Expertise provided by Kevin Matthews from buildingbread.com

The financial industry plays a role, in the economy, and investing in bank stocks has been a popular choice for many looking for steady returns, dividends, and growth. However, deciding whether to invest in bank stocks is not always straightforward.

Are banks an investment option and what factors should one consider when selecting bank stocks? I don't find banks exciting. I think there are less risky options in finance. In recent years, news of downturns and rising inflation has hurt bank stocks. These sectors are known for their stability and predictability. For instance, insurance is often required, such as car insurance. Many jobs come with insurance benefits making it a dependable industry. Therefore, my inclination leans towards these areas. Banks are not investments. But, in my opinion, they may not perform as well as credit card companies or insurers.

Pros of Investing in Bank Stocks

There are good and bad aspects. One should weigh them before investing.

Advantages of Investing in Bank Stocks:

i. Dividend Income: Banks often give a share of their earnings to shareholders as dividends. Dividends offer investors income.

ii. Stability: Banks are usually seen as vulnerable during downturns. This is due to their crucial role in the economy. They provide financial services like loans to businesses and people.

iii. Growth potential: Banks can grow revenue by expanding, acquiring, and introducing new products.

iv. Benefit from Increasing Interest Rates: Banks earn profits by lending money at higher interest rates. These rates are higher than what they pay on deposits. With rising interest rates banks can enhance their profit margins.

v. Government-insured deposits: Many countries have deposit insurance programs. These programs are backed by the government. They safeguard investors from losing their funds if a bank collapses. This assurance can offer peace of mind to investors.

Disadvantages of Investing in Bank Stocks

i. Vulnerability during downturns: Despite being relatively stable banks are still susceptible to contractions. In times of recession loan defaults may. Lead banks to reduce dividends.

ii. Regulatory constraints: The banking sector faces regulations that could restrict the profitability of banks.

iii. Interest rate fluctuations risk: Banks profitability can be influenced by changes in interest rates. A decrease, in interest rates may shrink banks profit margins.

iv. Competition: in the banking sector is intensifying due to the entry of fintech firms leading to increased pressure, on banks profitability.

v. Potential for fraud: Banks face a risk of fraud, which may result in losses

How to Value Bank Stocks

When considering investing in bank stocks it's crucial to evaluate the company’s value. Many factors influence bank stock prices. These include indicators like the price to earnings (P/E) ratio, return on equity (ROE), and debt to equity (D/E) ratio. These ratios offer insights into the bank’s profit and financial stability. Assessing a bank's growth potential is essential. You can do this through metrics like loan growth, deposit growth, and new product offerings. The dividend yield is calculated by dividing the dividend per share by the stock price. It can attract income investors to banks with high yields. Also, market conditions determine how bank stocks perform relative to the market. For example, during periods of rising interest rates.

How to Calculate Profitability Ratios for a Bank?

Source: Investopedia

Source: Investopedia

To compute profitability ratios for banks, you need to gauge their ability to generate profits from assets and equity. It is important to consider the ratios and their formulas.

1. Return on Equity (ROE):

Return on Equity (ROE) is a metric. It shows how profitable a bank is about the funds its shareholders invest. Essentially it gauges how efficiently the bank utilizes shareholder capital to generate profits.

Formula: ROE = Net Income / Shareholders' Equity

2. Return on Assets (ROA):

It measures how well a bank uses its assets to make profits. It shows the profit generated relative to the assets owned. The Net Profit Margin shows the percentage of revenue kept as profit. This is after deducting all expenses.

Formula: Net Profit Margin = Net Income / Revenue

Here's an example:

Let's say a bank has the following financial data:

Net Income: $100 million

Shareholders' Equity: $500 million

Total Assets: $1 billion

Revenue: $2 billion

ROE = $100 million / $500 million = 0.2 (or 20%)

ROA = $100 million / $1 billion = 0.1 (or 10%)

Net Profit Margin = $100 million / $2 billion = 0.05 (or 5%)

These figures suggest the bank earns a 20% return on equity and a 10% return on assets. It keeps 5 cents in profit for every dollar it earns. By evaluating these ratios against the bank's performance and industry standards, you can understand the bank's profitability. You can also see how attractive it is as an investment.

