Understanding the Materials Sector

The materials sector encompasses a diverse set of industries involved in the discovery, development, and processing of raw materials. The materials sector is closely tied to the economic cycle. It tends to rise and fall with overall economic growth. Historically, the material sector performs well in the early stages of new economic growth.

There are many sub-segments in the industrial sector. The main material sub-sectors

Chemical Producers - These companies manufacture fertilizers, industrial chemicals, and other chemical products.

Metals Producers - Includes gold and copper miners, steelmakers, and other metal refining businesses.

Construction Materials - Makers of cement, bricks, glass, gravel, and other construction-related materials.

Wood-Based Goods - Producers of lumber, paper packaging, and related products.

Importance in the Economy

The material sector plays a crucial role in the economy. The material sector is the starting point in the economy’s supply chain. All sectors build goods and services that start with materials produced from the materials sector.

Material companies work at discovering, developing, and processing raw materials—such as metals, minerals, timber, and oil. These materials serve as essential building blocks for various industries, including manufacturing, construction, and energy production. Manufacturing relies heavily on raw materials and is a key driver of economic growth.

The material sector affects more the manufacturing. Construction, farming and technology all start their value-add processes with materials from the material sector. Construction needs wood and iron, farming needs nitrogen, and technology needs silicon.

Current State of the Material Sector

Historically, it performs well during early stages of economic recovery. In 2023, the sector delivered positive but sluggish returns due to recession concerns.

Copper mining is a materials Segment to Watch. There is favorable supply-and-demand which is making Copper Miners attractive for long-term investment. Also, the chemical manufacturing segment is holding strong in 2024.

As for Building Materials, the construction industry is testing new materials driven by decarbonization efforts and changing consumer preferences.

In terms of the Investment Landscape, over 2560 startups globally in the building materials industry. The average investment value per funding round was $50 million.

Material Sector Trends

- Sustainable Materials: Governments are implementing environmental regulations due to substantial waste generated during material use and production. Companies are focusing on sustainable alternatives.

- Responsive & Smart Materials: Innovations in materials that adapt to external stimuli, such as changes in temperature or light, are gaining traction. These smart materials have applications in various industries.

- Nanotechnology: Continued advancements in nanomaterials are enabling breakthroughs in fields like medicine, electronics, and energy storage.

- Additive Manufacturing (3D Printing): The adoption of 3D printing is growing, allowing customized and efficient production of complex parts.

- Lightweighting: Industries are seeking lightweight materials to improve fuel efficiency, reduce emissions, and enhance performance.

- Material Informatics: Data-driven approaches are being used to optimize material properties and accelerate research and development.

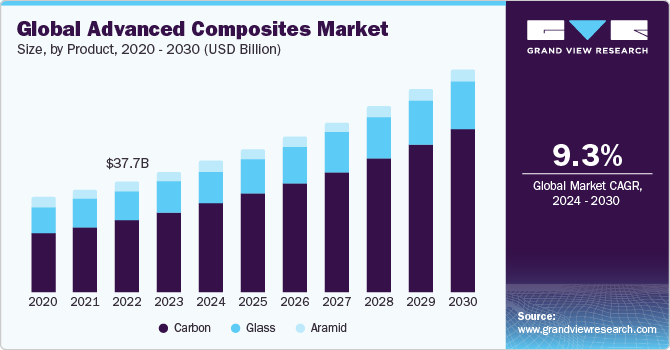

- Advanced Composites: Composite materials with superior properties (e.g., strength, durability) are being developed for aerospace, automotive, and construction applications.

- Graphene & 2D Materials: Graphene and other two-dimensional materials are being explored for their exceptional electrical, mechanical, and thermal properties.

lithium Prices Expected to Rise

However, Lithium prices have experienced a decline in 2024 even though forecasts predict price increases. There are some key factors influencing the market.

The surplus of raw materials for electric vehicle (EV) battery manufacturers has led to low prices. Lithium miners and producers continue to expand capacity, contributing to expectations of oversupply. On the supply side, government subsidies for firms across the EV supply chain have caused battery gluts, further impacting prices.

