Overview: The markets are putting the finishing touches on this week’s activity. Japan, returning from yesterday’s holiday bought equities, and its major indices jumped more than 2%. China, South Korea, and Australia struggled. Europe’s Stoxx 600 is firmer for the third consecutive session. It is up about 1.3% this week. US futures are also firmer after reversing earlier gains yesterday to close lower on the day. The US 10-year yield is flat near 2.88%, while European benchmarks are 4-6 bp higher. The greenback is mixed. The dollar-bloc currencies and Norwegian krone are slightly firmer, while the Swedish krona, sterling, and the yen are off around 0.3%-0.6%. Emerging market currencies are also mixed, though the freely accessible currencies are mostly firmer. The JP Morgan Emerging Market Currency Index is up about 1.15% this week, ahead of the Latam session, which if sustained would be the strongest performance in three months. Gold is consolidating at lower levels having been turned back from $1800 in the middle of the week. Near $1787.50, it is up less than 0.7% for the week. September WTI is edging higher for the third consecutive session, which would match the longest streak since January. US natgas surged 8.2% yesterday but has come back offered today. It is off 2.3%. Europe’s natgas benchmark is snapping a three-day advance of nearly 8% and is off 1.8% today. Iron ore rose 2.2% yesterday and it gave most of its back today, sliding almost 1.7%. September copper is unchanged after rallying more than 3.3% over the past two sessions. September wheat has a four-day rally in tow but is softer ahead of the Department of Agriculture report (World Agricultural Supply and Demand Estimates).

Asia Pacific

Japan and China will drop some market sensitive high-frequency economic data as trading begins in the new week. Japan will release its first estimate of Q2 GDP. The median in Bloomberg's survey and the average of a dozen Japanese think tanks (cited by Jiji Press) project around a 2.7% expansion of the world's third-largest economy, after a 0.5% contraction in Q1. Consumption and business investment likely improved. Some of the demand was probably filled through inventories. They added 0.5% to Q1 growth but may have trimmed Q2 growth. Net exports were a drag on Q1 (-04%) and may be flat. The GDP deflator was -0.5% in Q1 and may have deteriorated further in Q2. Some observers see the cabinet reshuffle that was announced this week strengthening the commitment to ease monetary policy. The deflation in the deflator shows what Governor Kuroda's successor next April must address as well.

China reports July consumption (retail sales), industrial output, employment (surveyed jobless rate), and investment (fixed assets and property). The expected takeaway is that the world's second-largest economy is recovering but slowly. Industrial output and retail sales are expected to have edged up. Of note, the year-to-date retail sales compared with a year ago was negative each month in Q2 but is expected to have turned positive in July. The year-over-year pace of industrial production is expected to rise toward 4.5%, which would be the best since January. The housing market, which acted as a critical engine of growth is in reverse. New home prices (newly build commercial residential building prices in 70 cities) have been falling on a year-over-year basis starting last September, and likely continued to do so in July. Property investment (completed investment in real estate) likely fell for the fourth consecutive month. It has slowed every month beginning March 2021. The pace may have accelerated to -5.6% year-over-year after a 5.4% slide in the 12-months through June. The surveyed unemployed rate was at 4.9% last September and October. It rose to 6.1% in April and has slipped back to 5.5% in June. The median forecast in Bloomberg's survey expects it to have remained there in July. Lastly, there are no fixed dates for the lending figures and the announcement of the one-year medium-term lending facility rate. Lending is expected to have slowed sharply from the surge in June, while the MLF rate is expected to be steady at 2.85%.

Over the several weeks, foreign investors have bought a record amount of Japanese bonds. Over the past six weeks, foreigners snapped up JPY6.44 trillion (~$48 bln). It may partly reflect short-covering after the run-in with the Bank of Japan who bought a record amount to defend the yield-curve control cap of 0.25% on the 10-year bond. There is another consideration. For dollar-based investors, hedging the currency risk, which one is paid to do, a return of more than 4% can be secured. At the same time, for yen-based investors, hedging the currency risk is expensive, which encourages the institutional investors to return to the domestic market. Japanese investors have mostly been selling foreign bonds this year. However, the latest Ministry of Finance data shows that they were net buyers for the third consecutive week, matching the longest streak of the year. Still, the size is small. suggesting it may not be a broad or large force yet.