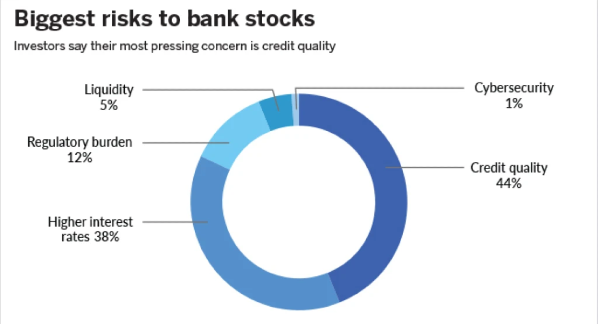

Risks of Bank Stocks

Source: Piper Sandler Annual Bank Investor Survey

Source: Piper Sandler Annual Bank Investor Survey

Purchasing bank stocks comes with risks that investors must assess thoughtfully. Here are some key risks to be aware of;

i. Credit Risk:

When borrowers fail to repay their loans it creates credit risk, for banks as it leads to loan defaults. Banks heavily depend on loan repayments to make money. If there is a rate of loan defaults it can significantly affect a banks profits and financial stability.

ii. Interest Rate Risk:

Banks are sensitive to changes in interest rates. If interest rates go up borrowing becomes more expensive for individuals and businesses which could lower the demand for loans. On the other hand if interest rates decrease, the net interest margin (NIM). The gap between interest income earned and interest paid out. May shrink.

iii. Regulatory Risk:

The banking sector faces regulations that can impact operations and profitability when rules change. Tougher regulations can increase compliance costs reduce profitability and limit growth opportunities for banks.

iv. Economic Risk:

The performance of bank stocks is closely linked to the economy health. During downturns or recessions, banks might experience loan defaults decreased loan demand and lower fee income from financial services. Economic instability can also affect investor trust and stock values.

v. Market Risk:

Market risk involves stock price fluctuations. They are caused by market shifts in investor sentiment and external events, like issues.

Investing in bank shares can be risky as they are prone, to fluctuations and challenging market circumstances may result in setbacks.

vi. Liquidity Risk:

It occurs when a bank is not able to pay back its short-term financial obligations due to an inability to quickly convert assets into cash. This can arise from a sudden withdrawal of deposits or a freeze in credit markets. The harsh part is that it potentially leads to solvency issues.

vii. Operational Risk:

It happens because of inadequate or failed internal processes, systems, or controls. This can include fraud, cyber-attacks, and technology failures, which can lead to financial losses and damage to reputation.

Are bank stocks worth buying?

Are bank stocks worth buying? It depends on your investment goals and risk tolerance. Bank stocks can offer stability and dividends, but they also carry risks like economic downturns and regulatory changes. Assess the pros and cons carefully to determine if they align with your investment strategy.

Are banks a good place to invest?

Banks can be a solid investment, especially for those seeking stability and dividends. However, their performance during inflation varies. On one hand, banks benefit from higher interest rates, which can increase their net interest margin. Inflation can also cause economic uncertainty. It can increase loan defaults and reduce borrowing. Thus, while banks may fare well in moderate inflation, high inflation poses risks. Carefully consider your investment goals and the current economic environment before investing in bank stocks.

Are banks an investment option?

Investing in banks can be a choice, for those seeking stable returns and dividends. However, their performance may be affected by inflation. Higher interest rates can benefit banks. They increase their interest margin. But inflation creates uncertainty. It might lead to higher loan defaults and less borrowing. Therefore, while banks may perform well in inflation scenarios high inflation could pose risks.

Before diving, into bank stocks take a moment to think about your investment objectives. How the economy is shaping up.

