Why Invest in Dover?

Dover Corporation is a strong investment candidate thanks to its consistent dividend growth, its robust financial performance, and strong capital implementation plan. This stock fits into a strong dividend portfolio well that plans on holding onto stocks for multiple years.

Dover Corporation expects strong growth in the coming year with estimated earnings to be $7.90 to $8.10 per share in 2024. With 2023 EPS at $7.52, the Dover executive team expects earnings per share to increase 5.3% to 7.7% in 2024.

Overall, Dover is a solid investment for new investors and dividend investors alike. Dover’s main divisions manufacture goods and services that are critical to multiple industrial businesses. Dover’s business segments are straight forward and can be understood by a typical retail investor.

Dover’s pumps and processing solutions is a broad segment of the company that touches chemical, food processing and oil and gas industries, just to name a few.

The company’s engineered solutions segment makes products used everyday inside a manufacturing company. These components include winches, clamps, and transport equipment.

Is DOV a dividend aristocrat?

Dover is a dividend aristocrat, which means it has increased its annual dividend payout for at least the last 25 consecutive years. Dover has been increasing its dividend quite regularly since 1972.

Dover has managed to keep its dividend growing through a combination of strategies. The company has made numerous acquisitions in the last few decades which have consolidated into its main segments today. The company has also allocated its capital prudently by either conducting acquisitions or conducting share buybacks.

As for the risk to its dividend, Dover’s dividend appears to be safe. The company has a low and conservative payout ratio of 26.9%. This means only about a quarter of Dover’s earnings is given out as a dividend.

Is DOV a Good Long-Term Investment?

Dover is a great long-term investment due to its consistent growth, capital allocation plan, diversified portfolio, and revenue growth. Expect Dover’s revenue and book-value to continue growing into the rest of the 2020s.

Dover is a significant player in the pumps market thanks to its Pumps and Process Solutions segment. Revenue in 2022 was $1.7 Billion. The global pumps market is estimated to be $70 Billion in 2022, which means that Dover makes up roughly 2.5% of the overall market.

This indicates a significant market opportunity for the Dover Corporation to continue to gain market share as they expand internationally. The pumps market is estimated to increase over the next 10 years.

Is Dover (DOV) a Buy?

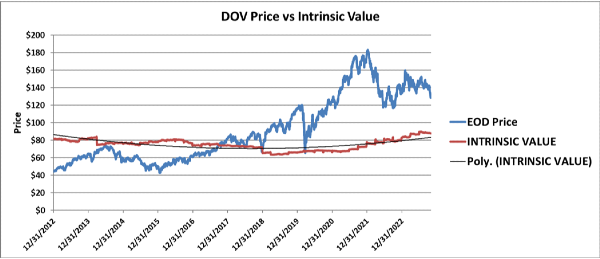

Though Dover is a great investment, we currently cannot claim it’s a good buy. Our analysis notes that the company is significantly overvalued thanks to the market paying a premium for the company’s strong growth potential. Like other stocks we’ve analyzed such as American Express and Union Pacific, the price of Dover Corporation fell right to its intrinsic value during Covid-19, showing the true price value investors want to buy into Dover Corporation.

The current estimated intrinsic value is only $110, compared to a stock price of $164. This stock price comes from taking a book value of $36.50 and earnings of $7.52, discounted over the next 10 years with an estimated 5% growth.

Even though EPS growth is estimated to be up to 7% by the company, their real performance has only been about 5% growth. Until they can prove their cost savings initiatives are coming to fruition, using a 7% growth rate seems unwise. Dover’s earnings have been relatively flat for the past couple years, while revenue has been growing.

Dover Corporation has seen consistent revenue growth over the past six years.

- 2018: $6.992 billion

- 2019: $7.136 billion

- 2020: $6.684 billion

- 2021: $7.907 billion

- 2022: $8.508 billion

- 2023: $8.438 billion

This growth can be attributed to a combination of factors:

1.) Healthy Growth Across all Segments. The company’s diversified portfolio of businesses and industries have also all shown healthy growth since 2019.

Each segment has seen revenue growth since 2020.

