Sound investments

don't happen alone

Find your crew, build teams, compete in VS MODE, and identify investment trends in our evergrowing investment ecosystem. You aren't on an island anymore, and our community is here to help you make informed decisions in a complex world.

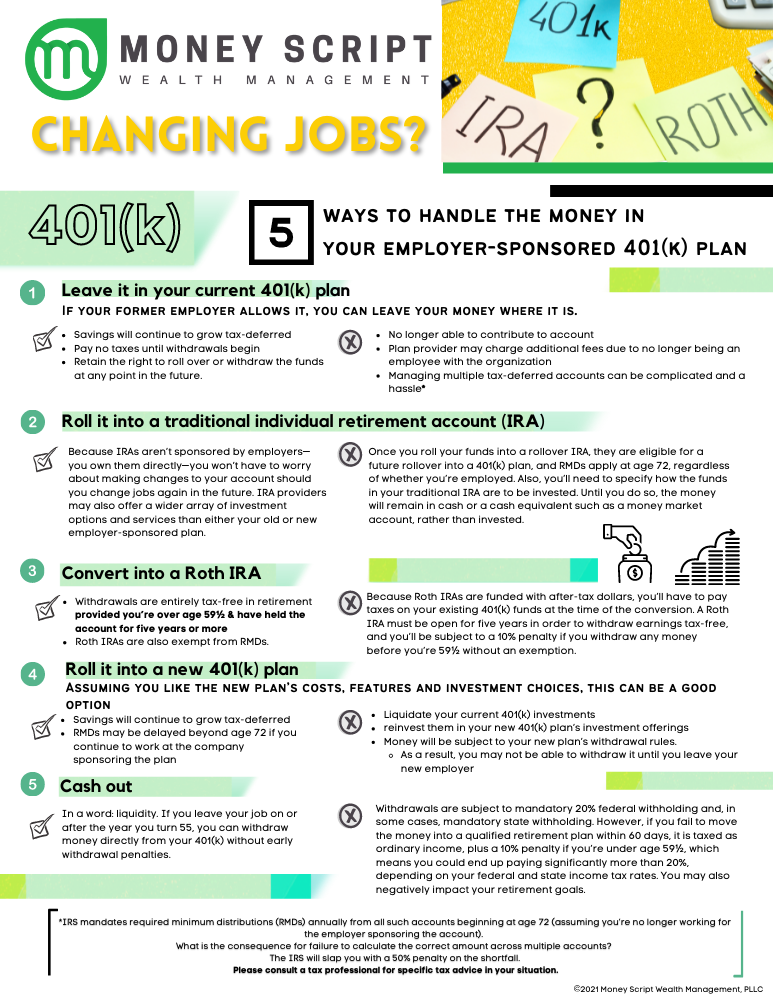

Changing Jobs: 5 Ways to Handle your 401(k)

Pros: Savings will continue to grow tax-deferred Pay no taxes until withdrawals begin Retain the right to roll over or withdraw the funds at any point in the future. Cons: No longer able to contribute to account Plan provider may charge additional fees due to no longer being an employee with the organization Managing multiple tax-deferred accounts can be complicated and a hassle* 2. Roll it into a traditional individual retirement account (IRA) Pros: Because IRAs aren’t sponsored by employers—you own them directly—you won’t have to worry about making changes to your account should you change jobs again in the future. IRA providers may also offer a wider array of investment options and services than either your old or new employer-sponsored plan. Cons Once you roll your funds into a rollover IRA, they are eligible for a future rollover into a 401(k) plan, and RMDs apply at age 72, regardless of whether you’re employed. Also, you’ll need to specify how the funds in your traditional IRA are to be invested. Until you do so, the money will remain in cash or a cash equivalent such as a money market account, rather than invested. 4.Convert into a Roth IRA Pros: Withdrawals are entirely tax-free in retirement provided you’re over age 59½ & have held the account for five years or more Roth IRAs are also exempt from RMDs. Cons Because Roth IRAs are funded with after-tax dollars, you’ll have to pay taxes on your existing 401(k) funds at the time of the conversion. A Roth IRA must be open for five years in order to withdraw earnings tax-free, and you’ll be subject to a 10% penalty if you withdraw any money before you’re 59½ without an exemption. 5. Roll it into a new 401(k) plan Assuming you like the new plan’s costs, features and investment choices, this can be a good option Pros: Savings will continue to grow tax-deferred RMDs may be delayed beyond age 72 if you continue to work at the company sponsoring the plan Cons Liquidate your current 401(k) investments reinvest them in your new 401(k) plan’s investment offerings Money will be subject to your new plan’s withdrawal rules. As a result, you may not be able to withdraw it until you leave your new employer 5.Cash Out Pros: In a word: liquidity. If you leave your job on or after the year you turn 55, you can withdraw money directly from your 401(k) without early withdrawal penalties. Cons Withdrawals are subject to mandatory 20% federal withholding and, in some cases, mandatory state withholding. However, if you fail to move the money into a qualified retirement plan within 60 days, it is taxed as ordinary income, plus a 10% penalty if you’re under age 59½, which means you could end up paying significantly more than 20%, depending on your federal and state income tax rates. You may also negatively impact your retirement goals.

**IRS mandates required minimum distributions (RMDs) annually from all such accounts beginning at age 72 (assuming you’re no longer working for the employer sponsoring the account). What is the consequence for failure to calculate the correct amount across multiple accounts? The IRS will slap you with a 50% penalty on the shortfall. Please consult a tax professional for specific tax advice in your situation.