Introduction

Nvidia is currently one of the most favorite stocks of institutional and retail investors in 2024 with an year to date return of 130%. But what exactly is Nvidia, it is an American corporation and technology company, currently being one of the global market leaders in the semiconductor industry. Their main operations consist of creating graphics processing units (GPUs), application programming interfaces (APIs) that are used for gaming, professional visualization, data markets and more. Furthermore, they are one of the leaders with respect to delivering artificial intelligence (AI) hardware and software. Using their AI tools helps projects to reach production faster, better efficiency and improving performance at a lower cost. In this article we will take a closer look at the industry overview, competitive analysis, stock price in 2024, financial health and the investment opportunity.

Industry overview

In modern society, every electronic device from your phone, car, medical equipment to your electronic toothbrush is run on semiconductors. The industry has experienced exponential growth in the last years due to the rise of gaming, data centers, but even more important the rise of generative AI which will only become larger in the future. However, the industry is facing some major challenges related to geopolitical tension between Taiwan, China and the US as well as supply chain disruptions caused by a global production process and shortages of raw materials. Fortunately, companies are finding innovative solutions to overcome these challenges and gain a better market position.

Competitive analysis of Nvidia

The main competitors from Nvidia are Taiwan Semiconductors (TSM), AMD and Intel. Currently Nvidia is seen as the AI king with an approximation of owning 70 to 90% of the AI chip market. This is thanks to their high powered graphics processors that are needed in order to train AI models. For Nvidia, the demand towards their AI chips is exceeding their current supply. However, rivals like AMD and Intel are trying to catch up and steal some market share from Nvidia. Both companies are creating new AI chips and data center accelerators that are of similar quality and potentially cheaper. On the other hand, hyperscalers such as Google, Microsoft and Amazon are starting to build their own chips known as application specific integrated circuits (ASIC). These are chips that are specifically build for a company’s own AI needs and are more efficient in exercising one specific task. If these large companies build their own chips, this could harm the demand towards AI chips from Nvidia and other semiconductor companies.

Financials & ratios

In order to determine whether Nvidia is a healthy company rather than an overvalued and overhyped share, a closer look is taken into the financials in the company. In the following section the development of the income statement, cash flow statement and balance sheet throughout the years. Furthermore, some key financial ratios are taken into consideration to determine the healthiness of the company.

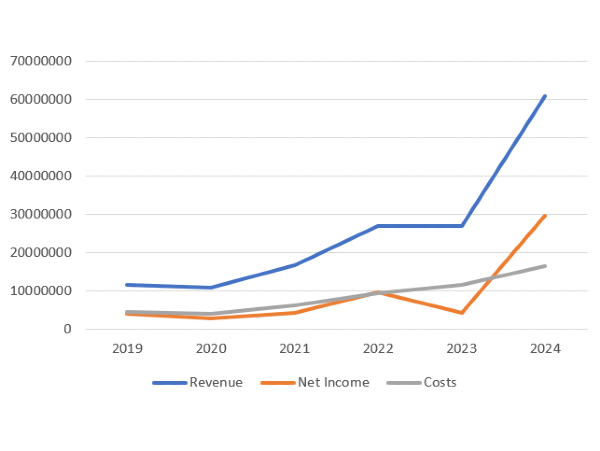

With respect to the income statement, the revenue of Nvidia has been increasing yearly with the only exception in 2023 where revenue remained similar to 2022 at $27 billion. In 2024 the revenue increased massively with 125% to a total revenue of circa $61 billion. Next, when looking at the costs, they do not increase substantially and therefore we see that Nvidia holds a strong gross margin of between 60%-70% in the last 5 years of trading, indicating efficient cost management and high profitability.

Further, the net income of Nvidia has been rather volatile throughout the years. 2020 was a bad year due to the covid-19 pandemic and its lockdowns. In 2023 the net income decreased with 55% from $9.7 to $4.4 billion due to rising operating expenses while the revenue remained stable. However, 2024 shows immense growth. Net income increased to a whopping $29.7 billion or an increase of 581%. Hence, the increasing demand towards Nvidia chips while maintaining their costs helps them to boost their profits. Another interesting ratio is the net income margin. From 2020 to 2023 it ranges between 16% and 36%. In 2024, the margin increased to 48%. Ultimately, showcasing solid bottom-line performance.

Figure 1: Key metrics income statement, 2019-2024

Continuing to the cash flow analysis which provides data regarding all cash in- and outflows that Nvidia receives from their operating activities as well as their external investment and financing activities. With respect to the operating cash flow (CFO), the cashflow has been growing at a strong pace with the exception of 2023. On average the CFO grew with 17% from 2020 to 2023. However, just as we saw in the income statement, in 2024 the CFO increased drastically from $5.6 to $28 billion which is equivalent to an increase of 398%. This reflects Nvidia’s efficient cash management and high profitability.

