Key Notes

- Utilities are stable businesses. Use their stability to your advantage when assessing the stock

- A discounted earnings model, taking book value per share into account, works well in assessing a utility’s intrinsic value.

- When assessing the value of a stock, the dividend is immaterial

- Earnings and earnings growth are critical

- Book value is much more important with utilities as accountants can more accurately assess the assets of the company, making it a valuable metric

- Interest rates matter, be sure to discount future earnings by the 10-year treasury bond rate

- It can take two years for a utility to readjust to its valuation

Are Utilities Considered Value Stocks?

Utility stocks are a poster child for value stocks. You can use value investing tools to value any stock; however, utilities are consistent, well-regulated companies whose demand for their product is continuous and rarely changed by economic conditions. Hence, discrepancies in a utilities price versus their intrinsic value are typically low and a large deviation can be a sign of a big opportunity or a significant malfunction of the company.

An example of a big opportunity was in 2008 when the stock market crashed. Utilities were significantly undervalued by the market due to the shear lack of liquidity available to buy up cheap assets. An example of a company malfunctioning was when PG&E had to file bankruptcy after being indicted for causing major forest fires in California.

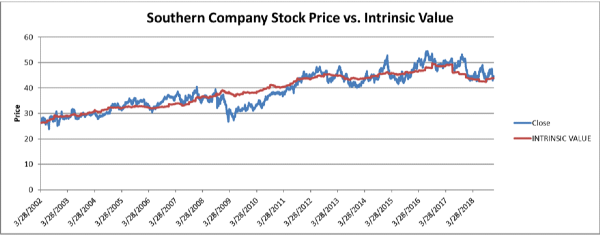

A utility’s stock price will follow the intrinsic value of a company very closely. It will revert to the intrinsic value in 2-year cycles.

Why are Utilities a Good Investment?

Utilities are the teapot ride at Disneyland. You’re not going to get as much excitement, but you’ll consistently have a fun and safe time. Utilities offer a business with low volatility and consistent dividends. This usually results in a slow but growing appreciation of the company. Nonetheless, in the last five years, electric companies had their worst drawdowns of 30% to 50%.

Overall, utility stocks are great for income generation portfolios. They may also be used for wealth preservation strategies; however, they likely will be the riskiest asset in the portfolio.

Are Utility Stocks a Safe Investment?

Utility stocks are the safest stock sector. The trade-off to this safety is that utilities will lag behind the overall market.

What Makes a Good Utility Stock Investment

There is a big difference between an undervalued company and a quality company to invest in long-term. While an undervalued company has a discrepancy between its intrinsic value and its market value, a quality company has leadership, processes and culture that will lead to continued earnings growth and asset accumulation.

A good utility stock investment has the following traits:

- Leadership with a strong vision for the company’s future

- A strong focus on stability and growth

- A strong management of risk including environmental, regulatory, and technical

- Strong stewardship of capital as seen in selective capital projects and dividend policy

How to Value Utility Stocks

1). Estimate Future Earnings

Start with the trailing twelve-month (ttm) earnings per share. Take the last ten years average growth rate and use the average of this growth rate to extrapolate the next ten years of earnings. Double check your growth estimate against the company’s own forecasts on earnings growth. Take the more conservative growth rate.

To estimate future earnings, its critical to assess the utility's recent quarter earnings growth. Typically, utilities will use a earnings bridge chart to present their recent EPS growth.

2). Discount the 10-year Treasure rate

Discount the 10-year treasury rate by taking the interest rate and dividing it into your forecasted earnings. As the years get further into the future, you must divide by the interest rate to the power of that year. For example, year 4 would have a discounted earnings value of:

Year four forecasted earnings / (1 + 10-year treasury rate) ^ 4

3). Add Book Value per Share

Take all your discounted earnings and add them up. This is the net present value of the company’s earnings. Add this value to the book value per share of the company. This is the intrinsic value of the company

Why Utility Investments are Held for Two Years Minimum

Alright, so I went through the secret formula, now why is this effective. Let’s use data to show why this process is consistent. The key here is realizing the market takes two-years to correct.