- The Pumps and Process Solutions segment increased 30% between 2020 and 2022.

- Image and Identification jumped 9% in revenue in the same period.

- Clean Energy and Fueling revenue increased about 25%.

- Engineered products increased revenue by about 30%.

- The Climate and Sustainability segment increased revenue by about 30%.

2). Strategic Acquisitions

Dover Corporation has made numerous acquisitions in the last few years that have helped to boost earnings. The details of some of those acquisitions are discussed later in the article.

3). Strong Backlog and Customer Demand.

Management noted on the Q2 2023 results:

"We have a constructive outlook for the remainder of the year and see a solid foundation building for 2024. Underlying demand remains good across the portfolio, and a significant volume of business is already in the backlog. Our flexible business model and execution playbook are proven to deliver results in various operating conditions."

DOV Book Value per Share

Dover Corporations’s book value has increased due to robust revenue performance and consistent earnings. Dover’s intangibles and goodwill is at about $6 Billion, in line with expected goodwill based on acquisition activity. As of 2022, Goodwill accounted for $4.669 Billion of the company’s balance sheet. Being that goodwill is a significant portion of the company’s equity, the 2022 Dover annual report discusses the audit procedures in detail on page 61. Some key notes about the audit process:

- Evaluation of management’s controls related to revenue growth projections and cash flow model

- Assessing the results of the sensitivities over the assumptions in the discounted cash flow model

- Testing the reasonableness of significant assumptions made by management

- Comparing the growth rates forecasted to previous time periods and industry data.

If Goodwill was wiped away from the company’s book value, this could signify a reduction of the company’s intrinsic value by $30 per share.

In previous years, book value per share has fallen sharply, likely due to the reassessment of the company’s Goodwill. These dramatic falls are taken into consideration in our intrinsic value model and is one reason why we are cautious about the current valuations the market has set on Dover Corporation.

DOV Earnings

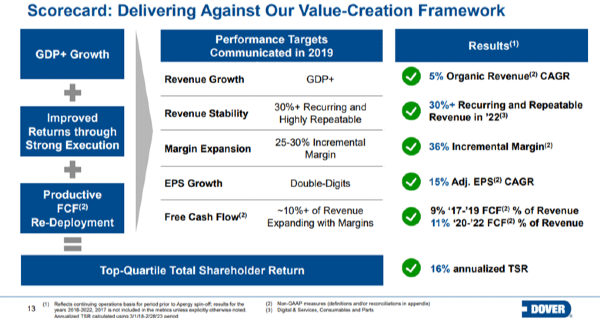

After growing in 2019 and 2020, Dover’s earnings have been stagnant for the last 12 quarters. The company has forecasted about 7% earnings growth in 2024.

This forecast looks possible as the company cuts costs by merging similar companies they have acquired and eliminating redundancies. The company has a goal of double-digit EPS growth moving forward and increased cash flow. Their previous results saw a 15% adjusted EPS CAGR.

While earnings have historically been muted, it could be possible the earnings will start to grow again in the coming decade thanks to a strong organic growth plan and a consistent bolt-on acquisition process.

What is Dover’s Stock Forecast?

Dover has a lot of potential and if they can continue to grow earnings, they will see significant growth in their intrinsic value. In the past few years, intrinsic value eroded as earnings growth was lack luster and investor equity was muted.

Overall, value investors should watch for the following concerns when monitoring Dover and conducting a value investment analysis

Is Goodwill being wiped away? - Dover has made numerous acquisitions and have accumulated significant goodwill. This Goodwill only exists if forecasted growth continues. If growth does not continue, then Dover overpaid for their acquisitions and the Goodwill will be wiped away from the balance sheet. Hence, failing to meet earnings, revenue, or cashflow expectations overall or in one particular business segment could lead to a cascading fall in intrinsic value.

Does Dover hit the 7% EPS growth? - Ultimately, Dover’s executive team is selling to investors that they can organically grow their numerous acquisitions more efficiently when they are merged together. This is very likely a good plan, as the acquisitions they take on have specific industry niches with low competition. This allows them to increase pricing without significant competition. But execution is still key. The institutional investors who own Dover have already priced in Dover’s successful execution of the plan.

