If you enjoy reading this blog, please leave a star rating on WealthTender. Thank you!

The ramifications of the big fall in Gilts will be far reaching

You may have heard or read that Gilt yields have been rising sharply recently. Rarely, however, is one told what the percentage change in the underlying Gilt has been, whether over the day or, of more relevance, a longer period.

You may also have heard that Gilts are low risk, perhaps from an investment professional. They offer steady - low risk - returns, you perhaps were told, because the UK government and others like it do not tend to default. The reason for this is that governments can always increase taxes if necessary in order to make coupon and principal payments to bond holders. Bond holders, in return, accept returns from bonds commensurate with the lower risk.

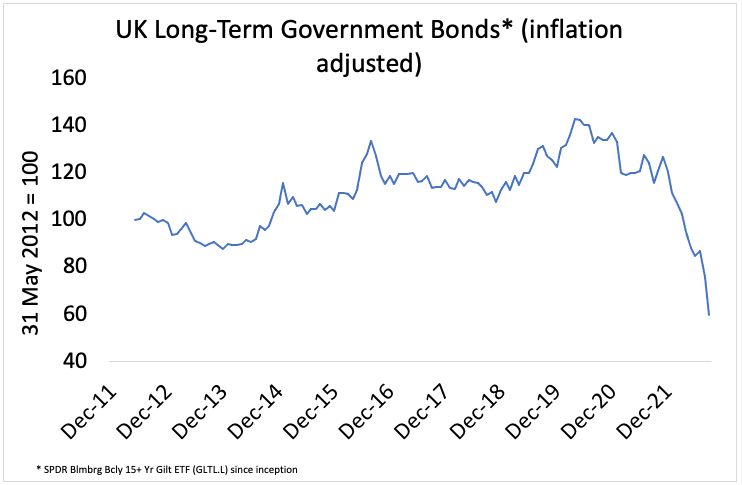

Below is a chart of the Bloomberg Barclays 15+ Gilt Index, or rather an ETF that tracks it. It is adjusted for inflation as indeed all financial asset prices should be - what £100 buys you today is very different to what £100 bought you 20 years ago, and two nominal amounts should never, in my view, be compared with each other. Unless, that is, they are first adjusted for the change in the price of goods and services over the 20 years...

Source: https://uk.finance.yahoo.com/

Source: https://uk.finance.yahoo.com/

To be clear, the chart is of the real price of long duration Gilts, those with a maturity of 15 years or more. Short-duration Gilts will not have fallen nearly as much as long-duration Gilts, but they will still have fallen considerably, something you may well have been told they do not do. Unlike long duration Gilts which are low risk, short duration Gilts are very low risk. Blah blah.

Since April 2020, long-term Gilts have fallen by 58pct, equivalent to -30pct annualised. Over the last three months they have fallen by 29pct, equivalent to -75pct annualised. Low risk? Hmmm.

You may well think that similar falls have been seen in other bond markets. Wrong. Below is a chart of the real value of long-term Gilts relative to their US equivalents, real long-term Treasuries. Ouch.

Source: https://uk.finance.yahoo.com/

Source: https://uk.finance.yahoo.com/

You may well also wonder if the big fall in Gilts is related to a big increase in their default risk. Again, this would be wrong. The chart below is of the UK 5 Years CDS (credit default swap) price. The CDS price as of Monday was 26.70bp, equivalent to an implied probability of default of 0.45pct (assuming a 40pct recovery rate). This is still low, and so the rise in the default risk since June will only have accounted for a small portion of the fall in bond values.

Source: http://www.worldgovernmentbonds.com/cds-historical-data/united-kingdom/5-years/

Source: http://www.worldgovernmentbonds.com/cds-historical-data/united-kingdom/5-years/

The ramifications of the falls in real Gilt values - whether recently or over the last two and a half years - will be far reaching.

Many, particularly those in retirement, will have been advised to invest in "safe" government bonds. Lower retirement income as a result of significantly lower bond prices will impact spending.