Conclusion

The decision to invest in bank stocks depends on different factors. While bank stocks may present an investment opportunity, for individuals they may not be the right choice for everyone. It is essential to weigh the advantages and disadvantages of investing in bank stocks before reaching a conclusion. You should evaluate factors like your risk tolerance and investment objectives. Also, consider current market conditions. They will show if bank stocks fit into your investment plan.

For more information watch this video:

https://youtu.be/D4dG4LvB4ic

Expertise provided by Kevin Matthews from buildingbread.com

The financial industry plays a role, in the economy, and investing in bank stocks has been a popular choice for many looking for steady returns, dividends, and growth. However, deciding whether to invest in bank stocks is not always straightforward.

Are banks an investment option and what factors should one consider when selecting bank stocks? I don't find banks exciting. I think there are less risky options in finance. In recent years, news of downturns and rising inflation has hurt bank stocks. These sectors are known for their stability and predictability. For instance, insurance is often required, such as car insurance. Many jobs come with insurance benefits making it a dependable industry. Therefore, my inclination leans towards these areas. Banks are not investments. But, in my opinion, they may not perform as well as credit card companies or insurers.

Pros of Investing in Bank Stocks

There are good and bad aspects. One should weigh them before investing.

Advantages of Investing in Bank Stocks:

i. Dividend Income: Banks often give a share of their earnings to shareholders as dividends. Dividends offer investors income. ii. Stability: Banks are usually seen as vulnerable during downturns. This is due to their crucial role in the economy. They provide financial services like loans to businesses and people. iii. Growth potential: Banks can grow revenue by expanding, acquiring, and introducing new products. iv. Benefit from Increasing Interest Rates: Banks earn profits by lending money at higher interest rates. These rates are higher than what they pay on deposits. With rising interest rates banks can enhance their profit margins. v. Government-insured deposits: Many countries have deposit insurance programs. These programs are backed by the government. They safeguard investors from losing their funds if a bank collapses. This assurance can offer peace of mind to investors.

Disadvantages of Investing in Bank Stocks

i. Vulnerability during downturns: Despite being relatively stable banks are still susceptible to contractions. In times of recession loan defaults may. Lead banks to reduce dividends. ii. Regulatory constraints: The banking sector faces regulations that could restrict the profitability of banks. iii. Interest rate fluctuations risk: Banks profitability can be influenced by changes in interest rates. A decrease, in interest rates may shrink banks profit margins. iv. Competition: in the banking sector is intensifying due to the entry of fintech firms leading to increased pressure, on banks profitability. v. Potential for fraud: Banks face a risk of fraud, which may result in losses

How to Value Bank Stocks

When considering investing in bank stocks it's crucial to evaluate the company’s value. Many factors influence bank stock prices. These include indicators like the price to earnings (P/E) ratio, return on equity (ROE), and debt to equity (D/E) ratio. These ratios offer insights into the bank’s profit and financial stability. Assessing a bank's growth potential is essential. You can do this through metrics like loan growth, deposit growth, and new product offerings. The dividend yield is calculated by dividing the dividend per share by the stock price. It can attract income investors to banks with high yields. Also, market conditions determine how bank stocks perform relative to the market. For example, during periods of rising interest rates.

How to Calculate Profitability Ratios for a Bank?

To compute profitability ratios for banks, you need to gauge their ability to generate profits from assets and equity. It is important to consider the ratios and their formulas.