Next, when looking at the free cash flow (FCF) which represent the cash the company has available excluding non-cash expenses and includes spending on property plant & equipment as well as the change in working capital. A strong FCF can help the company payout dividends, pay debtholders or invest in new growth opportunities. Nvidia has seen its FCF grow significantly over the years with a total FCF in 2024 of $30.9 billion and once again an increase of 398% relative to 2023. Hence, they have plenty of cash to use for investing purposes or for equity holders. In their Q1 2024 earnings call they announced that they will implement a 10-1 stock split as well as a quarterly dividend increase to $0.01 per share on a post-split basis. This shows the commitment of Nvidia towards their shareholders and could potentially attract new investors that are looking for both growth and passive income.

The balance sheet of Nvidia further depicts a strong and healthy growth across all key aspects as can be seen in figure 2 below. The total assets have shown a steady increase over the years with a big jump in 2024, mainly thanks to the growth in the current assets. The key factors that caused the growth in the current assets are the rise in their short term investments as well as the increase in account receivables and cash. Hence, this highlights Nvidia’s expansion opportunities and improved liquidity.

With respect to liabilities, Nvidia is able to keep both their total and current liabilities at manageable levels and at the same time the liabilities grow at a slower rate compared to its assets. This reflects that Nvidia is able to manage their debt and obligations efficiently. For 2024, the rise in total liabilities comes from the rise in current liabilities which is affected by the increase in account payables. Furthermore, the total equity of Nvidia skyrocketed in 2024 as well, almost doubling from the previous year. The reason behind this jump is the increase of the retained earnings which represent the amount of net income left over for the business after it has paid out dividends to its shareholders. Because Nvidia pays out relatively low dividends, they can use the retained earnings to invest in expansion activities like increasing their production capacity.

Some other worthy ratios to mention are the current ratio, quick ratio, debt to equity ratio and asset turnover ratio. Starting with the current ratio which measures the ability to use pay your current liabilities using your current assets. For Nvidia, the current ratio equals 4.17 indicating strong short term financial health. If we only want to consider cash equivalents, the quick ratio is used which excludes inventory from the current assets since inventory needs to be sold before the cash can be used to pay the current liabilities. The quick ratio is 3.38 highlighting excellent liquidity without relying on inventory.

Moving over to the debt to equity (D/E) ratio which tells us something about the capital structure and leverage of the company. The D/E ratio has been decreasing over the last years, while it was around 0.45-0.55 from 2021 until 2023. In 2024 the ratio decreased to 0.26 indicating that equity outgrew the growth in debt. This further implies that Nvidia has a strong balanced approach to leveraging debt and in the future they have the ability to take on new debt to invest in R&D and further expansion of the company. This is also in line with the interest coverage ratio which measures how many times your EBIT covers the interest expenses. This ratio currently is 129.22 so Nvidia has to problem paying their interest expenses on their debt.

Finally we have some asset ratios to consider. First the return on assets (ROA) which measures how efficiently Nvidia uses their assets to generate income. The current ROA is 58.34% indicating that for every dollar of assets, Nvidia generates 58 dollar cents of net income. This improved drastically since the ROA of 2023 was only 10.18%.

Figure 2: Balance sheet progress

Analyst and valuation forecasts

Analysts have a positive outlook on Nvidia with many rating it a “buy” due to its strong growth prospects in the AI sector and market leadership. Recent price targets from leading analysts like Morningstar, Citibank, JPM etc. have an average fair value estimation of $1050, with other valuations ranging between $500-$1400. However, it is noteworthy that the current price to earnings ratio is 84 even after the most recent price rally of Nvidia. This is very high and investors have to pay a large premium for the share because many investors expect that the company is going to increase in price or will have larger earnings in the future. Hence, investors should trade with caution as the price to earnings ratio of other semiconductor companies (Besi, ASML, Intel, TSMC) range between 25-50. Indicating that Nvidia might be a overvalued compared to the industry average.

Conclusion

Nvidia stands out as a powerhouse in the semiconductor industry, driven by its strategic focus on AI and market-leading GPUs. The company's remarkable revenue growth, high profitability margins, and impressive cash flow generation underscore its robust financial health. Nvidia effectively manages its liabilities while significantly increasing its assets and equity, showcasing prudent financial management. Key financial ratios such as the current ratio, quick ratio, and debt-to-equity ratio further highlight Nvidia's excellent liquidity and balanced capital structure.