Geopolitically, trade barriers are also distorting the market. The EU imposed tariffs on Chinese EV producers, and the US quadrupled duties on Chinese EVs, affecting input materials for battery production.

Goldman Sachs estimates lithium carbonate prices at $13,377 per tonne and lithium hydroxide at $14,263 per tonne in 2024. S&P Global projects stabilization near current levels, ranging between $20,000 per metric tonne and $25,000 per metric tonne from 2024 to 2027.

Agricultural Chemical Prices are Trending

2024 Agricultural Chemical Price Transparency Report examined over 2,400 unique pricing data points across 33 states, covering more than 120 insecticides, fungicides, herbicides, and adjuvants. Additionally, the Producer Price Index for pesticide and other agricultural chemical manufacturing in July 2024 indicates trends in the industry.

Material Sector Forecasts

The materials sector, which includes industries like chemical producers, metals producers, construction materials, and wood-based goods, tends to move in sync with the broader economy. In 2023, it delivered positive but sluggish returns due to concerns over recession risk.

As the economy evolves, materials stocks could benefit from an eventual economic brightening in 2024. Historically, this sector performs well in the early stages of new economic growth. Favorable supply-demand dynamics may exist in some areas of the sector. For instance, copper miners and US chemical manufacturers show promising potential.

Manufacturers are increasingly adopting smart factory solutions, which could drive competitiveness and productivity in the materials industry.

Finally,The US construction market is expected to grow, supported by investments in infrastructure projects.

With all these variables in mind, Goldman Sachs predicts that the materials sector will outperform the broader market in the next 12 months. Their analysis considers factors like commodity prices, supply chain disruptions, and global demand.

Morgan Stanley’s research suggests that industrial metals (such as copper and aluminum) will experience strong demand due to infrastructure spending and green energy initiatives. They anticipate a positive outlook for materials companies.

Investing in Basic Materials Stocks

Investing in the material sectors have some differences from other sectors new investors should be aware of. The material sector is cyclical and tends to perform well during economic expansions, so be prepared for fluctuations. For example, this is different from the utility sector which will tend to not rise and fall with the general economy.

As we’ve noted early in the article, basic materials include chemicals, metals, construction materials, and wood-based goods. Be sure to research companies within these segments and understand that even these sub-segments react differently to market conditions. Finally, Look for favorable supply-demand dynamics. For instance, copper and certain chemicals may have strong demand. The material stock sector is influenced by the materials commodities market, which can be more volatile than material stocks.

The Pros of Investing in Basic Material Stocks

The material sector encompasses companies involved in mining, manufacturing, and processing raw materials. Investing in material stocks can be advantageous for the following reasons:

Resilience: Material stocks tend to perform well during economic cycles. Demand for core materials remains steady, even during downturns, as they underpin various industries.

Cyclical Upside: During economic expansions, material stocks benefit from increased demand. As economies grow, there’s greater need for construction materials, metals, chemicals, and other basic inputs.

Income Potential: Some material companies offer attractive dividends. Their consistent demand and stable cash flows allow them to distribute dividends, making them appealing for income-seeking investors.

Inflation Hedge: Material prices often rise during inflationary periods. Investing in material stocks can act as a hedge against inflation, preserving purchasing power.

Global Infrastructure Spending: As countries invest in infrastructure projects (roads, bridges, utilities), material stocks stand to gain. These projects require substantial raw materials.

Technological Advancements: Innovations in materials science drive demand for specialized materials (e.g., rare earth elements, advanced alloys). Companies at the forefront of such innovations can deliver strong returns.

Exposure to global economy and growth prospects

Material stocks stand to benefit significantly from global infrastructure spending. Here’s why:

Increased Demand for Construction Materials: As countries invest in infrastructure projects, there’s a surge in demand for construction materials like cement, aggregates, and steel. Companies like Vulcan Materials (VMC) play a crucial role in supplying these materials.

Roads and Bridges: Repairing and building roads, bridges, and highways require massive quantities of raw materials. For instance, Alcoa (AA) provides aluminum for lightweight bridges, while Cleveland-Cliffs (CLF) supplies iron ore for steel production.