Although the US 10-year yield jumped 10 bp yesterday, extending its recovery from Monday's low near 2.75% for a third session, the dollar barely recovered against the yen. After falling 1.6% on Wednesday, after the softer than expected US CPI, the greenback rose 0.1% yesterday and is edging a little higher today. Partly what has happened is that the exchange rate correlation with the 10-year yield has slackened while the correlation with the two-year has increased. In fact, the correlation of the change in the two-year and the exchange rate is a little over 0.60 and is the highest since March. The dollar appears to be trading comfortably now between two large set of options that expire today. One set is at JPY132 for $860 mln and the other at JPY134 for $1.3 bln. Around $0.7120, the Australian dollar is up about 3% this week and is near two-month highs. It reached almost $0.7140 yesterday. The next technical target is in the $0.7150-$0.7170 area. Support is seen ahead of $0.7050. Next week's data highlight is the employment data (August 18). The greenback traded in a CNY6.7235-CNY6.7600 on Wednesday and remained in that range yesterday and today. For the second consecutive week, the dollar has alternated daily between up and down sessions for a net change of a little more than 0.1%. The PBOC set the dollar's reference rate at CNY6.7413, tight to expectations (Bloomberg's survey) of CNY6.7415.

Europe

The UK's economy shrank by 0.6% in June, ensuring a contraction in Q2. The 0.1% shrinkage was a bit smaller than expected but the weakness was widespread. Consumption fell by 0.2% in the quarter, worse than expected, while government spending collapsed by 2.9% after a 1.3% pullback in Q1. A decline in Covid testing and slower retail sales were notable drags. The one bright spot was business investment was stronger than expected. The June data itself was miserable, though there was an extra holiday (Queen's jubilee). All three sectors, industrial output, services, and construction, all fell in June and the trade balance deteriorated. The market's expectation for next month's BOE meeting was unaffected by the data. The swaps market has about an 85% chance of another 50 bp hike discounted.

Industrial output in the eurozone rose by 0.7%, well above the 0.2% median forecast in Bloomberg's survey and follows a 2.1% increase in May. The manufacturing PMI warned that an outright contraction is possible. Of the big four members, only Italy disappointed. The median forecast in Bloomberg's survey anticipated a decline in German, France, and Spain. Instead, they reported gains of 0.4%, 1.4%, and 1.1% respectively. Industrial output was expected to have contracted by 0.1% in Italy and instead it reported a 2.1% drop. In aggregate, the strength of capital goods (2.6% month-over-month) and energy (0.6%) more than offset the declines in consumer goods and intermediate goods. The year-over-year rise of 2.4% is the strongest since last September.

The disruption caused by Russia's invasion of Ukraine and the uneven Covid outbreaks and responses are as Rumsfeld might have said known unknowns. But the disruptive force that may not be fully appreciated is about to get worse. The German Federal Waterways and Shipping Administration is warning that water in the Rhine River will fall below a critical threshold this weekend. At an important waypoint, the level may fall to about 13 inches (33 centimeters). Less than around 16 inches (40 centimeters) and barges cannot navigate. An estimated 400k barrels a day of oil products are sent from the Amsterdam-Rotterdam-Antwerp region to Germany and Switzerland. The International Energy Agency warns that the effects could last until late this year, and hits landlocked countries who rely on the Rhine the hardest. Bloomberg reported that Barge rates from Rotterdam to Basel have risen to around 267 euros a ton, a ten-fold increase in a few months.

The strong surge in the euro to almost $1.0370 on Wednesday has stalled. The euro is consolidating inside yesterday's relatively narrow range (~ $1.0275-$1.0365). The momentum traders may be frustrated by the lack of follow-through. We suspect a break of $1.0265 would push more to the sidelines. The downtrend line from the February, March, and June highs comes in slightly above $1.0385 today. The broad dollar selloff in response to the July CPI saw sterling reach above $1.2275, shy of the month's high closer to $1.2295. Similar to the euro, sterling stalled. It has slipped through yesterday's low (~$1.2180). A break of the $1.2140 area could see $1.2100. That said, the $1.20 area could be the neckline of a double top and a convincing break would signal the risk of a return to the lows set a month ago near $1.1760.