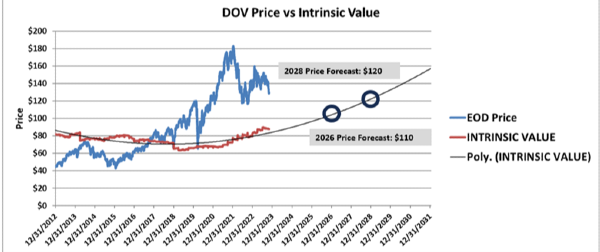

What is Dover’s 2026 Stock Forecast?

We set a price target for Dover at $110. The company looks to be overvalued based on historical EPS growth. While management’s plan looks promising, Wall Street has already priced in the successful execution of the plan. This means that 7% growth is likely the top line growth you could reach with the stock’s price going into 2025. Hence, a max price of $170 may be possible. A target price of $110 would be suggested for value investors. That price isn’t yet discounting any risk factors attributed to the goodwill of the company or the earnings risk. Thanks to Dover’s business diversification, market segment drops are likely not a significant risk. However, the underperformance of the company’s acquisitions could have an impact on the stock’s forecasted prices.

What is Dover’s 5-year Forecast?

Using a polynomial growth trendline, Dover could start to have a strong price trajectory through the rest of the 2020s. Nonetheless, Dover’s 5-year forecast is still $120. This is a low-end price target, but if another market collapse occurs, Dover’s stock price will likely hit its intrinsic value just like it did during Covid-19.

About Dover

Dover Corporation is a diversified global manufacturer and solutions provider with an impressive annual revenue of over $8 billion. As an industry leader, Dover delivers innovative equipment and components, consumable supplies, aftermarket parts, software and digital solutions, and support services.

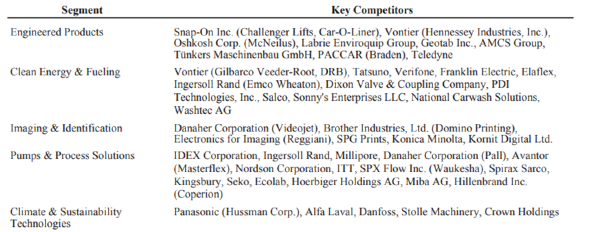

Dover Corporation’s Competitors

Dover Corporation spelled out their key competitors in their 2022 annual report:

Here are some of Dover Corporation’s competitors, along with their dividends and the market segments they compete in:

1). Gardner Denver: A global provider of industrial and well-being technology. They compete with Dover in various segments, including pumps and process solutions. Gardner Denver isn’t publicly traded.

2). Eaton Corporation: Eaton is a power management company providing energy-efficient solutions. They compete with Dover in several areas, including electrical systems and services. Their current 2024 dividend yield is 1.21%.

3). Hubbell Incorporated: Hubbell designs, manufactures, and sells electrical and electronic products. They compete with Dover in the electrical sector. Their current 2024 dividend yield is 1.33%.

4). Illinois Tool Works: ITW is a global manufacturer of industrial products and equipment. They compete with Dover in various segments, including automotive OEM, food equipment, and construction products. As of my last update in 2021, ITW had a 2024 dividend yield of 2.15%.

5). Cameron: Cameron is a provider of flow equipment products, systems, and services to worldwide oil, gas, and process industries. They compete with Dover in the oil and gas industry. Cameron is a private company.

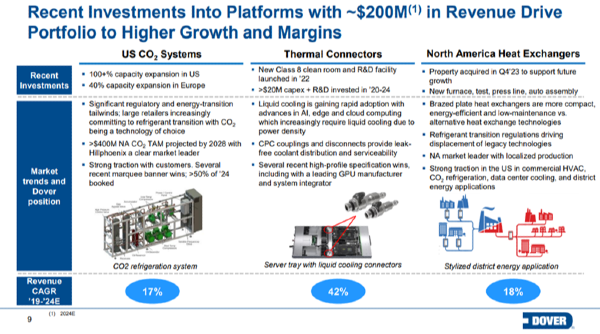

Dover’s Recent Acquisitions

In 2023, Dover completed the acquisition of FW Murphy Production Controls, LLC for a cash consideration of $530 million.