From randomness to Order

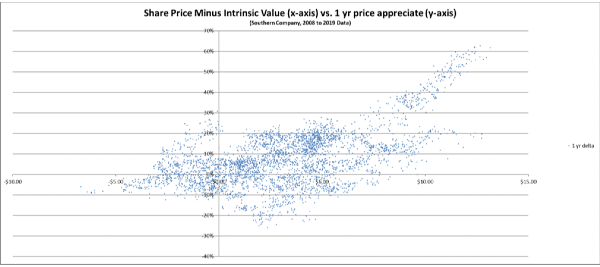

Let’s look at our calculated intrinsic value versus the future price movement of a stock. For example, let’s see how our stock behaves one year AFTER we have calculated our intrinsic value:

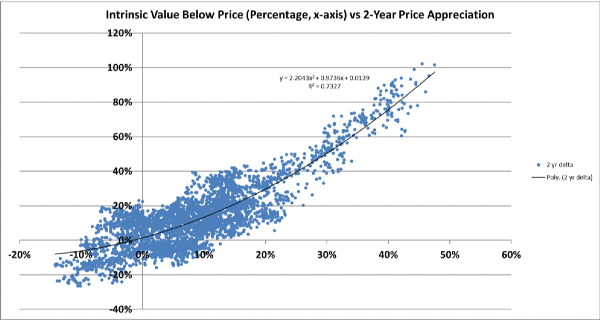

Looks chaotic, but it seems to have a bit of shape. What happens if we look into the future two years into the future:

Whoa! That’s a weird consistency coming from random stock data. A correlation of 0.73 is not even close for science, but in the stock market that is an anomaly indeed.

As value investor Benjamin Graham said in his book “The Intelligent Investor”[1]

"[The Stock Market] Is in the short run a voting machine, in the long run a weighing machine."

As you can see in the chart, the right side seems to be light and undervalued, while the left side is weighted down by the over-valuation of the company.

Book value per share

One reason utilities are easier to evaluate is that their assets are mostly tangible allowing accountants to accurately report a book value of the company. This is much easier than a company like Disney. Disney has intangible assets like trademark and licensing rights to characters and entertainment franchises. A utility’s assets are equipment, plants, and cash. Accountant standard and practices work well for you to give you a clear picture of the company’s current worth since they don’t have intangible assets that don’t have straight forward values.

Read More: Why is Book Value Important?

Earnings and Earnings Growth

Earnings is the purest metric you need to calculate the value of a utility stock. Earnings is not the right metric for all companies. Growth focused companies, especially technology stocks, are best valued based on revenue and revenue growth. Earnings is important for utilities because utilities don’t have to battle hard to keep customers. Utilities are really battling the entropy of rising costs and inefficiencies in their production.

Earnings growth shows that their continuous improvement initiatives, which are capital costs, can affect the bottom line and are not being wasted. Capital projects, maintenance, and training are all continuous projects that must be managed diligently, or they become wasted costs. Diligence is hard to keep up quarter after quarter, and a slip in diligence will reflect a laziness of the executive team that translates into poor earnings growth.

Ultimately, earnings and earnings growth encapsulate the overall management of the company. This value analysis must be backed up by a qualitative analysis because continued earnings growth cannot be forecasted by numbers but purely by the initiative of the executive team.

Interest Rates

Interest rates directly affect the valuation of stocks by giving investors a safer investment alternative. If that safer alternative is also providing a better return rate, institutional investors will instinctively flock to those higher, safer, returns. To take this phenomenon into account, we discount the earnings by the interest rate. This means that if interest rates are 2% annually, we remove that 2% from the earnings percentage of the utility we are assessing. That 2% is free money we can get in another investment, so the utility needs to do better than that to take our investment.

Discounting earnings by the interest rate is effective because it’s a calculation done all the time by institutional and retail investors. Sometimes they will do a dividend discount model. This model discounts the dividends being returned by the utility. Institutional investors may also run a discounted cash flow model as well. Regardless of the model, the concept is the same. Dividends, earnings, and cash flow can all be manipulated by the company to reflect a good standing company, but ultimately, these all need to continue growing or the company’s management is ineffective.

Determining if a Utility is Undervalued

All this analysis converges to one question: is this utility a buy? Utilities are very interesting, because they don’t require a large risk factor for investors to jump on.