America

Think about the recent big US economic news. It began last Friday with a strong employment report, more than twice what economists expected (median, Bloomberg survey) and a new cyclical low in unemployment. The job gains were broadly distributed. That was followed by a softer than expected CPI and PPI. Some observers placed emphasis on the slump in productivity and jump in unit labor costs. Those are derived from GDP figures and are not measured separately, though they are important economic concepts. Typically, when GDP is contracting, productivity contracts and by definition, unit labor costs rise. In effect, the market for goods and services adjusts quicker the labor market, and the market for money, even quicker. If the economy expands as the Atlanta Fed GDPNow tracker or the median in Bloomberg's survey project (2.5% and 2.0%, respectively), productivity will improve, and unit labor costs will fall.

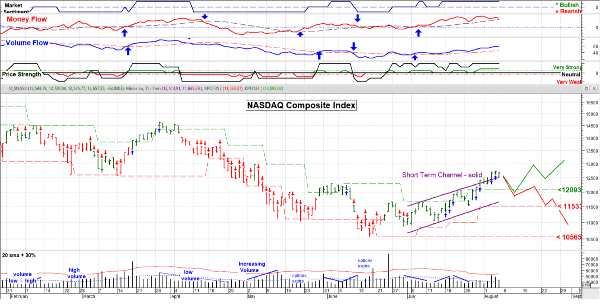

Barring a precipitous fall today, the S&P 500 and NASDAQ will advance for the fourth consecutive week. The 10-year yield fell by almost 45 bp on the last three week of July and has recovered around half here in August. That includes five basis points this week despite the softer inflation readings. The two-year note yield fell almost 25 bp in the last two weeks of July and jumped 34 bp last week. It is virtually flat this week around 3.22%. The odds of a 75 bp rate hike at next month's FOMC meeting fell from about 75% to about 47%. The year-end rate expectation fell to 3.52% from 3.56%. Some pundits claim the market is pricing in a March 2023 cut, but the implied yield of the March 2023 Fed funds futures contract is 18 bp above the December 2022 contract. It matches the most since the end of June. Still, while the Federal Reserve is trying to tighten financial conditions the market is pushing back. The Bloomberg Financial Conditions Index is at least tight reading since late April. The Goldman Sachs Financial Condition index is the least tight in nearly two months.

US import and export prices are the stuff that captures the market's imagination. However, the preliminary University of Michigan's consumer survey, and especially the inflation expectations can move the markets, especially given that Fed Chair Powell cited it as a factor encouraging the 75 bp hike in June. The Bloomberg survey shows the median expectation is for a tick lower in inflation expectations, with the one-year slipping to 5.1% from 5.2%. The 5-10-year expectation is seen easing to 2.8% from 2.9%. If accurate, it would match the lowest since April 2021. The two-year breakeven (difference between the conventional yield and the inflation-protected security) peaked in March near 5% and this week reached 2.70%, its lowest since last October. It is near 2.80% now.

Mexico delivered the widely anticipated 75 bp hike yesterday. The overnight rate target is now 8.50%. The decision was unanimous. It is the 10th consecutive hike and concerns that AMLO's appointments would be doves has proven groundless. The central bank meets again on September 29. Like other central banks, it did not pre-commit to the size of the next move, preserving some tactical flexibility. If the Fed hikes by 75 bp, it will likely match it. Peru's central bank hiked its reference rate by 50 bp, the 10th consecutive hike of that magnitude after starting the cycle last August with a 25 bp move. It is not done. Lima inflation was near 8.75% last month and the reference rate is at 6.50%. The Peruvian sol is up about 1.2% this month, coming into today. It has appreciated by around 3.25% year-to-date, making it the second-best performer in the region after Brazil's 8.1% rise. Argentina hiked its benchmark Leliq rate by 950 bp yesterday to 69.5%. It had delivered an 800 bp hike two weeks again. Argentina's inflation reached 71% last month. The Argentine peso is off nearly 23.5% so far this year, second only to the Turkish lira (~-26%).

The US dollar fell slightly below CAD1.2730 yesterday, its lowest level since mid-June. The slippage in the S&P 500 and NASDAQ helped it recover to around CAD1.2775. It has not risen above that today, encouraged perhaps by the firmer US futures. Although the 200-day moving average (~CAD1.2745) is a good mile marker, the next important chart is CAD1.2700-CAD1.2720. A convincing break would target CAD1.2650 initially and then CAD1.2600. While the Canadian dollar has gained almost 1.4% against the US dollar this week (around CAD1.2755), the Mexican peso is up nearly 2.4%. The greenback is pressing against support in the MXN19.90 area. A break targets the late June lows near MXN19.82. The MXN20.00 area provides the nearby cap.

