you to evaluate and decide if it is right for you. If you are sick and tired of being broke and stressing about money, you may decide to drastically change your life and spending to change your future drastically.

Save Money On Clothing

While we all need clothing, many of us wear clothes that would make kings of old envious. While a $200 pair of jeans may be more comfortable than a $30 pair, imagine how much extra money you could save if you buy generic. Or, heaving forbid, you bought slightly used clothing from a second-hand store!

Again, this depends on how quickly you want to get out of debt but double-check how much money you spend on clothing and see where you can make cuts if you wanted to.

Save Money On Groceries

I am the first to admit that spending money on food is where I struggle the most. When it comes to food, I usually spend more than I should because I am lazy. Rather than packing my lunch every day, I find myself going through a drive-through to grab a quick meal – at a much higher price.

In addition, when I get home from work and my wife and I are tired, it is so much easier to take the family to a restaurant than it is to make dinner at home.

However, when the end of the month comes, and I see how much money I spent on food, it has never been worth it. Whenever I overspend, I am always filled with regret.

I have found that to combat my midweek laziness, meal prepping is the best way to go. Check out my related article, How to meal prep for beginners, if you need some direction on how to meal prep each week to save you a TON of money each month.

Get in the habit of shopping for groceries. There are many ways you can save money on food each month through mobile apps and create a grocery list. I have another good article further detailing this: Save money on groceries with these simple tips.

Save Money On Your Mortgage Or Rent

Did you know that the average size of a new home build in the United States is now 2,600 square feet? That is more than double the size of the average home in 1960! In America, we definitely subscribe to the theory that bigger is better – but is it really? With increased home sizes comes increased spending on rent and mortgages.

Take a look at your current living situation and decide if downsizing is an option. We have much more space in our homes than we “need,” and most of us could cut way down on our square footage and our mortgage.

Relocating to a cheaper area may also be a good idea. In Arizona, you will pay more for a home simply because of the city you live in. The cheaper cities aren’t necessarily more dangerous, but some stigmas come with certain names.

This is only a viable tactic to reduce your debt load if you really are paying significantly more for where you are currently living than you need to be. If you are moving for purely financial reasons, you need to consider all of the different costs associated with your move.

Movers will likely be the largest expense, but even if you do this all on your own, it can still be a time-consuming and expensive process. Read up on moving checklists to make sure you fully understand what you are getting yourself into and what can go wrong.

How much are you paying for stigmas each month?

Save Money On Your Vehicle Expenses

You knew this section was coming. Everyone has a car payment, right? Wrong. I don’t, and I haven’t had a car payment in over 10 years. Now before you pat me on the back, let me tell you about my stupid vehicle decisions.

When my wife and I first married, we spent about $1,300 a month on vehicle payments. Looking back, I have no idea how we could afford those payments. However, 10 years ago, we decided to buy vehicles with cash and eliminate car payments. The amount of money we have saved over the past 10 years is astronomical.

My wife and I now drive vehicles that are over 10 years old and are closing in on 200,000 miles. And guess what, they still work! I had no idea vehicles could last so long if you maintained them and paid money once in a while to change the oil, rotate the tires, redo the brakes, etc.

Seriously, before we bought two cheap vehicles with cash, I thought that it was basically worthless after a vehicle hit 100,000 miles. I was convinced that after 100,000 miles, I would be stranded on the road over and over again. It turns out I was totally wrong. Our two vehicles are still running strong, and I’m super excited for the day my car crosses the 200,000-mile mark – just for bragging rights!

Reevaluate your vehicle situation. Could you save money with a cheaper insurance company or a cheaper vehicle? It’s worth looking into.

3. Decide How Much Should Be In Your Emergency Fund

The short answer is: $1,500 to $2,000. However, there is much more you need to know about emergency savings accounts.

Before you consider a “get out of debt loan” that many companies will try and sell you through consolidations or debt forgiveness programs, why don’t you be your own bank?

Before you yell at me because you are broke and that “free stuff” is even too expensive for you, hear me out. If you have done your job and created a budget, and decided to cut some unnecessary spending, extra money should be leftover. If there’s not, you either need to cut more out of your budget or pick up a side hustle.

