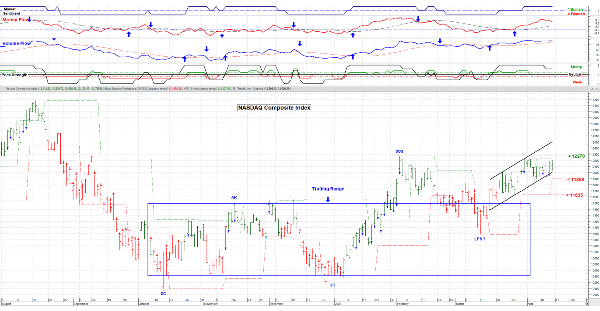

April 14, 2023 – I typically use multiple sources to check my own analysis each week. And this week the phase that stuck with me was “It’s about to get much better or much worse”. This dichotomy of thinking actually makes sense, at least to me. Since the mid October lows in the markets we’ve had a steady interest rate rise and banks (& the FED) bailing out other banks worldwide. Add to that inflation remaining stubbornly high and corporate forward earnings guidance lower plus increasing layoffs (especially in the Tech industry). But . . . the market went higher; good news, right?

Oh, I forgot to mention the war in Ukraine and the strain that it is putting on many western countries. My “take” on why is basic human nature: “I want to pick the bottom”. Folks are just afraid of missing out and are willing to take a chance that the economy and markets will improve, and soon. After all, why wait?

Consensus is that the FED will stop raising interest rates after the May ¼% increase then maybe (just maybe) start to lower them late Summer / Fall. OK, but even IF that comes to pass history shows us that recessions actual start when the FED lowers rates, so the “bet” must be that we’re going to have a soft landings and no significant recession of economic growth. That could be and the lows in October may hold; “About to Get Much Better”. Or not: “About to Get Much Worse” with an actual significant contraction in the economy and lower earnings. The bottom line is no one really knows with any certainty and there still is a lot of money on the sidelines waiting.

I note that just 5 companies (Apple, Google, Microsoft, Tesla & Amazon) make up over 20% of the S&P 500 Index (because it is capital weighted; bigger companies have the most influence). That largeness allows institutions the liquidity to move in and out easier without affecting prices. I note that just 53% of the companies in the Index are above their 50 day moving average. Not a broad vote of confidence.

March Retail Sales were disappointing on Friday and both the 10 and 30 year bond auctions yielded higher interest rates. On the flip side, big banks reported great earnings, likely with the help of a very liquid FED to support the industry. First quarter earning start to gear up this week and that may be a window into future corporate earnings and perceived economic strength. So we remain in a broad range, trying to move higher but so far having trouble getting above the mid-August high. I am taking scaled and cautious positions but not completely convinced that we’re “out of the woods” just yet.

Have a Good Week. ………… Tom …………

Price chart by MetaStock; Used with permission.

April 14, 2023 – I typically use multiple sources to check my own analysis each week. And this week the phase that stuck with me was “It’s about to get much better or much worse”. This dichotomy of thinking actually makes sense, at least to me. Since the mid October lows in the markets we’ve had a steady interest rate rise and banks (& the FED) bailing out other banks worldwide. Add to that inflation remaining stubbornly high and corporate forward earnings guidance lower plus increasing layoffs (especially in the Tech industry). But . . . the market went higher; good news, right?

Oh, I forgot to mention the war in Ukraine and the strain that it is putting on many western countries. My “take” on why is basic human nature: “I want to pick the bottom”. Folks are just afraid of missing out and are willing to take a chance that the economy and markets will improve, and soon. After all, why wait?

Consensus is that the FED will stop raising interest rates after the May ¼% increase then maybe (just maybe) start to lower them late Summer / Fall. OK, but even IF that comes to pass history shows us that recessions actual start when the FED lowers rates, so the “bet” must be that we’re going to have a soft landings and no significant recession of economic growth. That could be and the lows in October may hold; “About to Get Much Better”. Or not: “About to Get Much Worse” with an actual significant contraction in the economy and lower earnings. The bottom line is no one really knows with any certainty and there still is a lot of money on the sidelines waiting.

I note that just 5 companies (Apple, Google, Microsoft, Tesla & Amazon) make up over 20% of the S&P 500 Index (because it is capital weighted; bigger companies have the most influence). That largeness allows institutions the liquidity to move in and out easier without affecting prices. I note that just 53% of the companies in the Index are above their 50 day moving average. Not a broad vote of confidence.

March Retail Sales were disappointing on Friday and both the 10 and 30 year bond auctions yielded higher interest rates. On the flip side, big banks reported great earnings, likely with the help of a very liquid FED to support the industry. First quarter earning start to gear up this week and that may be a window into future corporate earnings and perceived economic strength. So we remain in a broad range, trying to move higher but so far having trouble getting above the mid-August high. I am taking scaled and cautious positions but not completely convinced that we’re “out of the woods” just yet.

Have a Good Week. ………… Tom ………… Price chart by MetaStock; Used with permission.