Utilities and Water Systems: Upgrading water treatment plants, pipelines, and utilities necessitates materials such as pipes, valves, and concrete from companies like Cemex (CX) which is a global cement supplier used in water infrastructure projects.

Metals and Mining: Companies like Freeport-McMoRan (FCX) benefit from increased demand for copper and other metals used in electrical grids, renewable energy systems, and transportation.

Building Materials: James Hardie Industries (JHX) produces fiber cement siding and other building materials which are essential for both residential and commercial infrastructure projects.

Steel Production: ArcelorMittal (MT) is a major steel producer. Steel is vital for constructing bridges, railways, and buildings.

Material Stocks Provide Reliable cash flow

Material stocks belong to companies that manufacture, mine, and produce core materials used across various industries. These materials include metals, concrete, chemicals, and more.

Regardless of economic conditions, there’s a consistent demand for these essential materials. Sectors like health care, food, and power generation rely on them.

As a result, material stocks tend to have a certain floor of demand, making their cash flow relatively stable

Material Stocks Provide Above-average Dividend Yields

As of 2024, the basic materials sector has an average stock dividend yield of 4.92%. In comparison, basic material stocks within the S&P 500 have an average yield of 2.5%. Keep in mind that individual companies may offer higher or lower yields, so thorough research is essential when considering investments.

The Cons of Investing in Basic Material Stocks

Investing in material stocks, like any other investment, comes with its own set of challenges and risks. Here are some of the cons associated with investing in material stocks:

- Business Cycle Sensitivity: Material stocks are generally sensitive to economic cycles. Their performance is closely tied to overall economic growth. During economic downturns, these stocks may experience a decline in demand and profitability.

- Cyclical Nature: The cyclical nature of materials stocks can be detrimental to investors’ portfolios, especially for those who prefer slow, steady, and consistent portfolio growth while enjoying as much dividends as possible.

- Capital Intensive: The basic materials sector is also capital-intensive. This means that companies in this sector often require a large amount of capital investment to fund their operations, which can lead to higher financial risk.

- Market Volatility: Like all stocks, material stocks are subject to market volatility. This can lead to fluctuations in the stock price, which can impact the value of your investment.

Final Thoughts

The materials sector, encompassing diverse industries like chemical producers, metals producers, construction materials, and wood-based goods, is a crucial component of the economy. It’s closely tied to the economic cycle, often performing well in the early stages of economic growth. Looking forward to 2025, the sector shows promising potential, particularly in areas like copper mining and US chemical manufacturing.

Trends such as sustainable materials, smart materials, nanotechnology, additive manufacturing, lightweighting, material informatics, advanced composites, and graphene & 2D materials are shaping the future of the sector. Despite a decline in lithium prices in 2024, forecasts predict price increases due to factors like surplus of raw materials for EV battery manufacturers and geopolitical trade barriers.

The agricultural chemical prices are also trending, with the 2024 Agricultural Chemical Price Transparency Report providing valuable insights. As the economy evolves, materials stocks could benefit from an eventual economic brightening. Goldman Sachs predicts that the materials sector will outperform the broader market in the next 12 months. Therefore, investing in material stocks could be a strategic move for investors looking to capitalize on these trends and forecasts.

Understanding the Materials Sector

The materials sector encompasses a diverse set of industries involved in the discovery, development, and processing of raw materials. The materials sector is closely tied to the economic cycle. It tends to rise and fall with overall economic growth. Historically, the material sector performs well in the early stages of new economic growth.

There are many sub-segments in the industrial sector. The main material sub-sectors

Chemical Producers - These companies manufacture fertilizers, industrial chemicals, and other chemical products.

Metals Producers - Includes gold and copper miners, steelmakers, and other metal refining businesses.

Construction Materials - Makers of cement, bricks, glass, gravel, and other construction-related materials.

Wood-Based Goods - Producers of lumber, paper packaging, and related products.

Importance in the Economy

The material sector plays a crucial role in the economy. The material sector is the starting point in the economy’s supply chain. All sectors build goods and services that start with materials produced from the materials sector.