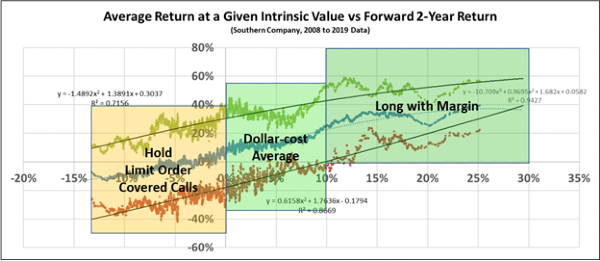

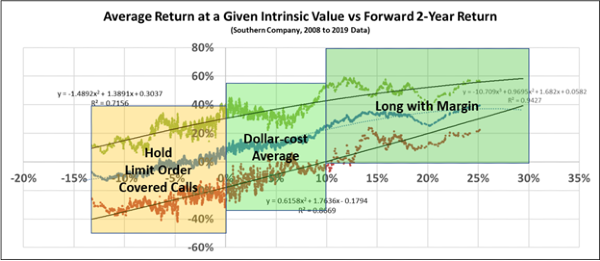

The graph above shows the average 2-year return (in blue) at a price point that is a percentage below intrinsic value. This graph is indifferent to a date. The green and red are 3-sigma distributions from the average. The larger the difference between red and green the more volatility at the point.

You can make some generalizations on what actions to take from this information:

- If the stock’s intrinsic value is 10% higher than the current price, the stock in undervalued. This is an accumulation phase

- If the stock’s intrinsic value is 0% to 9% higher than the current price, this is a good hold phase. The dividend rate will supplement price appreciation stagnation.

- If the stock’s intrinsic value is less than its current price, the stock should have trade limits placed on holdings. During these times, momentum may drive the stock higher, but a 5% to 10% fall in price is a good time to reduce your position.

Advanced Topics

The above section should help beginner investors take their stock analysis to the next level. These patterns in investing are the same for many different stocks. Stock’s that don’t hold this pattern are either highly speculative, poorly managed, or very growth focused. A stock that does not hold this pattern isn’t a bad stock, but they are not good for income focused or wealth preservation focused portfolios.

When to Use Margin

Margin is debt provided to you by the broker to buy investments. Using margin is very risky because you can lose more money than your initial investment. However, margin is a great way to amplify your returns, especially with utilities.

Warning: this is an advanced technique. Do not use margin until you are comfortable investing. We suggest only using margin sparingly. Overuse of margin may result in catastrophic loss during black swan events

Based on our analysis of Southern Company, the best time to use margin is when the price of Southern Company is 10% below its intrinsic value. Even better, if the stock is 20% below its intrinsic value, it may be good to have 5% to 10% of your investment be margin.

Margin has an interest rate you must pay. If this interest rate cannot be covered by your dividends, it may not be good to use margin, even if the stock is significantly undervalued. This is because a stock needs time to recover, and this recovery can take two years to occur.

Accumulation Phase

Looking at the graph again, you can see that roughly 5% to 10% below the intrinsic value is an accumulation phase. Here, you can buy stock using a dollar-cost averaging strategy. You can continue to keep your margin for previous stock you’ve bought but at this point it is not worth adding more margin.

De-Risking Phase

When the stock’s price is +/-5% of the intrinsic value, start de-risking your position. You can stop dollar-cost averaging and instead sell your stock positions for a profit if possible. Use these proceeds to clear your margin. This process alone should give you an easy 10% to 15% gain while still holding the stock without any more margin.

Utilizing Cover Calls and Limit Sells

The stock will stay in the +/-5% range for a while, so its best to let it be until it falls out of this range. As we’ll show in our theories section, this range is the most volatile price interval the stock can be in. If the price falls back into a value position, accumulate. If it starts to appreciate higher, then it’s overvalued by the market.

When the stock is overvalued, use two advanced techniques to continue profiting even while you’re trying to sell your position. The first is to use a limit order. Place a limit order 5% to 10% below the current price. If the price increases, raise your limit order line accordingly.

Use covered calls to make money on the option fees while also giving yourself a synthetic limit order on the upside. The covered call will let us get out of our position if momentum gets too strong while still profiting from the fees.

Do not ever regret missing additional upside

Momentum is a real phenomenon and even utilities can be driven by momentum. Do not regret missing out on further momentum upward as you’ll be expending unnecessary stress trying to “time the market”. Get out knowing that you’re winning a lot more by investing consistently and patiently.

