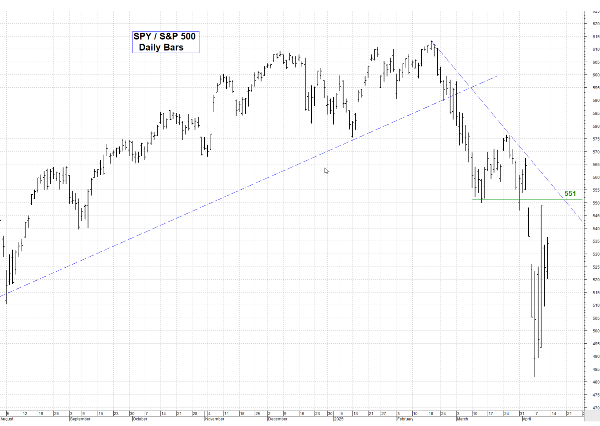

Apple Inc. (NASDAQ: AAPL) has seen a notable pullback in its stock price, dropping 23% year-to-date and over 17.5% in the last month. This decline is sparking questions among investors: is Apple presenting a generational buying opportunity, or is it still overvalued amid tariff-related challenges? This article explores Apple's performance, valuation, and prospects while addressing the factors influencing its stock price.

Tariffs Impacting Apple's Business

The escalating tariffs, currently at an astonishing 145%, are significantly pressuring Apple’s margins. Experts speculate that iPhone prices could surge to $3,500, posing challenges in transferring costs to consumers. While Apple boasts unparalleled brand loyalty, these higher prices could dampen sales or force the company to absorb some of the expenses. To mitigate tariff-related risks, Apple is investing $500 billion over the next few years to relocate production to the U.S., though such efforts will take time to materialize.

Key Fundamentals of Apple

Apple continues to showcase its strong fundamentals:

- Return on Capital: Over 70%, indicating excellent efficiency in generating returns.

- Net Income Margin: A robust 26.5%, driven by its growing services revenue.

- Recurring Revenue Model: Services contribute $73 billion out of $184 billion in gross profits, offering stability and high margins.

- Buybacks: Apple aggressively reduces its shares outstanding, enhancing shareholder value. Since 2013, the company has decreased its share count from 26.5 million to 15.4 million.

Apple also holds $54 billion in cash, ensuring financial resilience in challenging times.

Valuation Analysis

Currently trading at 27 times earnings, Apple's P/E ratio is better than prior valuations but still reflects a historical mean:

- Apple has previously traded at 13-17 times earnings during market downturns, offering superior buying opportunities.

Earnings Growth Assumptions:

Analysts expect Apple’s EPS growth of approximately 10% annually, supported by:

- Revenue growth of 3-4% per year.

- Continued share buybacks reducing market cap by 5-6% annually.

Valuation Scenarios

Using projected EPS of $11.71 over the next five years:

- 27 P/E (Mean Multiple): Targets a price of $316/share in 5 years.

- 23 P/E (Conservative Multiple): Forecasts $269/share in 5 years.

For investors aiming to double their investment:

- At 27 P/E, the buy-in price should be $158/share.

- At 23 P/E, the entry point drops to $134/share.

Strategic Opportunities

Investors can consider dollar-cost averaging between $158-$134/share to minimize downside risks. While Apple remains a high-quality company, the current price may not offer the best risk/reward ratio compared to other opportunities like Alphabet (Google) or Amazon, which trade at lower multiples and exhibit faster growth.

Conclusion

Apple’s pullback presents a potential entry point for long-term investors; however, caution is warranted given tariff-related uncertainties and broader market challenges. While Apple’s fundamentals are strong, investors should monitor its valuation closely and consider waiting for a more favorable price before accumulating shares.

For more insights on valuation strategies and market trends, subscribe to the channel and stay updated on the latest opportunities. Share your thoughts on Apple stock and tariffs in the comments below!

https://youtu.be/gp35P-p7t7M?si=PHwXvW0NnweRaB5V

Apple Inc. (NASDAQ: AAPL) has seen a notable pullback in its stock price, dropping 23% year-to-date and over 17.5% in the last month. This decline is sparking questions among investors: is Apple presenting a generational buying opportunity, or is it still overvalued amid tariff-related challenges? This article explores Apple's performance, valuation, and prospects while addressing the factors influencing its stock price.

Tariffs Impacting Apple's Business

The escalating tariffs, currently at an astonishing 145%, are significantly pressuring Apple’s margins. Experts speculate that iPhone prices could surge to $3,500, posing challenges in transferring costs to consumers. While Apple boasts unparalleled brand loyalty, these higher prices could dampen sales or force the company to absorb some of the expenses. To mitigate tariff-related risks, Apple is investing $500 billion over the next few years to relocate production to the U.S., though such efforts will take time to materialize.

Key Fundamentals of Apple

Apple continues to showcase its strong fundamentals:

Apple also holds $54 billion in cash, ensuring financial resilience in challenging times.

Valuation Analysis

Currently trading at 27 times earnings, Apple's P/E ratio is better than prior valuations but still reflects a historical mean:

Earnings Growth Assumptions: Analysts expect Apple’s EPS growth of approximately 10% annually, supported by:

Valuation Scenarios

Using projected EPS of $11.71 over the next five years:

For investors aiming to double their investment:

Strategic Opportunities

Investors can consider dollar-cost averaging between $158-$134/share to minimize downside risks. While Apple remains a high-quality company, the current price may not offer the best risk/reward ratio compared to other opportunities like Alphabet (Google) or Amazon, which trade at lower multiples and exhibit faster growth.

Conclusion

Apple’s pullback presents a potential entry point for long-term investors; however, caution is warranted given tariff-related uncertainties and broader market challenges. While Apple’s fundamentals are strong, investors should monitor its valuation closely and consider waiting for a more favorable price before accumulating shares.

For more insights on valuation strategies and market trends, subscribe to the channel and stay updated on the latest opportunities. Share your thoughts on Apple stock and tariffs in the comments below!

https://youtu.be/gp35P-p7t7M?si=PHwXvW0NnweRaB5V