Analysts are optimistic about Nvidia's continued growth prospects and market leadership, particularly in the AI chip market where it holds a significant share. However, the high price-to-earnings ratio suggests that investors are paying a premium for Nvidia's stock, indicating potential overvaluation relative to industry peers. While Nvidia presents a compelling investment opportunity due to its strong market position and growth potential, investors should approach with caution, considering the premium valuation and potential market volatility. Overall, Nvidia's strategic initiatives and financial strength make it an attractive investment for those seeking exposure to the rapidly growing AI and semiconductor sectors.

I/we have no positions in any asset mentioned, but may initiate a position over the next 7 days

Introduction

Nvidia is currently one of the most favorite stocks of institutional and retail investors in 2024 with an year to date return of 130%. But what exactly is Nvidia, it is an American corporation and technology company, currently being one of the global market leaders in the semiconductor industry. Their main operations consist of creating graphics processing units (GPUs), application programming interfaces (APIs) that are used for gaming, professional visualization, data markets and more. Furthermore, they are one of the leaders with respect to delivering artificial intelligence (AI) hardware and software. Using their AI tools helps projects to reach production faster, better efficiency and improving performance at a lower cost. In this article we will take a closer look at the industry overview, competitive analysis, stock price in 2024, financial health and the investment opportunity.

Industry overview

In modern society, every electronic device from your phone, car, medical equipment to your electronic toothbrush is run on semiconductors. The industry has experienced exponential growth in the last years due to the rise of gaming, data centers, but even more important the rise of generative AI which will only become larger in the future. However, the industry is facing some major challenges related to geopolitical tension between Taiwan, China and the US as well as supply chain disruptions caused by a global production process and shortages of raw materials. Fortunately, companies are finding innovative solutions to overcome these challenges and gain a better market position.

Competitive analysis of Nvidia

The main competitors from Nvidia are Taiwan Semiconductors (TSM), AMD and Intel. Currently Nvidia is seen as the AI king with an approximation of owning 70 to 90% of the AI chip market. This is thanks to their high powered graphics processors that are needed in order to train AI models. For Nvidia, the demand towards their AI chips is exceeding their current supply. However, rivals like AMD and Intel are trying to catch up and steal some market share from Nvidia. Both companies are creating new AI chips and data center accelerators that are of similar quality and potentially cheaper. On the other hand, hyperscalers such as Google, Microsoft and Amazon are starting to build their own chips known as application specific integrated circuits (ASIC). These are chips that are specifically build for a company’s own AI needs and are more efficient in exercising one specific task. If these large companies build their own chips, this could harm the demand towards AI chips from Nvidia and other semiconductor companies.

Financials & ratios

In order to determine whether Nvidia is a healthy company rather than an overvalued and overhyped share, a closer look is taken into the financials in the company. In the following section the development of the income statement, cash flow statement and balance sheet throughout the years. Furthermore, some key financial ratios are taken into consideration to determine the healthiness of the company.

With respect to the income statement, the revenue of Nvidia has been increasing yearly with the only exception in 2023 where revenue remained similar to 2022 at $27 billion. In 2024 the revenue increased massively with 125% to a total revenue of circa $61 billion. Next, when looking at the costs, they do not increase substantially and therefore we see that Nvidia holds a strong gross margin of between 60%-70% in the last 5 years of trading, indicating efficient cost management and high profitability.

Further, the net income of Nvidia has been rather volatile throughout the years. 2020 was a bad year due to the covid-19 pandemic and its lockdowns. In 2023 the net income decreased with 55% from $9.7 to $4.4 billion due to rising operating expenses while the revenue remained stable. However, 2024 shows immense growth. Net income increased to a whopping $29.7 billion or an increase of 581%. Hence, the increasing demand towards Nvidia chips while maintaining their costs helps them to boost their profits. Another interesting ratio is the net income margin. From 2020 to 2023 it ranges between 16% and 36%. In 2024, the margin increased to 48%. Ultimately, showcasing solid bottom-line performance.

Figure 1: Key metrics income statement, 2019-2024

Continuing to the cash flow analysis which provides data regarding all cash in- and outflows that Nvidia receives from their operating activities as well as their external investment and financing activities. With respect to the operating cash flow (CFO), the cashflow has been growing at a strong pace with the exception of 2023. On average the CFO grew with 17% from 2020 to 2023. However, just as we saw in the income statement, in 2024 the CFO increased drastically from $5.6 to $28 billion which is equivalent to an increase of 398%. This reflects Nvidia’s efficient cash management and high profitability.