Warning: if the stock price falls and you have a covered call option and a limit order on your stocks. Be sure the covered call option is closed before the limit order is met. Do not sell a call option without the underlying asset as backup unless you’re an advanced options trader

Why We Don’t Care About Other Financial Values

This section is for the financial nerds out there. These topics aren’t for new investors, but feel free to read on if you’re curious

Why Dividends Don’t Matter When You’re Valuing a Utility Stock

We clearly saw in our analysis of the best electric utility companies that companies who push dividends as their main attraction to investors have more volatility, poor stock appreciation, and larger drawdowns. Dividends don’t matter in assessing a utility stock when you’re determining its valuation, or the price you want to buy the stock at.

Dividend policy and management strength matter significantly when deciding which utility to invest in. Even though a utility may be undervalued, that doesn’t mean it’s a good buy. Management malfunction can completely break down an analysis like this.

Getting back to dividends, the key reason why they don’t help in valuing the company is because they are artificially made by the board. If the dividend is 70% of earnings or higher (this is the dividend payout ratio) then the company is basically giving away all their earnings without thinking long term about continuously improving the business. This means the company is sacrificing earnings growth for dividends. Any company that does this for too long will see earnings fall, which will be catastrophic for the company’s stock price.

Dividends are important to determine if a utility is right for you, but it shouldn’t be used to evaluate the company’s intrinsic value.

Cashflow

Cashflow is a great measure of a company’s value. Cashflow growth is a good indication of a well-managed company. Nonetheless, cashflow can obscure real company growth. One-time costs like fees can make cashflow look poor, while the truth is that earnings were solid. For a utility, earnings can give a better sense of the overall value of the company instead of cashflow.

Revenue

Revenue is the premier financial metric when looking at technology companies, start-ups, and high-growth companies. When revenue increases, it means the company is forging new markets or disrupting old ones. Price movement of technology stocks historically correlate better with revenue than earnings. In many cases, earnings may be zero or negative for years as the company burns through capital to disrupt their market.

However, for utilities, you can predict revenue growth by simply monitoring population growth. Utilities that operate in areas with a population growth will see an increase in demand. Regulated utilities have a monopoly in their area and so revenue directly correlates to population. And even if a utility can increase revenue, their profit margins are low. In Q3 2022, AEP’s profit margin was only 13.08%[2].

Utilities must fight the constant corrosion of energy costs to their bottom line. Hence significant revenue increase may be irrelevant if a management team cannot turn a profit on the revenue.

Red Flags

Our value analysis gives you a big advantage when assessing a stable, profitable, well managed company. But value investors measure multiple qualitative metrics like executive team quality and company culture. Why though? The answer is that poor company quality will lead to bad practices and poor culture which will undermine the stock’s consistency. Here are some red flags that can occur due to mismanagement.

Book Value per Share is Plummeting

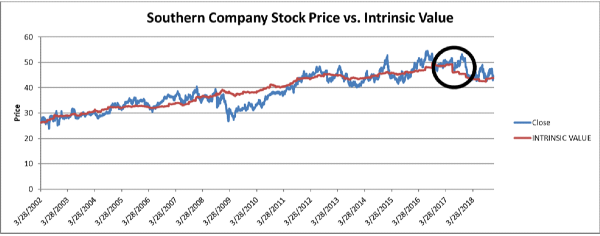

The book value per share of a utility should steadily increase overtime. Small fluctuations downward are typically no more than random variability. But if a company writes off a poor investment or burns too much cash, you could see book value per share plummet.

In the graph above, the sharp drop in intrinsic value was due to a drop in book value per share. Inevitably, the price readjusted back down accordingly

Book value per share may drop for the falling reasons (this list is not exhaustive):

- Accountants write off a failed investment

- Negative earnings

- A significant increase in debt, with the money being burned through fees, legal issues, or dividends.

Earnings growth is negative

Earnings growth will fluctuate every quarter. However, years of negative earnings growth is a signal of a potential disaster. When a utility cannot turn around earnings growth, keep away from the utility until they can prove they can turn it around. A new executive team cannot immediately turn earnings growth around and for income investors its not wise to speculate on new executive teams.

Payout Ratio is Too High

A utility company that pays out a dividend higher than their earnings needs to be avoided until their dividend policy is adjusted. A utility is always looking for investors so that it can raise its stock price. That’s an inherent quality of companies. For utilities, the dividend alone can sometimes entice income investors and ETFs to buy into the utility. This may come at the expense of the long-term prospects of the company as too much money is allocated to dividends instead of the business’s continuous improvement.