Material companies work at discovering, developing, and processing raw materials—such as metals, minerals, timber, and oil. These materials serve as essential building blocks for various industries, including manufacturing, construction, and energy production. Manufacturing relies heavily on raw materials and is a key driver of economic growth.

The material sector affects more the manufacturing. Construction, farming and technology all start their value-add processes with materials from the material sector. Construction needs wood and iron, farming needs nitrogen, and technology needs silicon.

Current State of the Material Sector

Historically, it performs well during early stages of economic recovery. In 2023, the sector delivered positive but sluggish returns due to recession concerns. Copper mining is a materials Segment to Watch. There is favorable supply-and-demand which is making Copper Miners attractive for long-term investment. Also, the chemical manufacturing segment is holding strong in 2024. As for Building Materials, the construction industry is testing new materials driven by decarbonization efforts and changing consumer preferences. In terms of the Investment Landscape, over 2560 startups globally in the building materials industry. The average investment value per funding round was $50 million.

Material Sector Trends

Source: startus-insights.com

Source: grandviewresearch.com

lithium Prices Expected to Rise

Source: tradingeconomics.com

However, Lithium prices have experienced a decline in 2024 even though forecasts predict price increases. There are some key factors influencing the market. The surplus of raw materials for electric vehicle (EV) battery manufacturers has led to low prices. Lithium miners and producers continue to expand capacity, contributing to expectations of oversupply. On the supply side, government subsidies for firms across the EV supply chain have caused battery gluts, further impacting prices. Geopolitically, trade barriers are also distorting the market. The EU imposed tariffs on Chinese EV producers, and the US quadrupled duties on Chinese EVs, affecting input materials for battery production. Goldman Sachs estimates lithium carbonate prices at $13,377 per tonne and lithium hydroxide at $14,263 per tonne in 2024. S&P Global projects stabilization near current levels, ranging between $20,000 per metric tonne and $25,000 per metric tonne from 2024 to 2027.

Agricultural Chemical Prices are Trending

2024 Agricultural Chemical Price Transparency Report examined over 2,400 unique pricing data points across 33 states, covering more than 120 insecticides, fungicides, herbicides, and adjuvants. Additionally, the Producer Price Index for pesticide and other agricultural chemical manufacturing in July 2024 indicates trends in the industry.

Material Sector Forecasts

The materials sector, which includes industries like chemical producers, metals producers, construction materials, and wood-based goods, tends to move in sync with the broader economy. In 2023, it delivered positive but sluggish returns due to concerns over recession risk. As the economy evolves, materials stocks could benefit from an eventual economic brightening in 2024. Historically, this sector performs well in the early stages of new economic growth. Favorable supply-demand dynamics may exist in some areas of the sector. For instance, copper miners and US chemical manufacturers show promising potential. Manufacturers are increasingly adopting smart factory solutions, which could drive competitiveness and productivity in the materials industry.

Finally,The US construction market is expected to grow, supported by investments in infrastructure projects. With all these variables in mind, Goldman Sachs predicts that the materials sector will outperform the broader market in the next 12 months. Their analysis considers factors like commodity prices, supply chain disruptions, and global demand. Morgan Stanley’s research suggests that industrial metals (such as copper and aluminum) will experience strong demand due to infrastructure spending and green energy initiatives. They anticipate a positive outlook for materials companies.

Investing in Basic Materials Stocks

Investing in the material sectors have some differences from other sectors new investors should be aware of. The material sector is cyclical and tends to perform well during economic expansions, so be prepared for fluctuations. For example, this is different from the utility sector which will tend to not rise and fall with the general economy.

As we’ve noted early in the article, basic materials include chemicals, metals, construction materials, and wood-based goods. Be sure to research companies within these segments and understand that even these sub-segments react differently to market conditions. Finally, Look for favorable supply-demand dynamics. For instance, copper and certain chemicals may have strong demand. The material stock sector is influenced by the materials commodities market, which can be more volatile than material stocks.