Next, when looking at the free cash flow (FCF) which represent the cash the company has available excluding non-cash expenses and includes spending on property plant & equipment as well as the change in working capital. A strong FCF can help the company payout dividends, pay debtholders or invest in new growth opportunities. Nvidia has seen its FCF grow significantly over the years with a total FCF in 2024 of $30.9 billion and once again an increase of 398% relative to 2023. Hence, they have plenty of cash to use for investing purposes or for equity holders. In their Q1 2024 earnings call they announced that they will implement a 10-1 stock split as well as a quarterly dividend increase to $0.01 per share on a post-split basis. This shows the commitment of Nvidia towards their shareholders and could potentially attract new investors that are looking for both growth and passive income.

The balance sheet of Nvidia further depicts a strong and healthy growth across all key aspects as can be seen in figure 2 below. The total assets have shown a steady increase over the years with a big jump in 2024, mainly thanks to the growth in the current assets. The key factors that caused the growth in the current assets are the rise in their short term investments as well as the increase in account receivables and cash. Hence, this highlights Nvidia’s expansion opportunities and improved liquidity.

With respect to liabilities, Nvidia is able to keep both their total and current liabilities at manageable levels and at the same time the liabilities grow at a slower rate compared to its assets. This reflects that Nvidia is able to manage their debt and obligations efficiently. For 2024, the rise in total liabilities comes from the rise in current liabilities which is affected by the increase in account payables. Furthermore, the total equity of Nvidia skyrocketed in 2024 as well, almost doubling from the previous year. The reason behind this jump is the increase of the retained earnings which represent the amount of net income left over for the business after it has paid out dividends to its shareholders. Because Nvidia pays out relatively low dividends, they can use the retained earnings to invest in expansion activities like increasing their production capacity.

Some other worthy ratios to mention are the current ratio, quick ratio, debt to equity ratio and asset turnover ratio. Starting with the current ratio which measures the ability to use pay your current liabilities using your current assets. For Nvidia, the current ratio equals 4.17 indicating strong short term financial health. If we only want to consider cash equivalents, the quick ratio is used which excludes inventory from the current assets since inventory needs to be sold before the cash can be used to pay the current liabilities. The quick ratio is 3.38 highlighting excellent liquidity without relying on inventory.

Moving over to the debt to equity (D/E) ratio which tells us something about the capital structure and leverage of the company. The D/E ratio has been decreasing over the last years, while it was around 0.45-0.55 from 2021 until 2023. In 2024 the ratio decreased to 0.26 indicating that equity outgrew the growth in debt. This further implies that Nvidia has a strong balanced approach to leveraging debt and in the future they have the ability to take on new debt to invest in R&D and further expansion of the company. This is also in line with the interest coverage ratio which measures how many times your EBIT covers the interest expenses. This ratio currently is 129.22 so Nvidia has to problem paying their interest expenses on their debt.

Finally we have some asset ratios to consider. First the return on assets (ROA) which measures how efficiently Nvidia uses their assets to generate income. The current ROA is 58.34% indicating that for every dollar of assets, Nvidia generates 58 dollar cents of net income. This improved drastically since the ROA of 2023 was only 10.18%.

Figure 2: Balance sheet progress

Analyst and valuation forecasts

Analysts have a positive outlook on Nvidia with many rating it a “buy” due to its strong growth prospects in the AI sector and market leadership. Recent price targets from leading analysts like Morningstar, Citibank, JPM etc. have an average fair value estimation of $1050, with other valuations ranging between $500-$1400. However, it is noteworthy that the current price to earnings ratio is 84 even after the most recent price rally of Nvidia. This is very high and investors have to pay a large premium for the share because many investors expect that the company is going to increase in price or will have larger earnings in the future. Hence, investors should trade with caution as the price to earnings ratio of other semiconductor companies (Besi, ASML, Intel, TSMC) range between 25-50. Indicating that Nvidia might be a overvalued compared to the industry average.

Conclusion

Nvidia stands out as a powerhouse in the semiconductor industry, driven by its strategic focus on AI and market-leading GPUs. The company's remarkable revenue growth, high profitability margins, and impressive cash flow generation underscore its robust financial health. Nvidia effectively manages its liabilities while significantly increasing its assets and equity, showcasing prudent financial management. Key financial ratios such as the current ratio, quick ratio, and debt-to-equity ratio further highlight Nvidia's excellent liquidity and balanced capital structure.

Analysts are optimistic about Nvidia's continued growth prospects and market leadership, particularly in the AI chip market where it holds a significant share. However, the high price-to-earnings ratio suggests that investors are paying a premium for Nvidia's stock, indicating potential overvaluation relative to industry peers. While Nvidia presents a compelling investment opportunity due to its strong market position and growth potential, investors should approach with caution, considering the premium valuation and potential market volatility. Overall, Nvidia's strategic initiatives and financial strength make it an attractive investment for those seeking exposure to the rapidly growing AI and semiconductor sectors.

I/we have no positions in any asset mentioned, but may initiate a position over the next 7 days