Theories

Warning, we are deviating significantly from “beginners’ topics” in this section

Momentum and Value Investing Intertwined

A conjecture made from looking at the 2-year forward looking movements of stocks is that momentum and value investing are intertwined phenomena. When the price of a stock is significantly undervalued, momentum starts to accumulate as the price tries to get back to intrinsic value. Once intrinsic value is reached, momentum seems to consistently pull the price up significantly past the base intrinsic value. Inevitably, another pull back occurs again. This cycle of undervaluation, momentum up to overvaluation, and then a correction seems to happen in roughly 2-year intervals for utility stocks.

Utility stocks in particular show this cycle possibly due to their low volatility of the underlying intrinsic value of the company.

The Money is in Volatility

When a stock is near its intrinsic value, it seems to be the most volatile. It seems that the market just doesn’t want it to stay at that price. The conjecture is that while the “efficient market” is satisfied with the price, this part of the market stops partaking in the price movement. What’s left are traders, market makers, and investors changing their position for non-efficient reasons. For example, an ETF will buy more shares of the utility to meet an arbitrary portfolio percentage. Or a retail investor will sell their shares to take a vacation. Traders and market makers are likely pushing the price of the stock away from the intrinsic value so that they themselves can make their own profit on the transaction.

This may be why the price of a stock is most volatile when its at or near the intrinsic value of the stock. All efficient participants are satisfied with the price and don’t partake in trading, leaving volume to be controlled by participants who need volatility for their own profit.

Conclusion

The discounted earnings model is the best way to value a utility stock. A utility’s unique business characteristics can give you an opportunity to evaluate the intrinsic value of the company with confidence. Nonetheless, be sure to run a qualitative analysis of the company as well. Be sure the executive team has a clear vision to grow the company and are building processes and cultures to meet that vision.

The Top Utility Stocks

Our community is writing new analysis every day to help you find undervalued investment opportunities. Check out these top lists to find new investment ideas:

References

1.) The Intelligent Investor, Mr. Market as summarized on Wikipedia

2.) AEP key statistics from Yahoo! Finance

Key Notes

Are Utilities Considered Value Stocks?

Utility stocks are a poster child for value stocks. You can use value investing tools to value any stock; however, utilities are consistent, well-regulated companies whose demand for their product is continuous and rarely changed by economic conditions. Hence, discrepancies in a utilities price versus their intrinsic value are typically low and a large deviation can be a sign of a big opportunity or a significant malfunction of the company. An example of a big opportunity was in 2008 when the stock market crashed. Utilities were significantly undervalued by the market due to the shear lack of liquidity available to buy up cheap assets. An example of a company malfunctioning was when PG&E had to file bankruptcy after being indicted for causing major forest fires in California.

A utility’s stock price will follow the intrinsic value of a company very closely. It will revert to the intrinsic value in 2-year cycles.

Why are Utilities a Good Investment?

Utilities are the teapot ride at Disneyland. You’re not going to get as much excitement, but you’ll consistently have a fun and safe time. Utilities offer a business with low volatility and consistent dividends. This usually results in a slow but growing appreciation of the company. Nonetheless, in the last five years, electric companies had their worst drawdowns of 30% to 50%. Overall, utility stocks are great for income generation portfolios. They may also be used for wealth preservation strategies; however, they likely will be the riskiest asset in the portfolio.

Are Utility Stocks a Safe Investment?

Utility stocks are the safest stock sector. The trade-off to this safety is that utilities will lag behind the overall market.

What Makes a Good Utility Stock Investment

There is a big difference between an undervalued company and a quality company to invest in long-term. While an undervalued company has a discrepancy between its intrinsic value and its market value, a quality company has leadership, processes and culture that will lead to continued earnings growth and asset accumulation.

A good utility stock investment has the following traits:

How to Value Utility Stocks

1). Estimate Future Earnings

Start with the trailing twelve-month (ttm) earnings per share. Take the last ten years average growth rate and use the average of this growth rate to extrapolate the next ten years of earnings. Double check your growth estimate against the company’s own forecasts on earnings growth. Take the more conservative growth rate.

To estimate future earnings, its critical to assess the utility's recent quarter earnings growth. Typically, utilities will use a earnings bridge chart to present their recent EPS growth.

