As markets show the first signs of potential recovery, Uber Technologies (NYSE: UBER) continues to stand out as a compelling investment opportunity. Despite recent short-term declines, investor sentiment and long-term growth projections suggest this could be the perfect time to buy into the mobility giant. Let’s dive into Uber’s performance, valuation, and reasons why it deserves a place in your portfolio.

Market Conditions and Uber’s Recent Performance

Over the last week, nearly every industry has experienced declines, with Uber following the trend—down over 6%, including a 3% drop just yesterday. Year to date, however, Uber is up an impressive 177%, outperforming the S&P with a 169% gain over the last five years. These numbers demonstrate the company’s resilience and ability to thrive despite challenging market conditions.

Investor sentiment, as measured by the Fear & Greed Index, currently sits at an extreme low of 17 points, underscoring market pessimism. However, such times often present the greatest opportunities for disciplined investors willing to take a long-term view.

Institutional Confidence in Uber

Institutional investors continue to show confidence in Uber. Over the past year, institutions sold $13 billion worth of shares but purchased nearly double that amount—$19 billion. In the most recent quarter (Q4 2024), institutional buying outpaced selling, reflecting strong sentiment among big players.

Notably, prominent investor Bill Ackman has expressed confidence in Uber, acquiring over 30 million shares at the beginning of the year. Ackman describes Uber as "one of the best-managed and highest-quality businesses in the world," emphasizing its undervaluation relative to intrinsic worth. This level of institutional and super-investor interest further strengthens Uber’s investment case.

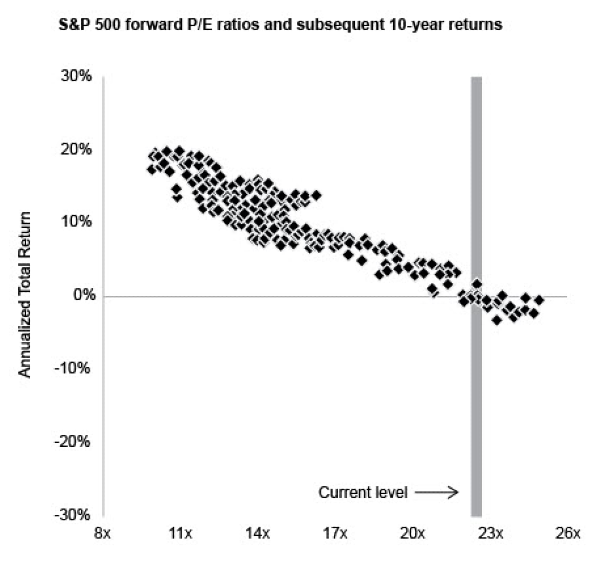

Valuation: A Premium Worth Paying

Uber currently trades with a forward price-to-earnings (P/E) ratio of 22, which is a 23% premium compared to the sector average of 18. However, this premium is justified by Uber’s high-quality metrics and strong growth potential. While metrics such as price-to-book, price-to-sales, and price-to-cash-flow show Uber trading at higher-than-average valuations, its market leadership and revenue growth validate the premium.

Diverse Revenue Streams and Strong Margins

Uber’s revenue streams are robust and diverse:

- Mobility: Uber’s flagship ride-hailing segment has grown 25% year-over-year.

- Uber Eats: This segment now accounts for approximately half of total revenue, growing 21% year-over-year.

- Total Revenue: Up 20% to $12 billion, with a gross margin of 40%, highlighting operational efficiency.

Free cash flow turned positive in Q2 2022 and has shown consistent improvement since, signaling Uber’s transition into a more mature and financially sustainable phase.

Growth Strategy: Maximizing Consumer Engagement

Uber’s business model revolves around increasing consumer engagement and spending. The company has successfully grown its base of multi-product users—those utilizing more than one service—up from 21% in 2021 to 34% today. Multi-product users spend over three times more than single-product users, a trend that bodes well for future revenue growth.

Additionally, Uber continues to expand its presence in new markets, including Argentina and Italy, while finding room to grow even in mature markets like Spain and Japan.

Long-Term Outlook and Market Leadership

Uber’s three-year outlook includes:

- Mid-to-high teens growth in gross bookings.