Overview: The markets are putting the finishing touches on this week’s activity. Japan, returning from yesterday’s holiday bought equities, and its major indices jumped more than 2%. China, South Korea, and Australia struggled. Europe’s Stoxx 600 is firmer for the third consecutive session. It is up about 1.3% this week. US futures are also firmer after reversing earlier gains yesterday to close lower on the day. The US 10-year yield is flat near 2.88%, while European benchmarks are 4-6 bp higher. The greenback is mixed. The dollar-bloc currencies and Norwegian krone are slightly firmer, while the Swedish krona, sterling, and the yen are off around 0.3%-0.6%. Emerging market currencies are also mixed, though the freely accessible currencies are mostly firmer. The JP Morgan Emerging Market Currency Index is up about 1.15% this week, ahead of the Latam session, which if sustained would be the strongest performance in three months. Gold is consolidating at lower levels having been turned back from $1800 in the middle of the week. Near $1787.50, it is up less than 0.7% for the week. September WTI is edging higher for the third consecutive session, which would match the longest streak since January. US natgas surged 8.2% yesterday but has come back offered today. It is off 2.3%. Europe’s natgas benchmark is snapping a three-day advance of nearly 8% and is off 1.8% today. Iron ore rose 2.2% yesterday and it gave most of its back today, sliding almost 1.7%. September copper is unchanged after rallying more than 3.3% over the past two sessions. September wheat has a four-day rally in tow but is softer ahead of the Department of Agriculture report (World Agricultural Supply and Demand Estimates).

Asia Pacific

Japan and China will drop some market sensitive high-frequency economic data as trading begins in the new week. Japan will release its first estimate of Q2 GDP. The median in Bloomberg's survey and the average of a dozen Japanese think tanks (cited by Jiji Press) project around a 2.7% expansion of the world's third-largest economy, after a 0.5% contraction in Q1. Consumption and business investment likely improved. Some of the demand was probably filled through inventories. They added 0.5% to Q1 growth but may have trimmed Q2 growth. Net exports were a drag on Q1 (-04%) and may be flat. The GDP deflator was -0.5% in Q1 and may have deteriorated further in Q2. Some observers see the cabinet reshuffle that was announced this week strengthening the commitment to ease monetary policy. The deflation in the deflator shows what Governor Kuroda's successor next April must address as well.

China reports July consumption (retail sales), industrial output, employment (surveyed jobless rate), and investment (fixed assets and property). The expected takeaway is that the world's second-largest economy is recovering but slowly. Industrial output and retail sales are expected to have edged up. Of note, the year-to-date retail sales compared with a year ago was negative each month in Q2 but is expected to have turned positive in July. The year-over-year pace of industrial production is expected to rise toward 4.5%, which would be the best since January. The housing market, which acted as a critical engine of growth is in reverse. New home prices (newly build commercial residential building prices in 70 cities) have been falling on a year-over-year basis starting last September, and likely continued to do so in July. Property investment (completed investment in real estate) likely fell for the fourth consecutive month. It has slowed every month beginning March 2021. The pace may have accelerated to -5.6% year-over-year after a 5.4% slide in the 12-months through June. The surveyed unemployed rate was at 4.9% last September and October. It rose to 6.1% in April and has slipped back to 5.5% in June. The median forecast in Bloomberg's survey expects it to have remained there in July. Lastly, there are no fixed dates for the lending figures and the announcement of the one-year medium-term lending facility rate. Lending is expected to have slowed sharply from the surge in June, while the MLF rate is expected to be steady at 2.85%.

Over the several weeks, foreign investors have bought a record amount of Japanese bonds. Over the past six weeks, foreigners snapped up JPY6.44 trillion (~$48 bln). It may partly reflect short-covering after the run-in with the Bank of Japan who bought a record amount to defend the yield-curve control cap of 0.25% on the 10-year bond. There is another consideration. For dollar-based investors, hedging the currency risk, which one is paid to do, a return of more than 4% can be secured. At the same time, for yen-based investors, hedging the currency risk is expensive, which encourages the institutional investors to return to the domestic market. Japanese investors have mostly been selling foreign bonds this year. However, the latest Ministry of Finance data shows that they were net buyers for the third consecutive week, matching the longest streak of the year. Still, the size is small. suggesting it may not be a broad or large force yet.