2). Discount the 10-year Treasure rate

Discount the 10-year treasury rate by taking the interest rate and dividing it into your forecasted earnings. As the years get further into the future, you must divide by the interest rate to the power of that year. For example, year 4 would have a discounted earnings value of:

Year four forecasted earnings / (1 + 10-year treasury rate) ^ 4

3). Add Book Value per Share

Take all your discounted earnings and add them up. This is the net present value of the company’s earnings. Add this value to the book value per share of the company. This is the intrinsic value of the company

Why Utility Investments are Held for Two Years Minimum

Alright, so I went through the secret formula, now why is this effective. Let’s use data to show why this process is consistent. The key here is realizing the market takes two-years to correct.

From randomness to Order

Let’s look at our calculated intrinsic value versus the future price movement of a stock. For example, let’s see how our stock behaves one year AFTER we have calculated our intrinsic value:

Looks chaotic, but it seems to have a bit of shape. What happens if we look into the future two years into the future:

Whoa! That’s a weird consistency coming from random stock data. A correlation of 0.73 is not even close for science, but in the stock market that is an anomaly indeed.

As value investor Benjamin Graham said in his book “The Intelligent Investor”[1]

"[The Stock Market] Is in the short run a voting machine, in the long run a weighing machine."

As you can see in the chart, the right side seems to be light and undervalued, while the left side is weighted down by the over-valuation of the company.

Book value per share

One reason utilities are easier to evaluate is that their assets are mostly tangible allowing accountants to accurately report a book value of the company. This is much easier than a company like Disney. Disney has intangible assets like trademark and licensing rights to characters and entertainment franchises. A utility’s assets are equipment, plants, and cash. Accountant standard and practices work well for you to give you a clear picture of the company’s current worth since they don’t have intangible assets that don’t have straight forward values.

Earnings and Earnings Growth

Earnings is the purest metric you need to calculate the value of a utility stock. Earnings is not the right metric for all companies. Growth focused companies, especially technology stocks, are best valued based on revenue and revenue growth. Earnings is important for utilities because utilities don’t have to battle hard to keep customers. Utilities are really battling the entropy of rising costs and inefficiencies in their production.

Earnings growth shows that their continuous improvement initiatives, which are capital costs, can affect the bottom line and are not being wasted. Capital projects, maintenance, and training are all continuous projects that must be managed diligently, or they become wasted costs. Diligence is hard to keep up quarter after quarter, and a slip in diligence will reflect a laziness of the executive team that translates into poor earnings growth. Ultimately, earnings and earnings growth encapsulate the overall management of the company. This value analysis must be backed up by a qualitative analysis because continued earnings growth cannot be forecasted by numbers but purely by the initiative of the executive team.

Interest Rates

Interest rates directly affect the valuation of stocks by giving investors a safer investment alternative. If that safer alternative is also providing a better return rate, institutional investors will instinctively flock to those higher, safer, returns. To take this phenomenon into account, we discount the earnings by the interest rate. This means that if interest rates are 2% annually, we remove that 2% from the earnings percentage of the utility we are assessing. That 2% is free money we can get in another investment, so the utility needs to do better than that to take our investment. Discounting earnings by the interest rate is effective because it’s a calculation done all the time by institutional and retail investors. Sometimes they will do a dividend discount model. This model discounts the dividends being returned by the utility. Institutional investors may also run a discounted cash flow model as well. Regardless of the model, the concept is the same. Dividends, earnings, and cash flow can all be manipulated by the company to reflect a good standing company, but ultimately, these all need to continue growing or the company’s management is ineffective.

Determining if a Utility is Undervalued

All this analysis converges to one question: is this utility a buy? Utilities are very interesting, because they don’t require a large risk factor for investors to jump on.

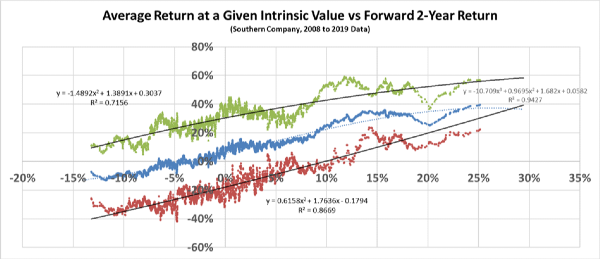

The graph above shows the average 2-year return (in blue) at a price point that is a percentage below intrinsic value. This graph is indifferent to a date. The green and red are 3-sigma distributions from the average. The larger the difference between red and green the more volatility at the point.