- EBITDA growth in the high 30% to 40% range.

- Free cash flow as a percentage of adjusted EBITDA reaching 90%.

As a global player operating in over 70 countries, Uber remains the category leader in all top 10 countries by gross bookings. This market leadership, coupled with expanding services like grocery and parcel delivery, positions Uber for continued success.

Conclusion

While short-term fluctuations may present challenges, Uber Technologies offers a unique combination of market leadership, diverse revenue streams, and strong growth potential. Institutional confidence and consistent performance make Uber a stock to watch in 2025 and beyond.

Investors should conduct their own due diligence but, with its current valuation and growth trajectory, Uber looks like a strong candidate for long-term portfolios.

https://youtu.be/cs02ydmPnss?si=oxOqidJzq6S5WSXk

As markets show the first signs of potential recovery, Uber Technologies (NYSE: UBER) continues to stand out as a compelling investment opportunity. Despite recent short-term declines, investor sentiment and long-term growth projections suggest this could be the perfect time to buy into the mobility giant. Let’s dive into Uber’s performance, valuation, and reasons why it deserves a place in your portfolio.

Market Conditions and Uber’s Recent Performance

Over the last week, nearly every industry has experienced declines, with Uber following the trend—down over 6%, including a 3% drop just yesterday. Year to date, however, Uber is up an impressive 177%, outperforming the S&P with a 169% gain over the last five years. These numbers demonstrate the company’s resilience and ability to thrive despite challenging market conditions.

Investor sentiment, as measured by the Fear & Greed Index, currently sits at an extreme low of 17 points, underscoring market pessimism. However, such times often present the greatest opportunities for disciplined investors willing to take a long-term view.

Institutional Confidence in Uber

Institutional investors continue to show confidence in Uber. Over the past year, institutions sold $13 billion worth of shares but purchased nearly double that amount—$19 billion. In the most recent quarter (Q4 2024), institutional buying outpaced selling, reflecting strong sentiment among big players.

Notably, prominent investor Bill Ackman has expressed confidence in Uber, acquiring over 30 million shares at the beginning of the year. Ackman describes Uber as "one of the best-managed and highest-quality businesses in the world," emphasizing its undervaluation relative to intrinsic worth. This level of institutional and super-investor interest further strengthens Uber’s investment case.

Valuation: A Premium Worth Paying

Uber currently trades with a forward price-to-earnings (P/E) ratio of 22, which is a 23% premium compared to the sector average of 18. However, this premium is justified by Uber’s high-quality metrics and strong growth potential. While metrics such as price-to-book, price-to-sales, and price-to-cash-flow show Uber trading at higher-than-average valuations, its market leadership and revenue growth validate the premium.

Diverse Revenue Streams and Strong Margins

Uber’s revenue streams are robust and diverse:

Free cash flow turned positive in Q2 2022 and has shown consistent improvement since, signaling Uber’s transition into a more mature and financially sustainable phase.

Growth Strategy: Maximizing Consumer Engagement

Uber’s business model revolves around increasing consumer engagement and spending. The company has successfully grown its base of multi-product users—those utilizing more than one service—up from 21% in 2021 to 34% today. Multi-product users spend over three times more than single-product users, a trend that bodes well for future revenue growth.

Additionally, Uber continues to expand its presence in new markets, including Argentina and Italy, while finding room to grow even in mature markets like Spain and Japan.

Long-Term Outlook and Market Leadership

Uber’s three-year outlook includes:

As a global player operating in over 70 countries, Uber remains the category leader in all top 10 countries by gross bookings. This market leadership, coupled with expanding services like grocery and parcel delivery, positions Uber for continued success.

Conclusion

While short-term fluctuations may present challenges, Uber Technologies offers a unique combination of market leadership, diverse revenue streams, and strong growth potential. Institutional confidence and consistent performance make Uber a stock to watch in 2025 and beyond.

Investors should conduct their own due diligence but, with its current valuation and growth trajectory, Uber looks like a strong candidate for long-term portfolios.

https://youtu.be/cs02ydmPnss?si=oxOqidJzq6S5WSXk