Although the US 10-year yield jumped 10 bp yesterday, extending its recovery from Monday's low near 2.75% for a third session, the dollar barely recovered against the yen. After falling 1.6% on Wednesday, after the softer than expected US CPI, the greenback rose 0.1% yesterday and is edging a little higher today. Partly what has happened is that the exchange rate correlation with the 10-year yield has slackened while the correlation with the two-year has increased. In fact, the correlation of the change in the two-year and the exchange rate is a little over 0.60 and is the highest since March. The dollar appears to be trading comfortably now between two large set of options that expire today. One set is at JPY132 for $860 mln and the other at JPY134 for $1.3 bln. Around $0.7120, the Australian dollar is up about 3% this week and is near two-month highs. It reached almost $0.7140 yesterday. The next technical target is in the $0.7150-$0.7170 area. Support is seen ahead of $0.7050. Next week's data highlight is the employment data (August 18). The greenback traded in a CNY6.7235-CNY6.7600 on Wednesday and remained in that range yesterday and today. For the second consecutive week, the dollar has alternated daily between up and down sessions for a net change of a little more than 0.1%. The PBOC set the dollar's reference rate at CNY6.7413, tight to expectations (Bloomberg's survey) of CNY6.7415.

Europe

The UK's economy shrank by 0.6% in June, ensuring a contraction in Q2. The 0.1% shrinkage was a bit smaller than expected but the weakness was widespread. Consumption fell by 0.2% in the quarter, worse than expected, while government spending collapsed by 2.9% after a 1.3% pullback in Q1. A decline in Covid testing and slower retail sales were notable drags. The one bright spot was business investment was stronger than expected. The June data itself was miserable, though there was an extra holiday (Queen's jubilee). All three sectors, industrial output, services, and construction, all fell in June and the trade balance deteriorated. The market's expectation for next month's BOE meeting was unaffected by the data. The swaps market has about an 85% chance of another 50 bp hike discounted.

Industrial output in the eurozone rose by 0.7%, well above the 0.2% median forecast in Bloomberg's survey and follows a 2.1% increase in May. The manufacturing PMI warned that an outright contraction is possible. Of the big four members, only Italy disappointed. The median forecast in Bloomberg's survey anticipated a decline in German, France, and Spain. Instead, they reported gains of 0.4%, 1.4%, and 1.1% respectively. Industrial output was expected to have contracted by 0.1% in Italy and instead it reported a 2.1% drop. In aggregate, the strength of capital goods (2.6% month-over-month) and energy (0.6%) more than offset the declines in consumer goods and intermediate goods. The year-over-year rise of 2.4% is the strongest since last September.

The disruption caused by Russia's invasion of Ukraine and the uneven Covid outbreaks and responses are as Rumsfeld might have said known unknowns. But the disruptive force that may not be fully appreciated is about to get worse. The German Federal Waterways and Shipping Administration is warning that water in the Rhine River will fall below a critical threshold this weekend. At an important waypoint, the level may fall to about 13 inches (33 centimeters). Less than around 16 inches (40 centimeters) and barges cannot navigate. An estimated 400k barrels a day of oil products are sent from the Amsterdam-Rotterdam-Antwerp region to Germany and Switzerland. The International Energy Agency warns that the effects could last until late this year, and hits landlocked countries who rely on the Rhine the hardest. Bloomberg reported that Barge rates from Rotterdam to Basel have risen to around 267 euros a ton, a ten-fold increase in a few months.

The strong surge in the euro to almost $1.0370 on Wednesday has stalled. The euro is consolidating inside yesterday's relatively narrow range (~ $1.0275-$1.0365). The momentum traders may be frustrated by the lack of follow-through. We suspect a break of $1.0265 would push more to the sidelines. The downtrend line from the February, March, and June highs comes in slightly above $1.0385 today. The broad dollar selloff in response to the July CPI saw sterling reach above $1.2275, shy of the month's high closer to $1.2295. Similar to the euro, sterling stalled. It has slipped through yesterday's low (~$1.2180). A break of the $1.2140 area could see $1.2100. That said, the $1.20 area could be the neckline of a double top and a convincing break would signal the risk of a return to the lows set a month ago near $1.1760.