Now that you have made enough cuts or increased your income let’s figure out what to do with that extra money.

Before you start paying any of your debt off, you need an emergency fund to protect yourself from life. For instance, if you have $300 extra each month and start putting it all towards debt, what do you do when your car breaks down? You’re going to put it on a credit card.

In other words, 1 step forward, two steps back.

To start taking 2 steps forward and only 1 step back, you need to protect yourself with an emergency fund. An emergency fund is a savings account with cash in it that you can quickly access when life throws expensive problems your way.

By dipping into this fund and replenishing it immediately, you will avoid all the interest charges that credit card companies tack on. An emergency savings is similar to your own insurance policy – for yourself.

To learn more about emergency funds and how to set one up, refer to my related article: Everything you need to know about emergency funds.

How To Identify An Emergency And When You Should Use Your Emergency Fund

Your emergency savings is only for that – emergencies. When you run out of fun money at the end of the month and want to go to a movie, that does not constitute an emergency.

An emergency savings should be your priority so you can deal with life when it happens because it will happen. Your washer and vehicle will both break simultaneously, and having these savings will keep you from going further into debt.

If you take money from it, your priority next month will be to replenish it. After your saving is adequate, between $1,500 and $2000, you can start attacking your debts.

Track Your Progress With An Emergency Fund Coloring Page And Other Debt Free Charts!

I am a very visual person, so I need physical things to keep me motivated. I created free coloring pages to keep me motivated when we first started our debt-free journey. If you are a visual person like me, click the image below to pick up your own emergency fund coloring page!

4. Choose The Best Way To Get Out Of Debt

After you have a fully-funded emergency savings, it’s now time to attack our debt! As discussed earlier, identify all of your debts individually.

We will now methodically destroy one debt at a time while paying the minimum amount on all of your other debts. Again, this is where personal finance becomes personal. Each of us is motivated by different strategies, so which debt you pay off first depends on your own personality.

There are two major methods to get out of debt. The first method is the debt snowball method originally credited to Dave Ramsey.

The other more mathematically sound method is the debt avalanche. The debt snowball pays off the lowest total debt first before you move on to the next.

The avalanche method pays off the debt with the highest interest rate first. For a more detailed comparison, refer to my related article: The debt snowball vs. the debt avalanche.

When it all comes down to it, it doesn’t really matter which method you choose as long as you pick a method and stick with it. In the end, if you quit halfway through, it didn’t matter which plan you chose. It’s more important to choose to stick with it than which plan you decide to follow.

Use Undebt.it To Help You Pick The Right Debt Payoff Plan

I recently came across the website Undebt.it and spoke with the owner and creator of the site, Jeff Donaldson. He has a great vision of helping people get out of debt and even designed a free website application to do just that. His get out of debt app is the perfect solution if you are unsure which debt plan you should follow.

I gave the Undebt.it app a test drive, and I was impressed with how much Jeff offered, for free! Full disclosure, he does have a paid version that costs $1 a month, but the free version does enough to get you on track. I wrote a full review of the Undebt.it app here.

That’s Great But How Do I Get Out Of Debt Fast?

In our current environment, everything is given to us immediately. Google is there for quick answers, and credit cards give us a way to buy things without waiting. Waiting has become a thing of the past – for those who are willing to spend money.

Unfortunately, many of us got into debt without even knowing it. One day we woke up and realized how big of a mess we were in. As much as I would like to give you a quick and simple way to get out of debt fast, I will not lie to you. There is no quick and painless way to get out of debt.

Those who promise you a quick and easy way are salesmen. They sell refinance and debt consolidation products as the “best ways to get out of debt.” In reality, these products make them rich and keep you broke.

If you’re considering debt consolidation, check out my article before you make your decision.

Getting out of debt once and for all will take longer than you will want. However, once you finally get out, you will feel a sense of accomplishment that is nothing short of awesome. Your look on money will have changed, and you will be able to finally start building wealth while watching your financial stress melt away.

But I’m Broke, How Can I Get Out Of Debt?

If you’re in debt, you’re right – you’re broke. However, just because you are broke, that doesn’t mean you’re broken.