The Pros of Investing in Basic Material Stocks

The material sector encompasses companies involved in mining, manufacturing, and processing raw materials. Investing in material stocks can be advantageous for the following reasons:

Resilience: Material stocks tend to perform well during economic cycles. Demand for core materials remains steady, even during downturns, as they underpin various industries.

Cyclical Upside: During economic expansions, material stocks benefit from increased demand. As economies grow, there’s greater need for construction materials, metals, chemicals, and other basic inputs.

Income Potential: Some material companies offer attractive dividends. Their consistent demand and stable cash flows allow them to distribute dividends, making them appealing for income-seeking investors.

Inflation Hedge: Material prices often rise during inflationary periods. Investing in material stocks can act as a hedge against inflation, preserving purchasing power.

Global Infrastructure Spending: As countries invest in infrastructure projects (roads, bridges, utilities), material stocks stand to gain. These projects require substantial raw materials.

Technological Advancements: Innovations in materials science drive demand for specialized materials (e.g., rare earth elements, advanced alloys). Companies at the forefront of such innovations can deliver strong returns.

Exposure to global economy and growth prospects

Material stocks stand to benefit significantly from global infrastructure spending. Here’s why:

Increased Demand for Construction Materials: As countries invest in infrastructure projects, there’s a surge in demand for construction materials like cement, aggregates, and steel. Companies like Vulcan Materials (VMC) play a crucial role in supplying these materials.

Roads and Bridges: Repairing and building roads, bridges, and highways require massive quantities of raw materials. For instance, Alcoa (AA) provides aluminum for lightweight bridges, while Cleveland-Cliffs (CLF) supplies iron ore for steel production.

Utilities and Water Systems: Upgrading water treatment plants, pipelines, and utilities necessitates materials such as pipes, valves, and concrete from companies like Cemex (CX) which is a global cement supplier used in water infrastructure projects.

Metals and Mining: Companies like Freeport-McMoRan (FCX) benefit from increased demand for copper and other metals used in electrical grids, renewable energy systems, and transportation.

Building Materials: James Hardie Industries (JHX) produces fiber cement siding and other building materials which are essential for both residential and commercial infrastructure projects.

Steel Production: ArcelorMittal (MT) is a major steel producer. Steel is vital for constructing bridges, railways, and buildings.

Material Stocks Provide Reliable cash flow

Material stocks belong to companies that manufacture, mine, and produce core materials used across various industries. These materials include metals, concrete, chemicals, and more. Regardless of economic conditions, there’s a consistent demand for these essential materials. Sectors like health care, food, and power generation rely on them. As a result, material stocks tend to have a certain floor of demand, making their cash flow relatively stable

Material Stocks Provide Above-average Dividend Yields

As of 2024, the basic materials sector has an average stock dividend yield of 4.92%. In comparison, basic material stocks within the S&P 500 have an average yield of 2.5%. Keep in mind that individual companies may offer higher or lower yields, so thorough research is essential when considering investments.

The Cons of Investing in Basic Material Stocks

Investing in material stocks, like any other investment, comes with its own set of challenges and risks. Here are some of the cons associated with investing in material stocks:

Final Thoughts

The materials sector, encompassing diverse industries like chemical producers, metals producers, construction materials, and wood-based goods, is a crucial component of the economy. It’s closely tied to the economic cycle, often performing well in the early stages of economic growth. Looking forward to 2025, the sector shows promising potential, particularly in areas like copper mining and US chemical manufacturing. Trends such as sustainable materials, smart materials, nanotechnology, additive manufacturing, lightweighting, material informatics, advanced composites, and graphene & 2D materials are shaping the future of the sector. Despite a decline in lithium prices in 2024, forecasts predict price increases due to factors like surplus of raw materials for EV battery manufacturers and geopolitical trade barriers. The agricultural chemical prices are also trending, with the 2024 Agricultural Chemical Price Transparency Report providing valuable insights. As the economy evolves, materials stocks could benefit from an eventual economic brightening. Goldman Sachs predicts that the materials sector will outperform the broader market in the next 12 months. Therefore, investing in material stocks could be a strategic move for investors looking to capitalize on these trends and forecasts.