Other big holders of Gilts such as insurance companies will be nursing huge losses.

And if you are squeamish, don't look at the Bank of England's balance sheet...

As for the increase in borrowing costs for the UK government and thus for us as UK taxpayers, this will be substantial and felt progressively over the coming decades as old Gilts mature and new ones are issued at higher yields. The UK government may also wish to continue to increase total borrowing.

If markets let them, that is.

The views expressed in this communication are those of Peter Elston at the time of writing and are subject to change without notice. They do not constitute investment advice and whilst all reasonable efforts have been used to ensure the accuracy of the information contained in this communication, the reliability, completeness or accuracy of the content cannot be guaranteed. This communication provides information for professional use only and should not be relied upon by retail investors as the sole basis for investment.

© Chimp Investor Ltd

If you enjoy reading this blog, please leave a star rating on WealthTender. Thank you!

The ramifications of the big fall in Gilts will be far reaching

You may have heard or read that Gilt yields have been rising sharply recently. Rarely, however, is one told what the percentage change in the underlying Gilt has been, whether over the day or, of more relevance, a longer period.

You may also have heard that Gilts are low risk, perhaps from an investment professional. They offer steady - low risk - returns, you perhaps were told, because the UK government and others like it do not tend to default. The reason for this is that governments can always increase taxes if necessary in order to make coupon and principal payments to bond holders. Bond holders, in return, accept returns from bonds commensurate with the lower risk.

Below is a chart of the Bloomberg Barclays 15+ Gilt Index, or rather an ETF that tracks it. It is adjusted for inflation as indeed all financial asset prices should be - what £100 buys you today is very different to what £100 bought you 20 years ago, and two nominal amounts should never, in my view, be compared with each other. Unless, that is, they are first adjusted for the change in the price of goods and services over the 20 years...

To be clear, the chart is of the real price of long duration Gilts, those with a maturity of 15 years or more. Short-duration Gilts will not have fallen nearly as much as long-duration Gilts, but they will still have fallen considerably, something you may well have been told they do not do. Unlike long duration Gilts which are low risk, short duration Gilts are very low risk. Blah blah.

Since April 2020, long-term Gilts have fallen by 58pct, equivalent to -30pct annualised. Over the last three months they have fallen by 29pct, equivalent to -75pct annualised. Low risk? Hmmm.

You may well think that similar falls have been seen in other bond markets. Wrong. Below is a chart of the real value of long-term Gilts relative to their US equivalents, real long-term Treasuries. Ouch.

You may well also wonder if the big fall in Gilts is related to a big increase in their default risk. Again, this would be wrong. The chart below is of the UK 5 Years CDS (credit default swap) price. The CDS price as of Monday was 26.70bp, equivalent to an implied probability of default of 0.45pct (assuming a 40pct recovery rate). This is still low, and so the rise in the default risk since June will only have accounted for a small portion of the fall in bond values.

The ramifications of the falls in real Gilt values - whether recently or over the last two and a half years - will be far reaching.

Many, particularly those in retirement, will have been advised to invest in "safe" government bonds. Lower retirement income as a result of significantly lower bond prices will impact spending.

Other big holders of Gilts such as insurance companies will be nursing huge losses.

And if you are squeamish, don't look at the Bank of England's balance sheet...

As for the increase in borrowing costs for the UK government and thus for us as UK taxpayers, this will be substantial and felt progressively over the coming decades as old Gilts mature and new ones are issued at higher yields. The UK government may also wish to continue to increase total borrowing.

If markets let them, that is.

The views expressed in this communication are those of Peter Elston at the time of writing and are subject to change without notice. They do not constitute investment advice and whilst all reasonable efforts have been used to ensure the accuracy of the information contained in this communication, the reliability, completeness or accuracy of the content cannot be guaranteed. This communication provides information for professional use only and should not be relied upon by retail investors as the sole basis for investment.

© Chimp Investor Ltd

Originally posted on chimpinvestor.com