FW Murphy provides reciprocating compressor control, remote monitoring, digital-twin-based predictive maintenance, and adaptive performance optimization components, solutions, and instruments2. This business has become part of Dover’s Pumps & Process Solutions unit.

Dover Corporation made two acquisition in clean energy in 2021.

Per the acquisition announcement:

“Acme Cryogenics, Inc. was acquired for $295 million1. Established in 1969 and headquartered in Allentown, PA, Acme is a provider of highly-engineered, mission-critical components and services that facilitate the production, storage, and distribution of cryogenic gases used in a diverse set of applications1. Acme’s products are highly complementary to Dover’s existing clean energy solutions1.

Engineered Controls International, LLC (RegO)1: Dover entered into a definitive agreement to acquire RegO for $631 million1. Established in 1918 and headquartered in Elon, NC, RegO is a well-established provider of similar services to Acme. RegO’s products will also enhance Dover’s offerings for clean energy applications.”

These acquisitions are part of Dover’s strategy to enhance its portfolio with growing participation in clean fuels and other attractive adjacencies.

I/we have no positions in any asset mentioned, and no plans to initiate any positions for the next 7 days

Why Invest in Dover?

Dover Corporation is a strong investment candidate thanks to its consistent dividend growth, its robust financial performance, and strong capital implementation plan. This stock fits into a strong dividend portfolio well that plans on holding onto stocks for multiple years.

Dover Corporation expects strong growth in the coming year with estimated earnings to be $7.90 to $8.10 per share in 2024. With 2023 EPS at $7.52, the Dover executive team expects earnings per share to increase 5.3% to 7.7% in 2024. Overall, Dover is a solid investment for new investors and dividend investors alike. Dover’s main divisions manufacture goods and services that are critical to multiple industrial businesses. Dover’s business segments are straight forward and can be understood by a typical retail investor.

Dover’s pumps and processing solutions is a broad segment of the company that touches chemical, food processing and oil and gas industries, just to name a few.

The company’s engineered solutions segment makes products used everyday inside a manufacturing company. These components include winches, clamps, and transport equipment.

Is DOV a dividend aristocrat?

Dover is a dividend aristocrat, which means it has increased its annual dividend payout for at least the last 25 consecutive years. Dover has been increasing its dividend quite regularly since 1972.

Dover has managed to keep its dividend growing through a combination of strategies. The company has made numerous acquisitions in the last few decades which have consolidated into its main segments today. The company has also allocated its capital prudently by either conducting acquisitions or conducting share buybacks.

As for the risk to its dividend, Dover’s dividend appears to be safe. The company has a low and conservative payout ratio of 26.9%. This means only about a quarter of Dover’s earnings is given out as a dividend.

Is DOV a Good Long-Term Investment?

Dover is a great long-term investment due to its consistent growth, capital allocation plan, diversified portfolio, and revenue growth. Expect Dover’s revenue and book-value to continue growing into the rest of the 2020s.

Dover is a significant player in the pumps market thanks to its Pumps and Process Solutions segment. Revenue in 2022 was $1.7 Billion. The global pumps market is estimated to be $70 Billion in 2022, which means that Dover makes up roughly 2.5% of the overall market. This indicates a significant market opportunity for the Dover Corporation to continue to gain market share as they expand internationally. The pumps market is estimated to increase over the next 10 years.

Is Dover (DOV) a Buy?

Though Dover is a great investment, we currently cannot claim it’s a good buy. Our analysis notes that the company is significantly overvalued thanks to the market paying a premium for the company’s strong growth potential. Like other stocks we’ve analyzed such as American Express and Union Pacific, the price of Dover Corporation fell right to its intrinsic value during Covid-19, showing the true price value investors want to buy into Dover Corporation.

The current estimated intrinsic value is only $110, compared to a stock price of $164. This stock price comes from taking a book value of $36.50 and earnings of $7.52, discounted over the next 10 years with an estimated 5% growth.