You’re broke because of some financial mistakes that were either your fault or something that was thrust upon you. Either way, you’re in debt, and it’s time to get out.

Even if you’re broke and on a low income, it’s still possible to get out of debt. By following the 4 steps above, even broke people can start to make progress. You’re either broke because you spend too much money, don’t make enough money or both. Control your spending, or you will never make enough to get out of debt.

Once you control how much you spend by creating a budget, you can focus on making more money with a side hustle or increasing your income at work. The steps to get out of debt don’t change – regardless of how much you do or do not make. Control spending and increasing income will ultimately be the key.

I Have A Bunch Of Credit Card Debt, How Do I Get Out Of It?

I recently met with someone who had 10 different credit cards, and most of them were maxed out. They had a strategy of moving their balances around to 0% interest cards, but that strategy quickly caught up with them. After a certain amount of time, the 0% interest would skyrocket to over 20%, and they frantically would move money around to make their minimum payments.

Unfortunately, this strategy is quite common as people struggle to stay above water. The best way to get out of credit card debt is to stop using them. Once and for all.

You could also consider a credit repair company, like Credit Saint. They can help you fix your credit score and repair the damage of credit card debt.

Credit cards and payday loans are created to make the lenders money at the expense of the borrower. It’s a terrible downward spiral that people find themselves in with no clear way to get out.

To get out of credit card debt, refuse to put any more money on them. Pay the minimum balance on every card except for one. Pay off one card at a time as quickly as you can.

Follow the steps above to create a budget and figure out what plan you will use to get out of debt. Is it the debt avalanche or the debt snowball? There’s no wrong answer as long as you pick a plan and stick with it.

Debt Settlement May Be An Option

If you’re broke, debt settlement may not be an option for you. However, if you have any money in your savings account, some credit card companies or debt collectors are willing to settle the debts for pennies on the dollar. For more information on negotiating with debt collectors and debt settlements, check out my related article below.

How My Wife And I Will (hopefully) Stay Debt Free For Life

Below is a flow chart I created to show how your monthly debt attack should work in order from most important to least. This is how my wife and I overcame our debt and now live a debt-free life.

Obviously, yours may look different depending on how many debts you have, but you get the idea. As you start, attack one debt at a time. Make the minimum required payments on the others as you knock out the first debt. After the first is eliminated, it’s time to move on to the next.

So as you can see, we put our money into our checking account and take out our monthly anticipated bills. After that, we attack our emergency savings. If your emergency fund isn’t fully funded, make minimum payments on all your debts until it is funded. After it is funded, we start on the debt.

I am a visual person, and I need aids to stay motivated. Right now, my wife and I are paying off our house. To see the progress, I put a glass jar in our kitchen and filled it with marbles. Each marble represents $1,000 towards the total amount left on our house. Each month as we pay down the principle, I take out the corresponding amount of marbles to physically see the debt going down.

You can use similar visual aids for your debts to stay motivated.

Some people use thermometers that they color and put on their fridges. Either way, find what works for you. Ultimately, you want to get to a point where your flow chart is not focused on debts because you have paid them off! Below is a similar chart that my wife and I now use.

From the charts, you can see where I started to where I am now. Soon, I will delete the “pay off house fund” because that is where the majority of my extra money goes now. That will be a fantastic day! It will happen for me because of the safeguards I have put in place and the vision I have for my family. You can be here too, and it will not take as long as you think!

With a clear strategy in place, you will see how quickly you can accomplish your goals.

I’m Debt Free! Now What?

After you have paid off all your debts, you need to increase your emergency fund except for your home. I recommend you save up to 6 months of living expenses (in cash) if you lose your job or income.

Other experts range from 3-8 months of expenses, so I decided to fall on the 6th-month mark to feel comfortable. That means if your monthly necessary bills are $2,000 a month, you need to save up $12,000 in your emergency savings. This protects you from a job loss or other significant financial disaster for at least 6 months.

Again, if you have any questions or comments, please reach out to me. I am here for you, and I am living proof this can be accomplished. You can get to a point where an unexpected vehicle repair does not need to go on a credit card. You can do it, and I will be here for you!

Originally Posted on arrestyourdebt.com