1. Return on Equity (ROE): Return on Equity (ROE) is a metric. It shows how profitable a bank is about the funds its shareholders invest. Essentially it gauges how efficiently the bank utilizes shareholder capital to generate profits. Formula: ROE = Net Income / Shareholders' Equity

2. Return on Assets (ROA): It measures how well a bank uses its assets to make profits. It shows the profit generated relative to the assets owned. The Net Profit Margin shows the percentage of revenue kept as profit. This is after deducting all expenses. Formula: Net Profit Margin = Net Income / Revenue

Here's an example: Let's say a bank has the following financial data: Net Income: $100 million Shareholders' Equity: $500 million Total Assets: $1 billion Revenue: $2 billion ROE = $100 million / $500 million = 0.2 (or 20%) ROA = $100 million / $1 billion = 0.1 (or 10%) Net Profit Margin = $100 million / $2 billion = 0.05 (or 5%)

These figures suggest the bank earns a 20% return on equity and a 10% return on assets. It keeps 5 cents in profit for every dollar it earns. By evaluating these ratios against the bank's performance and industry standards, you can understand the bank's profitability. You can also see how attractive it is as an investment.

Risks of Bank Stocks

Purchasing bank stocks comes with risks that investors must assess thoughtfully. Here are some key risks to be aware of;

i. Credit Risk:

When borrowers fail to repay their loans it creates credit risk, for banks as it leads to loan defaults. Banks heavily depend on loan repayments to make money. If there is a rate of loan defaults it can significantly affect a banks profits and financial stability.

ii. Interest Rate Risk:

Banks are sensitive to changes in interest rates. If interest rates go up borrowing becomes more expensive for individuals and businesses which could lower the demand for loans. On the other hand if interest rates decrease, the net interest margin (NIM). The gap between interest income earned and interest paid out. May shrink.

iii. Regulatory Risk:

The banking sector faces regulations that can impact operations and profitability when rules change. Tougher regulations can increase compliance costs reduce profitability and limit growth opportunities for banks.

iv. Economic Risk:

The performance of bank stocks is closely linked to the economy health. During downturns or recessions, banks might experience loan defaults decreased loan demand and lower fee income from financial services. Economic instability can also affect investor trust and stock values.

v. Market Risk:

Market risk involves stock price fluctuations. They are caused by market shifts in investor sentiment and external events, like issues. Investing in bank shares can be risky as they are prone, to fluctuations and challenging market circumstances may result in setbacks.

vi. Liquidity Risk:

It occurs when a bank is not able to pay back its short-term financial obligations due to an inability to quickly convert assets into cash. This can arise from a sudden withdrawal of deposits or a freeze in credit markets. The harsh part is that it potentially leads to solvency issues.

vii. Operational Risk:

It happens because of inadequate or failed internal processes, systems, or controls. This can include fraud, cyber-attacks, and technology failures, which can lead to financial losses and damage to reputation.

Are bank stocks worth buying?

Are bank stocks worth buying? It depends on your investment goals and risk tolerance. Bank stocks can offer stability and dividends, but they also carry risks like economic downturns and regulatory changes. Assess the pros and cons carefully to determine if they align with your investment strategy.

Are banks a good place to invest?

Banks can be a solid investment, especially for those seeking stability and dividends. However, their performance during inflation varies. On one hand, banks benefit from higher interest rates, which can increase their net interest margin. Inflation can also cause economic uncertainty. It can increase loan defaults and reduce borrowing. Thus, while banks may fare well in moderate inflation, high inflation poses risks. Carefully consider your investment goals and the current economic environment before investing in bank stocks.

Are banks an investment option?

Investing in banks can be a choice, for those seeking stable returns and dividends. However, their performance may be affected by inflation. Higher interest rates can benefit banks. They increase their interest margin. But inflation creates uncertainty. It might lead to higher loan defaults and less borrowing. Therefore, while banks may perform well in inflation scenarios high inflation could pose risks. Before diving, into bank stocks take a moment to think about your investment objectives. How the economy is shaping up.

Conclusion

The decision to invest in bank stocks depends on different factors. While bank stocks may present an investment opportunity, for individuals they may not be the right choice for everyone. It is essential to weigh the advantages and disadvantages of investing in bank stocks before reaching a conclusion. You should evaluate factors like your risk tolerance and investment objectives. Also, consider current market conditions. They will show if bank stocks fit into your investment plan.

For more information watch this video:

https://youtu.be/D4dG4LvB4ic