Even though EPS growth is estimated to be up to 7% by the company, their real performance has only been about 5% growth. Until they can prove their cost savings initiatives are coming to fruition, using a 7% growth rate seems unwise. Dover’s earnings have been relatively flat for the past couple years, while revenue has been growing.

DOV EPS Trends

Dover Corporation has seen consistent revenue growth over the past six years.

This growth can be attributed to a combination of factors:

1.) Healthy Growth Across all Segments. The company’s diversified portfolio of businesses and industries have also all shown healthy growth since 2019.

Dover Q4 2023 Earnings release, slide 9

Each segment has seen revenue growth since 2020.

2). Strategic Acquisitions Dover Corporation has made numerous acquisitions in the last few years that have helped to boost earnings. The details of some of those acquisitions are discussed later in the article.

3). Strong Backlog and Customer Demand. Management noted on the Q2 2023 results:

"We have a constructive outlook for the remainder of the year and see a solid foundation building for 2024. Underlying demand remains good across the portfolio, and a significant volume of business is already in the backlog. Our flexible business model and execution playbook are proven to deliver results in various operating conditions."

DOV Book Value per Share

Dover Corporations’s book value has increased due to robust revenue performance and consistent earnings. Dover’s intangibles and goodwill is at about $6 Billion, in line with expected goodwill based on acquisition activity. As of 2022, Goodwill accounted for $4.669 Billion of the company’s balance sheet. Being that goodwill is a significant portion of the company’s equity, the 2022 Dover annual report discusses the audit procedures in detail on page 61. Some key notes about the audit process:

If Goodwill was wiped away from the company’s book value, this could signify a reduction of the company’s intrinsic value by $30 per share.

In previous years, book value per share has fallen sharply, likely due to the reassessment of the company’s Goodwill. These dramatic falls are taken into consideration in our intrinsic value model and is one reason why we are cautious about the current valuations the market has set on Dover Corporation.

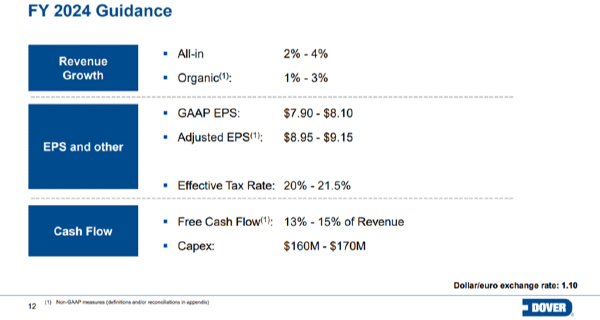

DOV Earnings

After growing in 2019 and 2020, Dover’s earnings have been stagnant for the last 12 quarters. The company has forecasted about 7% earnings growth in 2024.

Dover Corporation’s FY 2024 Guidance.

This forecast looks possible as the company cuts costs by merging similar companies they have acquired and eliminating redundancies. The company has a goal of double-digit EPS growth moving forward and increased cash flow. Their previous results saw a 15% adjusted EPS CAGR.

Dover Corporation 2023 Analyst and Investor Meeting, slide 13

While earnings have historically been muted, it could be possible the earnings will start to grow again in the coming decade thanks to a strong organic growth plan and a consistent bolt-on acquisition process.

What is Dover’s Stock Forecast?

Dover has a lot of potential and if they can continue to grow earnings, they will see significant growth in their intrinsic value. In the past few years, intrinsic value eroded as earnings growth was lack luster and investor equity was muted.

Overall, value investors should watch for the following concerns when monitoring Dover and conducting a value investment analysis

Is Goodwill being wiped away? - Dover has made numerous acquisitions and have accumulated significant goodwill. This Goodwill only exists if forecasted growth continues. If growth does not continue, then Dover overpaid for their acquisitions and the Goodwill will be wiped away from the balance sheet. Hence, failing to meet earnings, revenue, or cashflow expectations overall or in one particular business segment could lead to a cascading fall in intrinsic value.