America

Think about the recent big US economic news. It began last Friday with a strong employment report, more than twice what economists expected (median, Bloomberg survey) and a new cyclical low in unemployment. The job gains were broadly distributed. That was followed by a softer than expected CPI and PPI. Some observers placed emphasis on the slump in productivity and jump in unit labor costs. Those are derived from GDP figures and are not measured separately, though they are important economic concepts. Typically, when GDP is contracting, productivity contracts and by definition, unit labor costs rise. In effect, the market for goods and services adjusts quicker the labor market, and the market for money, even quicker. If the economy expands as the Atlanta Fed GDPNow tracker or the median in Bloomberg's survey project (2.5% and 2.0%, respectively), productivity will improve, and unit labor costs will fall.

Barring a precipitous fall today, the S&P 500 and NASDAQ will advance for the fourth consecutive week. The 10-year yield fell by almost 45 bp on the last three week of July and has recovered around half here in August. That includes five basis points this week despite the softer inflation readings. The two-year note yield fell almost 25 bp in the last two weeks of July and jumped 34 bp last week. It is virtually flat this week around 3.22%. The odds of a 75 bp rate hike at next month's FOMC meeting fell from about 75% to about 47%. The year-end rate expectation fell to 3.52% from 3.56%. Some pundits claim the market is pricing in a March 2023 cut, but the implied yield of the March 2023 Fed funds futures contract is 18 bp above the December 2022 contract. It matches the most since the end of June. Still, while the Federal Reserve is trying to tighten financial conditions the market is pushing back. The Bloomberg Financial Conditions Index is at least tight reading since late April. The Goldman Sachs Financial Condition index is the least tight in nearly two months.

US import and export prices are the stuff that captures the market's imagination. However, the preliminary University of Michigan's consumer survey, and especially the inflation expectations can move the markets, especially given that Fed Chair Powell cited it as a factor encouraging the 75 bp hike in June. The Bloomberg survey shows the median expectation is for a tick lower in inflation expectations, with the one-year slipping to 5.1% from 5.2%. The 5-10-year expectation is seen easing to 2.8% from 2.9%. If accurate, it would match the lowest since April 2021. The two-year breakeven (difference between the conventional yield and the inflation-protected security) peaked in March near 5% and this week reached 2.70%, its lowest since last October. It is near 2.80% now.

Mexico delivered the widely anticipated 75 bp hike yesterday. The overnight rate target is now 8.50%. The decision was unanimous. It is the 10th consecutive hike and concerns that AMLO's appointments would be doves has proven groundless. The central bank meets again on September 29. Like other central banks, it did not pre-commit to the size of the next move, preserving some tactical flexibility. If the Fed hikes by 75 bp, it will likely match it. Peru's central bank hiked its reference rate by 50 bp, the 10th consecutive hike of that magnitude after starting the cycle last August with a 25 bp move. It is not done. Lima inflation was near 8.75% last month and the reference rate is at 6.50%. The Peruvian sol is up about 1.2% this month, coming into today. It has appreciated by around 3.25% year-to-date, making it the second-best performer in the region after Brazil's 8.1% rise. Argentina hiked its benchmark Leliq rate by 950 bp yesterday to 69.5%. It had delivered an 800 bp hike two weeks again. Argentina's inflation reached 71% last month. The Argentine peso is off nearly 23.5% so far this year, second only to the Turkish lira (~-26%).

The US dollar fell slightly below CAD1.2730 yesterday, its lowest level since mid-June. The slippage in the S&P 500 and NASDAQ helped it recover to around CAD1.2775. It has not risen above that today, encouraged perhaps by the firmer US futures. Although the 200-day moving average (~CAD1.2745) is a good mile marker, the next important chart is CAD1.2700-CAD1.2720. A convincing break would target CAD1.2650 initially and then CAD1.2600. While the Canadian dollar has gained almost 1.4% against the US dollar this week (around CAD1.2755), the Mexican peso is up nearly 2.4%. The greenback is pressing against support in the MXN19.90 area. A break targets the late June lows near MXN19.82. The MXN20.00 area provides the nearby cap.

Originally Posted on Marctomarket.com