You can make some generalizations on what actions to take from this information:

Advanced Topics

The above section should help beginner investors take their stock analysis to the next level. These patterns in investing are the same for many different stocks. Stock’s that don’t hold this pattern are either highly speculative, poorly managed, or very growth focused. A stock that does not hold this pattern isn’t a bad stock, but they are not good for income focused or wealth preservation focused portfolios.

When to Use Margin

Margin is debt provided to you by the broker to buy investments. Using margin is very risky because you can lose more money than your initial investment. However, margin is a great way to amplify your returns, especially with utilities.

Warning: this is an advanced technique. Do not use margin until you are comfortable investing. We suggest only using margin sparingly. Overuse of margin may result in catastrophic loss during black swan events

Based on our analysis of Southern Company, the best time to use margin is when the price of Southern Company is 10% below its intrinsic value. Even better, if the stock is 20% below its intrinsic value, it may be good to have 5% to 10% of your investment be margin.

Margin has an interest rate you must pay. If this interest rate cannot be covered by your dividends, it may not be good to use margin, even if the stock is significantly undervalued. This is because a stock needs time to recover, and this recovery can take two years to occur.

Accumulation Phase

Looking at the graph again, you can see that roughly 5% to 10% below the intrinsic value is an accumulation phase. Here, you can buy stock using a dollar-cost averaging strategy. You can continue to keep your margin for previous stock you’ve bought but at this point it is not worth adding more margin.

De-Risking Phase

When the stock’s price is +/-5% of the intrinsic value, start de-risking your position. You can stop dollar-cost averaging and instead sell your stock positions for a profit if possible. Use these proceeds to clear your margin. This process alone should give you an easy 10% to 15% gain while still holding the stock without any more margin.

Utilizing Cover Calls and Limit Sells

The stock will stay in the +/-5% range for a while, so its best to let it be until it falls out of this range. As we’ll show in our theories section, this range is the most volatile price interval the stock can be in. If the price falls back into a value position, accumulate. If it starts to appreciate higher, then it’s overvalued by the market. When the stock is overvalued, use two advanced techniques to continue profiting even while you’re trying to sell your position. The first is to use a limit order. Place a limit order 5% to 10% below the current price. If the price increases, raise your limit order line accordingly.

Use covered calls to make money on the option fees while also giving yourself a synthetic limit order on the upside. The covered call will let us get out of our position if momentum gets too strong while still profiting from the fees.

Do not ever regret missing additional upside

Momentum is a real phenomenon and even utilities can be driven by momentum. Do not regret missing out on further momentum upward as you’ll be expending unnecessary stress trying to “time the market”. Get out knowing that you’re winning a lot more by investing consistently and patiently.

Warning: if the stock price falls and you have a covered call option and a limit order on your stocks. Be sure the covered call option is closed before the limit order is met. Do not sell a call option without the underlying asset as backup unless you’re an advanced options trader

Why We Don’t Care About Other Financial Values

This section is for the financial nerds out there. These topics aren’t for new investors, but feel free to read on if you’re curious

Why Dividends Don’t Matter When You’re Valuing a Utility Stock

We clearly saw in our analysis of the best electric utility companies that companies who push dividends as their main attraction to investors have more volatility, poor stock appreciation, and larger drawdowns. Dividends don’t matter in assessing a utility stock when you’re determining its valuation, or the price you want to buy the stock at.

Dividend policy and management strength matter significantly when deciding which utility to invest in. Even though a utility may be undervalued, that doesn’t mean it’s a good buy. Management malfunction can completely break down an analysis like this.

Getting back to dividends, the key reason why they don’t help in valuing the company is because they are artificially made by the board. If the dividend is 70% of earnings or higher (this is the dividend payout ratio) then the company is basically giving away all their earnings without thinking long term about continuously improving the business. This means the company is sacrificing earnings growth for dividends. Any company that does this for too long will see earnings fall, which will be catastrophic for the company’s stock price. Dividends are important to determine if a utility is right for you, but it shouldn’t be used to evaluate the company’s intrinsic value.

Cashflow

Cashflow is a great measure of a company’s value. Cashflow growth is a good indication of a well-managed company. Nonetheless, cashflow can obscure real company growth. One-time costs like fees can make cashflow look poor, while the truth is that earnings were solid. For a utility, earnings can give a better sense of the overall value of the company instead of cashflow.