Does Dover hit the 7% EPS growth? - Ultimately, Dover’s executive team is selling to investors that they can organically grow their numerous acquisitions more efficiently when they are merged together. This is very likely a good plan, as the acquisitions they take on have specific industry niches with low competition. This allows them to increase pricing without significant competition. But execution is still key. The institutional investors who own Dover have already priced in Dover’s successful execution of the plan.

What is Dover’s 2026 Stock Forecast?

We set a price target for Dover at $110. The company looks to be overvalued based on historical EPS growth. While management’s plan looks promising, Wall Street has already priced in the successful execution of the plan. This means that 7% growth is likely the top line growth you could reach with the stock’s price going into 2025. Hence, a max price of $170 may be possible. A target price of $110 would be suggested for value investors. That price isn’t yet discounting any risk factors attributed to the goodwill of the company or the earnings risk. Thanks to Dover’s business diversification, market segment drops are likely not a significant risk. However, the underperformance of the company’s acquisitions could have an impact on the stock’s forecasted prices.

What is Dover’s 5-year Forecast?

Using a polynomial growth trendline, Dover could start to have a strong price trajectory through the rest of the 2020s. Nonetheless, Dover’s 5-year forecast is still $120. This is a low-end price target, but if another market collapse occurs, Dover’s stock price will likely hit its intrinsic value just like it did during Covid-19.

About Dover

Dover Corporation is a diversified global manufacturer and solutions provider with an impressive annual revenue of over $8 billion. As an industry leader, Dover delivers innovative equipment and components, consumable supplies, aftermarket parts, software and digital solutions, and support services.

Dover Corporation’s Competitors

Dover Corporation spelled out their key competitors in their 2022 annual report:

Dover 2022 Annual Report, Page 19

Here are some of Dover Corporation’s competitors, along with their dividends and the market segments they compete in:

1). Gardner Denver: A global provider of industrial and well-being technology. They compete with Dover in various segments, including pumps and process solutions. Gardner Denver isn’t publicly traded.

2). Eaton Corporation: Eaton is a power management company providing energy-efficient solutions. They compete with Dover in several areas, including electrical systems and services. Their current 2024 dividend yield is 1.21%.

3). Hubbell Incorporated: Hubbell designs, manufactures, and sells electrical and electronic products. They compete with Dover in the electrical sector. Their current 2024 dividend yield is 1.33%.

4). Illinois Tool Works: ITW is a global manufacturer of industrial products and equipment. They compete with Dover in various segments, including automotive OEM, food equipment, and construction products. As of my last update in 2021, ITW had a 2024 dividend yield of 2.15%.

5). Cameron: Cameron is a provider of flow equipment products, systems, and services to worldwide oil, gas, and process industries. They compete with Dover in the oil and gas industry. Cameron is a private company.

Dover’s Recent Acquisitions

In 2023, Dover completed the acquisition of FW Murphy Production Controls, LLC for a cash consideration of $530 million.

FW Murphy provides reciprocating compressor control, remote monitoring, digital-twin-based predictive maintenance, and adaptive performance optimization components, solutions, and instruments2. This business has become part of Dover’s Pumps & Process Solutions unit.

Dover Corporation made two acquisition in clean energy in 2021.

Per the acquisition announcement: “Acme Cryogenics, Inc. was acquired for $295 million1. Established in 1969 and headquartered in Allentown, PA, Acme is a provider of highly-engineered, mission-critical components and services that facilitate the production, storage, and distribution of cryogenic gases used in a diverse set of applications1. Acme’s products are highly complementary to Dover’s existing clean energy solutions1.

Engineered Controls International, LLC (RegO)1: Dover entered into a definitive agreement to acquire RegO for $631 million1. Established in 1918 and headquartered in Elon, NC, RegO is a well-established provider of similar services to Acme. RegO’s products will also enhance Dover’s offerings for clean energy applications.”

These acquisitions are part of Dover’s strategy to enhance its portfolio with growing participation in clean fuels and other attractive adjacencies.

I/we have no positions in any asset mentioned, and no plans to initiate any positions for the next 7 days