Revenue

Revenue is the premier financial metric when looking at technology companies, start-ups, and high-growth companies. When revenue increases, it means the company is forging new markets or disrupting old ones. Price movement of technology stocks historically correlate better with revenue than earnings. In many cases, earnings may be zero or negative for years as the company burns through capital to disrupt their market.

However, for utilities, you can predict revenue growth by simply monitoring population growth. Utilities that operate in areas with a population growth will see an increase in demand. Regulated utilities have a monopoly in their area and so revenue directly correlates to population. And even if a utility can increase revenue, their profit margins are low. In Q3 2022, AEP’s profit margin was only 13.08%[2]. Utilities must fight the constant corrosion of energy costs to their bottom line. Hence significant revenue increase may be irrelevant if a management team cannot turn a profit on the revenue.

Red Flags

Our value analysis gives you a big advantage when assessing a stable, profitable, well managed company. But value investors measure multiple qualitative metrics like executive team quality and company culture. Why though? The answer is that poor company quality will lead to bad practices and poor culture which will undermine the stock’s consistency. Here are some red flags that can occur due to mismanagement.

Book Value per Share is Plummeting

The book value per share of a utility should steadily increase overtime. Small fluctuations downward are typically no more than random variability. But if a company writes off a poor investment or burns too much cash, you could see book value per share plummet.

In the graph above, the sharp drop in intrinsic value was due to a drop in book value per share. Inevitably, the price readjusted back down accordingly

Book value per share may drop for the falling reasons (this list is not exhaustive):

Earnings growth is negative

Earnings growth will fluctuate every quarter. However, years of negative earnings growth is a signal of a potential disaster. When a utility cannot turn around earnings growth, keep away from the utility until they can prove they can turn it around. A new executive team cannot immediately turn earnings growth around and for income investors its not wise to speculate on new executive teams.

Payout Ratio is Too High

A utility company that pays out a dividend higher than their earnings needs to be avoided until their dividend policy is adjusted. A utility is always looking for investors so that it can raise its stock price. That’s an inherent quality of companies. For utilities, the dividend alone can sometimes entice income investors and ETFs to buy into the utility. This may come at the expense of the long-term prospects of the company as too much money is allocated to dividends instead of the business’s continuous improvement.

Theories

Warning, we are deviating significantly from “beginners’ topics” in this section

Momentum and Value Investing Intertwined

A conjecture made from looking at the 2-year forward looking movements of stocks is that momentum and value investing are intertwined phenomena. When the price of a stock is significantly undervalued, momentum starts to accumulate as the price tries to get back to intrinsic value. Once intrinsic value is reached, momentum seems to consistently pull the price up significantly past the base intrinsic value. Inevitably, another pull back occurs again. This cycle of undervaluation, momentum up to overvaluation, and then a correction seems to happen in roughly 2-year intervals for utility stocks. Utility stocks in particular show this cycle possibly due to their low volatility of the underlying intrinsic value of the company.

The Money is in Volatility

When a stock is near its intrinsic value, it seems to be the most volatile. It seems that the market just doesn’t want it to stay at that price. The conjecture is that while the “efficient market” is satisfied with the price, this part of the market stops partaking in the price movement. What’s left are traders, market makers, and investors changing their position for non-efficient reasons. For example, an ETF will buy more shares of the utility to meet an arbitrary portfolio percentage. Or a retail investor will sell their shares to take a vacation. Traders and market makers are likely pushing the price of the stock away from the intrinsic value so that they themselves can make their own profit on the transaction.

This may be why the price of a stock is most volatile when its at or near the intrinsic value of the stock. All efficient participants are satisfied with the price and don’t partake in trading, leaving volume to be controlled by participants who need volatility for their own profit.

Conclusion

The discounted earnings model is the best way to value a utility stock. A utility’s unique business characteristics can give you an opportunity to evaluate the intrinsic value of the company with confidence. Nonetheless, be sure to run a qualitative analysis of the company as well. Be sure the executive team has a clear vision to grow the company and are building processes and cultures to meet that vision.

The Top Utility Stocks

Our community is writing new analysis every day to help you find undervalued investment opportunities. Check out these top lists to find new investment ideas:

The Top Utility Stocks to Buy Now

The Top Electric Company Stocks Ranked Best to Worst

The Top Water Company Stocks Ranked Best to Worst

The Top Dividend Stocks

References

1.) The Intelligent Investor, Mr. Market as summarized on Wikipedia

2.) AEP key statistics from Yahoo! Finance